Western European countries started the bandwagon to reach carbon neutrality by 2050, instituting a cap-and-trade program to reduce carbon dioxide emissions and rushing headlong into renewable energy, particularly wind and solar power—intermittent technologies that cannot be relied on to deliver power 24/7. Energy shortages resulting from high energy demand as countries recover from the COVID lockdowns, low wind generation and cutbacks of exports by Russia have raised European energy prices to record heights, making European leaders accelerate the rush into renewable energy. However, they will find shortages again as a recent study by KU Leuven University shows that meeting the European Union’s Green Deal goal of “climate neutrality” by 2050 will require 35 times more lithium and 7 to 26 times the amount of rare earth metals compared to Europe’s current use. These metals along with other critical metals are considered essential for producing wind, solar and hydrogen energy technologies, as well as the grid infrastructure needed for them, and for producing electric vehicles and batteries.

Further, other countries’ demand, including that of the United States, will also put pressure on the demand and prices for these metals. President Biden has goals for 50 percent of new car sales in the United States to be electric by 2030, a carbon free electric grid by 2035, and a carbon free economy by 2050. All of this requires massive amounts of new minerals, at a time when shortages of them and escalating prices abound.

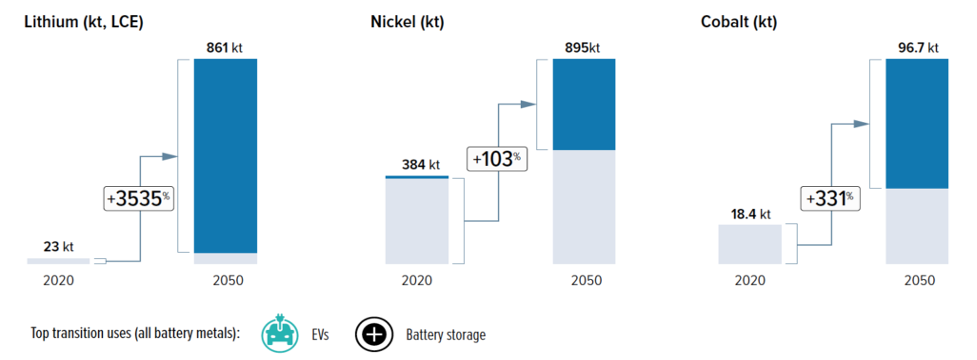

The KU Leuven University Study

According to the study, besides the increase in lithium and rare earth metals, the energy transition will also require 30 percent more aluminum than what is used currently, and 35 percent more copper, 45 percent more silicon, 100 percent more nickel and 330 percent more cobalt. That is, about 4.5 million metric tons of aluminum, 1.5 million metric tons of copper, 800,000 metric tons of lithium, 400,000 metric tons of nickel, 300,000 metric tons of zinc, 200,000 metric tons of silicon, 60,000 metric tons of cobalt, and 3,000 metric tons of the rare earths metals neodymium, dysprosium and praseodymium, which is an increase between 700 and 2,600 percent from current levels. The report indicates that Europe faces critical shortfalls in the next 15 years without more mined and refined metals supplying its renewable energy system.

Source: https://www.mining.com/europes-green-deal-requires-massive-amounts-of-battery-metals-study/

According to the study, global supply shortages for five raw materials (lithium, cobalt, nickel, rare earths, and copper) could occur around 2030 with the European Union’s primary metals demand peaking around 2040. Coal-powered Chinese and Indonesian metal production currently dominate global refining capacity growth for battery metals and rare earths. Similar to Europe’s dependence on Russia for fossil fuels, Europe also relies on Russia for its current supply of aluminum, nickel and copper.

The report indicates that Europe needs to start building solid bridges with proven responsible suppliers, managing their environmental and social risks. Currently, there is little community buy-in or positive business conditions for the continent to build its own strong supply chains. The study indicates that projects need to be taken forward in the next two years to be ready by 2030. There is the potential for new domestic mines to cover between 5 percent and 55 percent of Europe’s 2030 needs, with the largest project pipelines for lithium and rare earths. However, most announced projects are struggling with local community opposition and permit challenges, or relying on untested processes.

Because most of these metals need to be processed, Europe also needs to open new refineries to transform mined ores and secondary raw materials into metals or chemicals. Europe’s current energy crisis makes new refining investment challenging, as skyrocketing power prices have caused the temporary closure of nearly half the continent’s existing refining capacity for aluminum and zinc. Europe’s environmental stance against greenhouse gas emissions will be working against these mining and refinery goals and toward dependency on coal-fired China for the needed minerals and the processing of them.

The report indicates that after 2040, increased recycling will help Europe gain greater self-sufficiency, assuming major investments are made in recycling infrastructure and legislative bottlenecks are addressed.

Biden’s America Mimics Europe’s Goals and Regulatory Actions

President Biden’s goals toward a carbon free United States, as mentioned above, are similar to Europe’s. And, further, Biden’s regulatory stance toward mining has obstacles similar to that found in Europe.

On March 31, President Biden invoked the Defense Production Act to increase domestic production of minerals used in making electric vehicles, such as nickel, lithium and cobalt, because the country depends on unreliable foreign sources for many materials necessary for transitioning to the use of renewable energy. Biden’s order directs the Defense Department to consider at least five metals — lithium, cobalt, graphite, nickel and manganese — as essential to national security and authorizes steps to bolster domestic supplies. But, Biden’s action does not waive, streamline or suspend existing environmental and labor standards, nor does it address a major hurdle to increased domestic extraction of these critical minerals: the years-long process needed to obtain the necessary federal permits for a new mine.

While the United States has abundant mineral resources, the policy to ensure that they are produced, and to build secure, reliable supply chains is absent. For example, in January, the Biden administration revoked the federal leases for the Twin Metals mine in Minnesota that contains copper, nickel, cobalt, and platinum-group elements. Other critical mineral mines have suffered regulatory and environmental challenges from the Biden administration over the past year. And, last June, President Biden indicated that he wants to import these metals, supposedly from Allies. A majority of global lithium production comes from China, Australia, Argentina and Chile, while Russia dominates the global nickel market and the Democratic Republic of Congo is the world’s largest cobalt producer with half of its large mines owned by China. European allies are actually closing mining and processing facilities due to their exceptionally high energy prices, as noted above.

Conclusion

The KU Leuven University study indicates the massive amounts of critical metals needed for Europe to achieve its carbon free goals by 2050. The report urges the European Union to act now to develop a domestic critical mineral mining industry, the appropriate supply chains, and a recycling program to become less import dependent on these metals. The United States is in a similar situation to Europe.

The Biden presidency is all talk and little positive action toward the energy needs of the country, whether it is oil, natural gas, or coal or the critical minerals needed for producing renewable technologies. Despite the President invoking the defense production act, unless his administration streamlines permitting, there will be no meaningful increase in American mineral production. All signs point to just the opposite, with the Biden administration increasing the power of the federal government over the National Environmental Policy Act and reversing the Trump administration’s limitations on “compensatory mitigation” (requiring projects to pay for whatever bureaucrats want as a condition for a permit.) For a domestic critical mining program to evolve, President Biden needs to “stand up to mining opponents in his own party,” as Wyoming Senator Barrasso indicated.