- EIA’s International Energy Outlook projects a 34 percent increase in world energy consumption by 2050 due to global population growth, increased regional manufacturing, and higher living standards.

- Carbon dioxide emissions are expected to increase by 15 percent between 2022 and 2050 as fossil fuels still supply about 70 percent of the world’s energy by 2050.

- China will still be far-and-away the largest energy consumer and carbon dioxide emitter, but its world share of emissions will drop due mainly to a declining population that is expected to slow GDP growth.

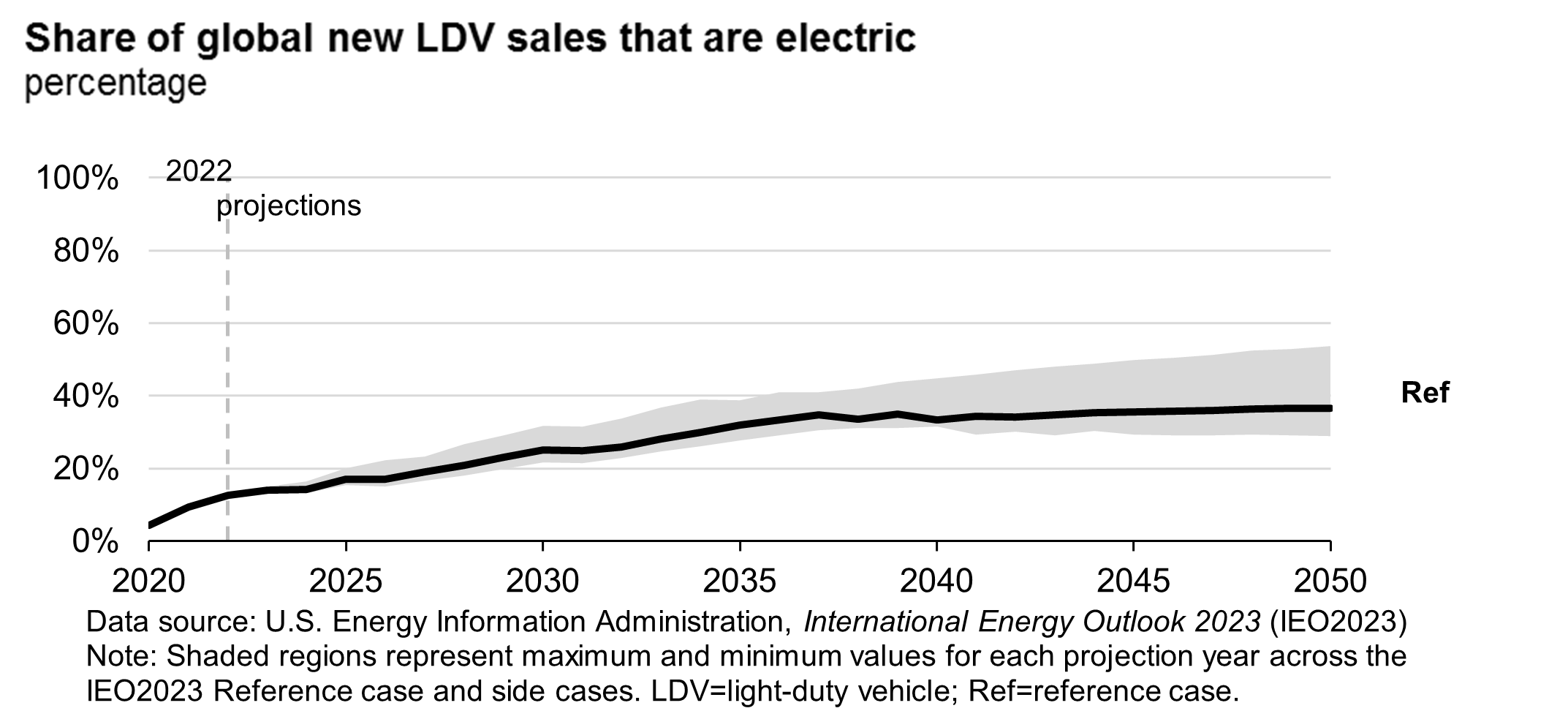

- Sales of electric vehicles are expected to increase, led primarily by China and Europe, adding to an existing fleet of 1.4 billion internal combustion engine vehicles worldwide.

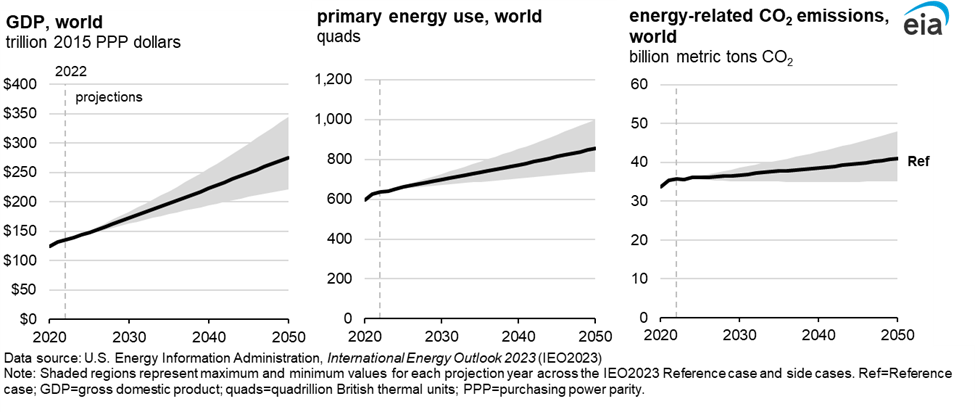

According to the Energy Information Administration’s (EIA) International Energy Outlook, global energy consumption is expected to increase by 34 percent between 2022 and 2050, outpacing advances in energy efficiency. Global population growth, increased regional manufacturing and higher living standards contribute to the increase in consumption, resulting in 15-percent higher global carbon dioxide emissions from energy by 2050. Population growth is concentrated in Africa, India, and Other Asia-Pacific, which combined, contribute 94 percent of the expected 1.7 billion people added to the global population by 2050. Non-fossil fuel-based resources, including nuclear and renewable energy, are expected to produce more energy through 2050, but that growth is not expected to reduce global energy-related carbon dioxide emissions under current laws and regulations. Fossil fuels are expected to provide about 70 percent of total primary energy in 2050, down from 79 percent in 2022.

EIA runs multiple scenarios besides a reference case based on different assumptions, including higher and lower macroeconomic assumptions, higher and lower oil prices, and higher and lower technology costs. For that reason, EIA’s forecast provides a range of results.

Electric Sector

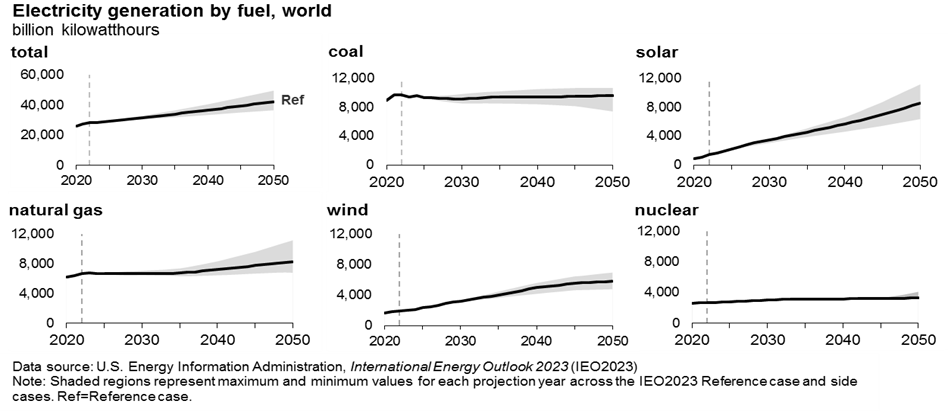

EIA expects global electric-power generating capacity by 2050 to increase by between 50 percent and 100 percent and electricity generation is expected to increase between 30 percent and 76 percent relative to 2022, as countries push electrification through renewable energy (mainly solar and wind power), which have much lower capacity factors. Electricity generation from renewables and nuclear could provide as much as two-thirds of global electricity generation by 2050, with solar and wind showing the highest levels of electricity generation growth. Meanwhile, coal and natural gas are expected to make up between 27 percent and 38 percent of power generation capacity by 2050, down from about half in 2022. Battery storage capacity is expected to grow, increasing from less than 1 percent of global power capacity in 2022 to between 4 percent and 9 percent of global power capacity by 2050.

EIA expects zero-carbon technology capacity to increase faster early in the projection period in Western Europe and China because of policy, rapid demand growth, and energy security considerations that favor locally available resources such as wind and solar power.

Personal Travel

EIA expects transportation-sector energy consumption to grow between 8 percent and 41 percent from 2022 to 2050, depending on the case.

Electric vehicles are expected to account for between 29 percent and 54 percent of global new vehicle sales by 2050 (36 percent in the Reference case in 2050) compared to 13 percent in 2022. China and Western Europe account for between 58 percent and 77 percent of the EV sales. Continued increases in EV adoption leads to a projected peak in the global fleet of internal combustion engine light-duty vehicles between 2027 and 2033 at 1.5 billion vehicles in the reference case. After 2033, the global internal combustion engine fleet is expected to remain at its 2022 level of 1.4 billion vehicles in the Reference case.

Oil and Natural Gas

The Middle East and North America are expected to increase natural gas production and exports to meet growing international demand, and Western Europe and Asia remain natural gas importers. Energy demand from China, India, Southeast Asia, and Africa is expected to incentivize oil and natural gas production. Near- to mid-term (2023–2035) growth in crude oil production is met by non-OPEC regions, particularly in North and South America. OPEC regains market share as other regions reach peak production, generally between 2030 and 2040. EIA expects reduced gasoline demand due to rising EV sales and rising demand for jet fuel due to global economic growth, which is expected to drive changes in refineries. Refineries are currently configured to meet gasoline and distillate demand and cannot easily change the petroleum ratio of products they produce. To address the shift in global products demand, refineries must adjust oil inputs, resulting in a transition from light oil to medium oil.

Carbon Dioxide Emissions

EIA expects carbon dioxide emissions from coal to increase by 3.9 percent from 2022 to 2050 in the Reference case, natural gas carbon dioxide emissions to increase by 28 percent and liquid fuel carbon dioxide emissions to increase by 20 percent as current policies are not enough to decrease global energy-sector emissions. Growth in carbon dioxide emissions is largely due to population growth, regional economic shifts toward more manufacturing, and increased energy consumption as living standards improve. Consumption of coal in the Reference case is expected to increase by 3.7 percent between 2022 and 2050, consumption of liquids is expected to increase by 21.8 percent, and consumption of natural gas is expected to increase by 28.5 percent.

Global gross domestic product (GDP) is expected to more than double by 2050 in all of the cases, except the Low Economic Growth case. The intensity of energy-related carbon dioxide emissions (carbon dioxide emissions per unit of primary energy) decreases through 2050, despite overall emissions increases. The decreasing emissions intensity reflects a transition toward lower-carbon energy sources and increasing efficiencies driven by new technology.

China is expected to remain the primary source of energy-related carbon dioxide emissions across all EIA cases, although its share of total global carbon dioxide emissions declines from 32 percent in 2022 to 26 percent in 2050 in EIA’s Reference case as a declining population is expected to slow GDP growth in China relative to recent history. India is expected to displace the United States as the second highest emitter of energy-related carbon dioxide emissions, increasing its share from 7 percent in 2022 to 13 percent in 2050 in the Reference case, and the Other Asia-Pacific region is expected to displace Western Europe as the third-highest emitter of energy-related carbon dioxide emissions by 2050, increasing its share from 8 percent in 2022 to 12 percent in 2050.

Conclusion

EIA projects that global energy demand and energy-related carbon dioxide emissions will increase through 2050 based on current world policies. China will still lead the world in carbon dioxide emissions, despite reducing its share as India and other Asia Pacific regions emit more carbon dioxide. Wind and solar capacity increases as nations pursue non-carbon generating options. Coal and natural gas generation reduce their combined share amid a growth in electricity demand from government’s push for non-carbon fuels and electric vehicles, whose share increases, but remains below 50 percent in the Reference case in 2050.