by Andrew Chamberlain

Fiscal Economics, Inc.

Commissioned by the Institute for Energy Research (IER)

September 2008

PDF (248KB)

Abstract

The recently released “Gang of Ten” energy proposal includes revenue offsets that would exclude domestic oil and gas companies from the Section 199 deduction for domestic production activity. Using a simple input-output model, we estimate the state-by-state impact of this proposal on tax burdens, employment, household earnings and economic output. By depressing the U.S. domestic oil and gas industry through increased corporate tax burdens, we estimate the proposal is likely to increase reliance on foreign sources of oil from unstable regimes. Specifically the proposal will increase corporate tax burdens by approximately $13.57 billion over 10 years, 44 percent of which will fall on households in the petroleum manufacturing states of Texas, California and Louisiana. Using RIMS II multipliers we estimate the proposal will reduce U.S. employment by roughly 637,000 jobs over 10 years, reduce household earnings by $34.97 billion, and reduce total U.S. economic output by $185.95 billion.

Executive Summary

A tax increase in the “New Energy Reform Act of 2008,” (NERA) being proposed by a bipartisan group of 16 members in Congress, is likely to increase U.S. reliance on imported oil from politically unstable nations, cost the U.S. economy 637,000 jobs and reduce U.S. household earnings by nearly $35 billion over the next 10 years.

The tax increases would result in a weaker domestic energy industry, thus making America more reliant on oil from foreign sources, including unstable regimes overseas. Higher U.S. corporate tax burdens on the energy sector are likely to discourage U.S. investment and employment, thus reducing domestic production while stimulating investment and jobs abroad. Since America’s energy demand is forecast to grow 34 percent in the next two decades, any hindrance to domestic production is likely to increase U.S. dependence on imported oil, including from politically unstable regimes such as Venezuela, Nigeria and Russia, threatening U.S. energy security and, by extension, national security.

Currently, the U.S. produces 5.1 million barrels of oil per day, which is enough to barely meet only 25 percent of the country’s energy demand. As domestic production of oil and gas shrinks relative to foreign production, the United States will tend to become more dependent on imported oil in order to meet its needs and lose its negotiating power in world energy markets.

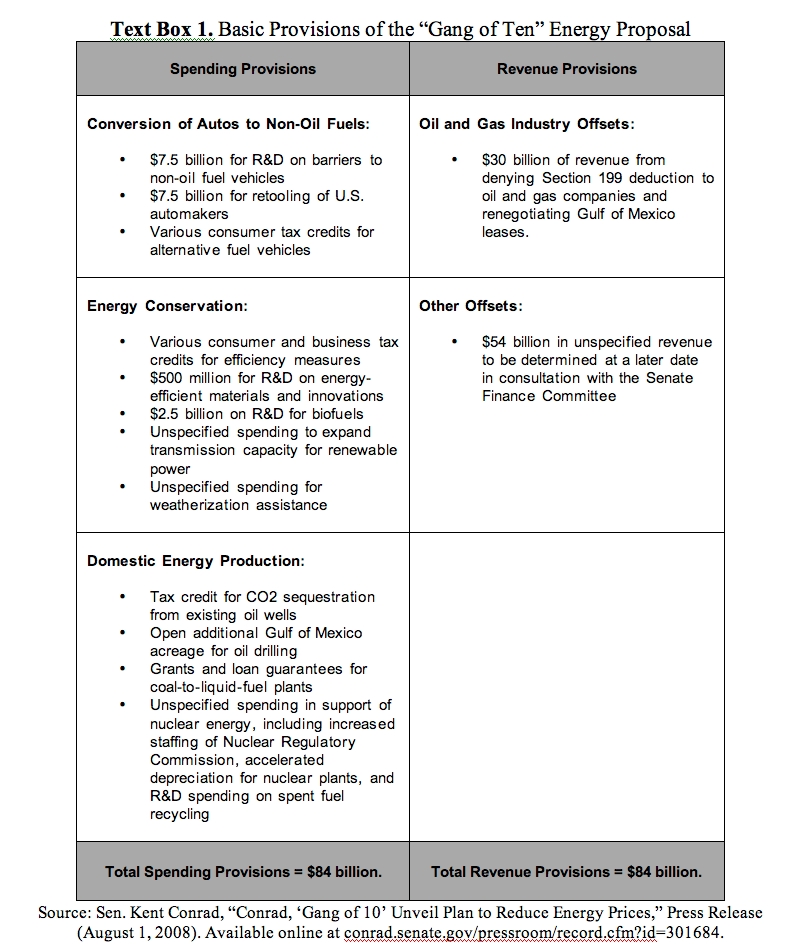

NERA proposes $84 billion in new spending on alternative energy and conservation measures over the next 10 years, financed in part by $30 billion in tax increases on the oil and gas industry. The most significant tax provision would repeal oil and gas companies’ ability to claim the Section 199 domestic manufacturing deduction, which was enacted by Congress in 2004 as part of the American Jobs Creation Act to encourage U.S. companies to increase employment in the United States.

The Section 199 deduction was enacted when other Congressional efforts to provide corporate income tax relief to American export industries were ruled in violation of world trade rules against export subsidies.

When fully implemented, the Section 199 deduction would effectively lower the U.S. federal corporate tax rate from 35 percent to 31.85 percent, more in line with the lower corporate tax rates now available in other industrial countries.

Elimination of the deduction for the oil and gas industry would result in higher corporate tax burdens for domestic oil and gas companies compared to other U.S. manufacturing industries, including filmmaking. On the world stage, U.S. oil and gas companies could not hope to keep pace with competitors in countries with lower tax rates.

A 2006 Congressional Budget Office study based on an open-economy model resembling the U.S. economy estimates that roughly 70 percent of the U.S. corporate tax burden is borne by domestic workers in the form of lower wages; domestic owners of capital—which today are predominately institutional investors, including both private and public pension funds—bear the remaining 30 percent.

Projections in previously proposed measures to eliminate the Section 199 deduction for the petroleum industry estimated it would raise $13.57 billion over 10 years. $9.5 billion of that additional tax burden is estimated to fall on workers and $4.07 billion would be borne by shareholders in the form of lower returns. A closer examination finds that workers in three states—California, Texas and Louisiana—would bear $5.3 billion of the lost wages, while investors in California, Florida and New York would bear $1.4 billion of the lower returns.

Ripple, or multiplier, effects extend beyond the integrated energy industries to additional workers and shareholders. Multipliers from the “Regional Impact Modeling System” from the Bureau of Economic Analysis take into account such ripple effects. They indicate the repeal of Section 199 would cost workers and shareholders an overall loss of 637,000 jobs over 10 years, including 352,000 in Texas, California and Louisiana, and reduce overall household earnings across the United States by $34.97 billion or $330 per U.S. household.

The losses to the economy in terms of jobs and shareholder earnings from a repeal of the Section 199 deduction essentially amount to 2.5 times the benefit the federal government would derive in increased tax revenues. The losses of $186 billion to total economic activity, however, amount to 13.5 times the benefit the federal government would derive. The repeal of the Section 199 deduction is more than the simple withdrawing of a tax deduction; it’s a mortgage on our nation’s energy future.

The primary reason for the job losses stems from investment dynamics. Investors allocate their resources to maximize return. Consequently, industries burdened by corporate profits taxes attract fewer investors, placing jobs in those industries in jeopardy. Moreover, increasing corporate taxes on the U.S. energy sector increase the costs of production and may reduce the resources available for research and development compared to other countries, making the U.S. energy sector less attractive for investment.

Foreword

Politics has been described as the art of the possible. On the other hand, economics has earned the sobriquet of a dismal science, demonstrating that achieving the possible is often not worth it.

The squeeze put on the economy by recent high energy prices coupled with concerns about both energy security and climate change has led some members in Congress to seek what they see as a possible solution to all three.

Their plan offers something for everyone. It would provide massive new subsidies for the development of renewable energy – wind and solar – to satisfy environmentalists. It also would give massive tax breaks for carbon capture for coal fired power plants, since coal remains the largest source of domestic energy available, providing half of our electricity needs. In a bow to the reality that a precipitous decline in domestic oil and gas production could continue to undermine our economic well-being through further increases in energy prices, their plan seeks to open a small area of federal land and offshore areas to energy exploration and development.

And then there is the manner in which these new subsidies and tax breaks are paid for. Proponents would engage in a direct assault upon the earnings of the nation’s integrated oil and gas companies and, in the process, put at risk hundreds of thousands of U.S. jobs and hundreds of billions in U.S. economic activity.

That is the dismal conclusion drawn in a recent examination by senior economist Andrew Chamberlain of Fiscal Economics, Inc. of the proposal to deny integrated oil companies the same production deductions Congress makes available to other U.S. manufacturing industries, such as filmmakers. Using a standard economic model of the effect of corporate income taxes, Chamberlain determines that the loss to the economy would be almost 15 times the amount of revenue raised by that plan.

Proponents of higher taxes on the nation’s integrated oil industry sell the plan by attacking “windfall profits” in the oil industry. They ignore the fact that those profits remain well within the norms for other U.S. industries; are paid mostly to institutional investors such as pension and mutual funds endowing U.S. workers’ retirements; and are vital to maintaining earnings that attract capital for additional development of domestic energy resources.

People invest their money to maximize its return. Consequently, industries that face big capital losses attract fewer investors. Both foreign-headquartered private oil companies and foreign nationally controlled oil companies, including those in Iran, Saudi Arabia, Nigeria, Venezuela, China and Russia, would gain a distinct competitive advantage over domestically headquartered integrated oil companies in attracting capital. Among the implications of this plan, Americans would become more reliant on unstable regimes for their oil supply, rather than cultivating domestic resources and enhancing U.S. energy security.

Furthermore, by giving a competitive advantage to foreign companies over the domestic producers America will further weaken its hand in global energy geopolitics.

This attempt to extract additional revenues from the domestic oil and gas industries by attacking their earnings will have the perverse effect of making it more economically attractive to more oil and refined products such as gasoline, rather than producing those goods here at home. In short, we’d send even more of our money and jobs abroad, further weakening our national economy, our energy security and our stature in global energy markets.

This plan is not America’s only option. There are better ways to raise additional funds for renewable and cleaner energy development and to encourage conservation without putting domestic jobs and energy development at risk. Opening access to federal lands would generate additional federal revenue in lease and royalty payments. A portion of that new revenue could be designated toward incentives for new technology. And certainly there are other ways to increase domestic energy development that make more sense than fiscally assaulting domestic energy producers.

In the long run, good policy must be based on solid principles that advance the U.S. economy, not mire the nation in economic disaster. At the same time, policymakers must act to protect all aspects of our nation’s energy future and prevent unintended economic consequences.

Thomas Pyle,

President, IER

I. Introduction

On August 1, 2008, a coalition of 10 U.S. Senators announced a sweeping federal energy plan titled the “New Energy Reform Act of 2008.” Led by Sens. Kent Conrad (D-N.D.) and Saxby Chambliss (R-Ga.), the group’s proposal features $84 billion in new spending on alternative energy and conservation measures, including $7.5 billion for R&D on alternative-fuel vehicles, $2.5 billion for research on biofuels, and a range of consumer and business tax credits aimed at encouraging energy efficiency and reducing demand for oil and gas.

To finance this new spending, the proposal includes $30 billion in tax increases on the oil and gas industry and $54 billion of other unspecified offsets. Among the tax provisions, the most significant is the proposed repeal of oil and gas companies’ ability to claim the Section 199 domestic manufacturing deduction—a deduction only recently enacted by Congress as part of the American Jobs Creation Act of 2004 and designed to encourage U.S. companies to increase employment in the United States.

By eliminating the Section 199 deduction for oil and gas companies, the “Gang of Ten” proposal would increase the effective corporate tax rate faced by domestic petroleum manufacturers, essentially undoing the very energy reforms the proposal is designed to advance. The purpose of this study is to estimate the size of the tax burden from these proposed Section 199 changes—both for the nation as a whole and for individual U.S. states—and illustrate the impact these tax changes may have on employment, earnings and economic output throughout the U.S. economy.

The remainder of this study is organized as follows. Section II provides a brief overview of the Section 199 deduction and how it lowers corporate tax liabilities for U.S. companies. Section III presents state-by-state estimates of the tax burden from the “Gang of Ten” proposal. Section IV outlines state-by-state estimates of the impact of these tax burdens on employment, household earnings and economic output. Last, Section IV explains the methodology and data sources used in this study.

II. Overview of the Section 199 Deduction

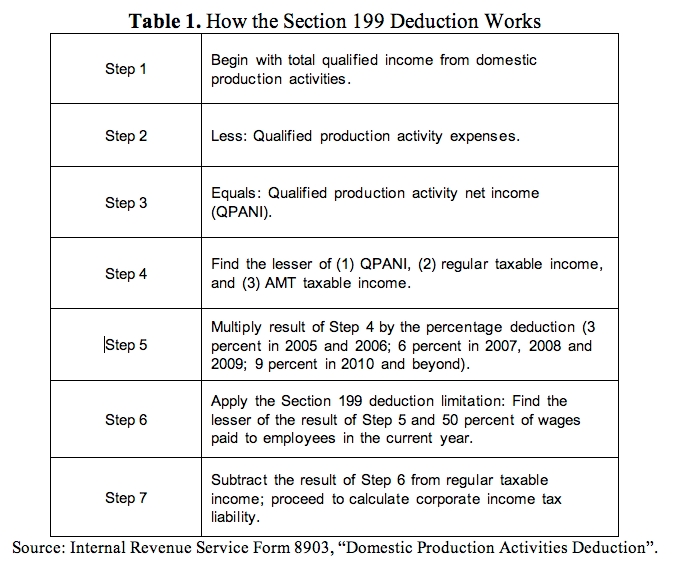

Section 199 of the Internal Revenue Code provides an income tax deduction for domestic manufacturers. The deduction was enacted as part of the American Jobs Creation Act of 2004 in response to an earlier World Trade Organization ruling that the U.S.’s “extraterritorial income exclusion” (ETI) violated international trade laws. The ETI was meant to relieve the disadvantage imposed on U.S. export industries by relatively high U.S. corporate tax rates in their competition with foreign producers. To alleviate the impact on U.S. exporters of repealing the illegal provisions, Congress enacted a new Section 199 business tax deduction known as the “domestic production activities deduction.”

When calculating corporate income taxes, the deduction allows companies to subtract from their taxable income a percentage of income earned from qualified domestic production activities. For oil and gas companies, qualified income includes earnings from oil and gas that is “manufactured, produced, or extracted in whole or in significant part in the United States.” The deduction is equal to 3 percent of qualified income for 2005 and 2006, rising to 6 percent in 2007, 2008 and 2009, and 9 percent in 2010 and beyond. The amount of the deduction is capped at 50 percent of wages paid by the company in that year.

According to the Congressional Budget Office, the Section 199 deduction substantially reduces marginal tax rates for qualified U.S. manufacturers. When fully implemented, the deduction effectively lowers the current federal marginal corporate tax rate from 35 percent to 31.85 percent. This rate would more closely match the average rate now in place for industries in nations of the Organization of Economic Cooperation and Development with which U.S. industries, including our oil and gas industries, compete.

According to IRS figures, total Section 199 deductions totaled $9.34 billion in 2005, the latest year for which data are available. Of this amount, roughly $1.86 billion, or 20 percent, was from companies in the petroleum and coal products manufacturing industry. Assuming this income was instead taxed at the top corporate tax rate of 35 percent, complete repeal would increase tax liabilities for these firms by $652 million per year. This order-of-magnitude calculation provides a rough sense of the size of the tax changes implied by the “Gang of Ten” proposal.

Table 1 summarizes how the Section 199 deduction for domestic production activity is calculated by companies on IRS Form 8903.

III. Estimating Tax Burdens from the Proposed Section 199 Changes

By excluding oil and gas companies from the Section 199 deduction, the “Gang of Ten” proposal would increase U.S. corporate tax burdens. As a result, the first step in estimating the impact on households is to develop a theory of incidence for the corporate income tax.

Companies remit corporate income tax payments, but economic theory suggests the ultimate burden falls on individuals in the form of higher prices for consumers, lower wages for workers, and poorer investment returns for owners of capital. To estimate the tax burden of the proposed changes, we must first estimate how the burden will be split among these three groups in the economy.

Many previous studies have estimated the incidence of corporate taxes. In a seminal 1962 study, economist Arnold Harberger examined a closed U.S. economy with no international trade, no capital flows across borders and a fixed stock of domestic capital. In such a world, domestic owners of capital cannot easily escape corporate tax burdens. Harberger famously concluded that under these assumptions domestic owners of capital bear 100 percent of the corporate tax burden, with none falling on workers or consumers.

More recent research on corporate tax incidence has incorporated more realistic “open economy” assumptions that reflect the growing worldwide mobility of capital in recent decades. In these models, domestic capital is no longer assumed to be fixed in size or internationally immobile. When companies can shift capital across borders in response to differences in labor costs, regulations, taxes and other factors, they are able to shift some of the corporate tax burden onto others in the economy—specifically, domestic workers.

In a 2006 working paper from the Congressional Budget Office, William C. Randolph estimated, based on an open-economy model with reasonable parameters for the U.S. economy, that roughly 70 percent of the U.S. corporate tax burden is borne by domestic workers and 30 percent is borne by domestic owners of capital. Similar results have also been found by subsequent empirical studies of international corporate tax incidence, with domestic workers bearing a significant fraction of corporate tax burdens.

In this study, we adopt the more recent open-economy approach to corporate tax incidence. Following the results from Randolph (2006), we allocate 70 percent of the burden of corporate tax changes to domestic workers in the form of lower earnings, and 30 percent to U.S. shareholders in the form of lower stock returns.

A. Estimating the Revenue Impact

Although the “Gang of Ten” proposal had not been formally introduced in the Senate at the time of this writing, several previous bills have included similar language modifying the Section 199 deduction to exclude domestic oil and gas companies. By analyzing the official revenue scoring of these similar bills, we can approximate the revenue impact of the proposed changes.

The most recent similar bill is H.B. 5351, the “Renewable Energy and Energy Conservation Tax Act of 2008.” The bill would eliminate the Section 199 deduction entirely for major integrated oil companies, and freeze it at 6 percent for companies in all industries. Under current law, the deduction would otherwise increase to 9 percent in 2010.

According to estimates from the Joint Committee on Taxation, the Section 199 changes in H.B. 5351 would raise $13.57 billion over the 10-year period from 2009 to 2018. Because of the similarity between this bill’s provisions and the “Gang of Ten” proposal, we use this revenue scoring as the basis for the tax burden and economic impact estimates in this study.

B. Estimating the U.S. Tax Burden

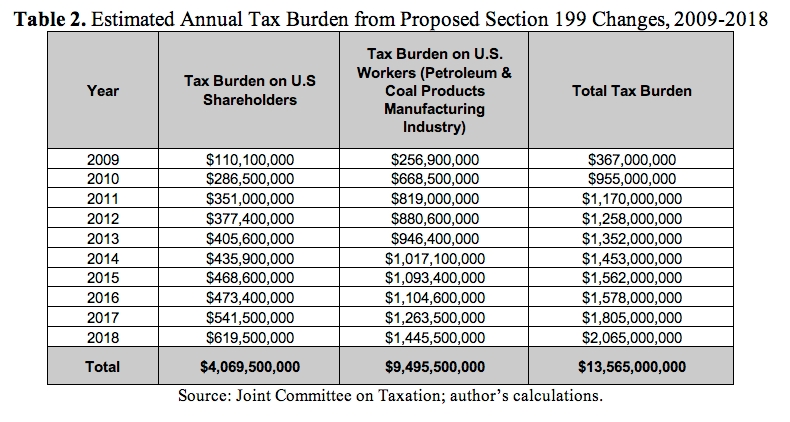

Estimates of the annual tax burden on U.S. households from the proposed Section 199 changes are presented in Table 2. Over 10 years, we estimate the proposed changes will increase corporate tax burdens by approximately $13.57 billion.

Of the total, approximately $9.50 billion is estimated to fall on workers in the petroleum manufacturing industry in the form of lower wages, and $4.07 billion is estimated to fall on U.S. shareholders in the form of lower investment returns. In this way, the proposed changes would deepen the economic pain Americans are feeling due to the energy crisis, rather than alleviating it.

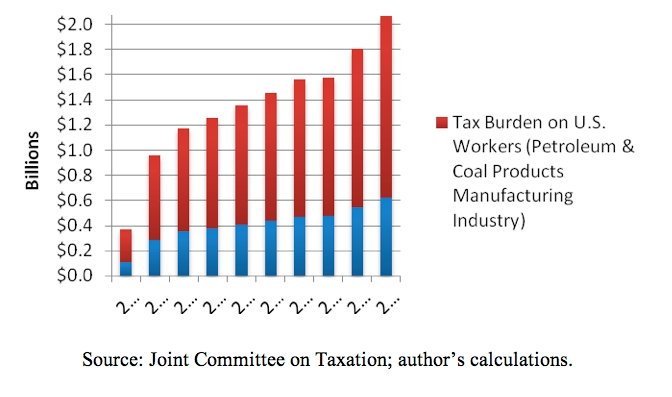

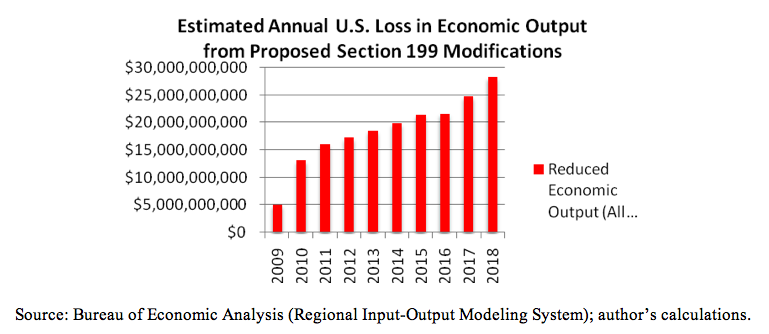

Figure 1 presents the annual tax burden estimates graphically, illustrating the year-by-year tax burden on U.S. workers and shareholders. The proposed changes are estimated to raise $367 million in 2009, increasing each year until reaching a peak of roughly $2.07 billion in 2018.

Figure 1: Estimated Annual Tax Burden on Labor and Capital from the Proposed Section 199 Changes

C. Estimating State-by-State Tax Burdens

As with most federal tax changes, some U.S. states and regions would be more heavily affected by the proposed Section 199 changes than others. In general, the geographic spread of tax burdens tends to follow the economic incidence of the tax. In the case of the proposed Section 199 changes, the portion of the tax borne by workers will tend to cluster in states with heavy concentrations of households working in the petroleum manufacturing industry. Similarly, the portion borne by owners of capital will tend to cluster in states with large numbers of households with investment income.

Using state-by-state data on the earnings of petroleum manufacturing workers from the Bureau of Economic Analysis and state-level data on investment earnings from the IRS, we can estimate the geographic distribution of the proposed Section 199 changes.

Table 3 presents a state-by-state breakdown of the tax burden from the “Gang of Ten” proposal. As is clear from the table, the tax burden on labor is heavily concentrated in the nation’s largest petroleum manufacturing states: Texas, California and Louisiana. Fifty-three percent of total U.S. earnings in the petroleum and coal manufacturing industry are earned by workers in these states. As a result, households in Texas, California and Louisiana will bear a disproportionate share of the tax burden on labor.

Conversely, the tax burden on capital from the proposed changes is heavily concentrated in upper-income states with the largest reported investment incomes. California, Florida and New York are estimated to bear the heaviest capital burden. Households in these states consistently report the nation’s largest investment incomes on IRS tax returns and are therefore estimated to bear the largest share of the tax burden on capital.

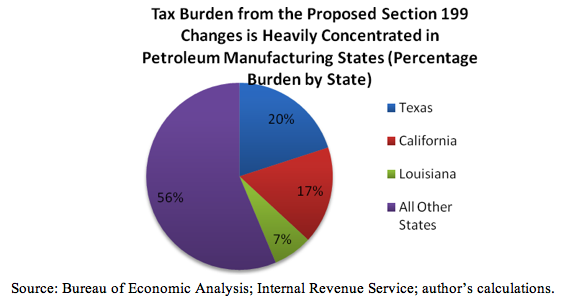

As expected, the total tax burden from the proposed changes is concentrated in the nation’s largest petroleum manufacturing states. As illustrated in Figure 2, America’s three largest petroleum manufacturing states—Texas, California and Louisiana—bear approximately 44 percent of the overall tax burden from the proposed changes. The remaining 47 states and District of Columbia share 56 percent of the overall tax burden.

Figure 2: Texas, California, and Louisiana Bear an Estimated 44 Percent Tax Burden from the Proposed Section 199 Changes

IV. Estimating the Impact on Jobs and the Economy

In Section III we estimated the tax burden from the proposed Section 199 changes. In this section, we use a simple input-output model to analyze the economy-wide impact of those tax burdens on jobs, household income and economic output.

A. Overview of Input-Output Multipliers

Using input-output analysis, it is possible to illustrate how an initial change in demand, earnings or employment in one industry or region will affect demand, output, jobs and earnings in other industries throughout the economy.

Input-output analysis begins with an accounting framework that divides the U.S. economy into distinct industries. Each industry buys inputs from itself and other industries, combines them with value-added, and sells the resulting products to other industries as inputs or to consumers, governments and the rest of the world. This economic linkage between input, outputs, value-added and demand is summarized by an input-output table—also known as a “Leontief table” after the 1973 Nobel Laureate Wassily Leontief.

One of the most common uses of input-output analysis is to estimate the regional “multiplier effect” from a policy change. For example, the impact of closing a $100 million per year military base is larger than $100 million dollars for the affected region. The reason is simple: military bases purchase large amounts of food, fuel and other supplies from companies in the area. Closing the base cuts jobs, earnings and output in these supplying industries as well. The total economic impact therefore includes the direct impact of the base closing as well as the indirect impact felt by complementary local industries.

The most widely-used regional input-output multipliers are the “Regional Impact Modeling System” (RIMS II) from the Bureau of Economic Analysis. RIMS II multipliers are derived from the official U.S. national input-out tables. They allow users to model the overall economic impact of any initial change in household earnings, employment or final demand.

Part of the tax burden from the proposed Section 199 changes falls on households in the form of lower wages. This additional tax burden can be modeled as a reduction in household earnings in the petroleum manufacturing industry. Using the state-by-state tax burden estimates from Section III, we model the total economic impact of the proposed Section 199 changes on jobs, household earnings and economic output.

Because input-output tables assume static relationships in the economy, the following estimates should be treated with caution and should only be considered order-of-magnitude estimates. A more detailed computable general equilibrium approach that accounts for industry and labor market responses to the Section 199 changes is beyond the scope of this study.

B. Total U.S. Economic Impact

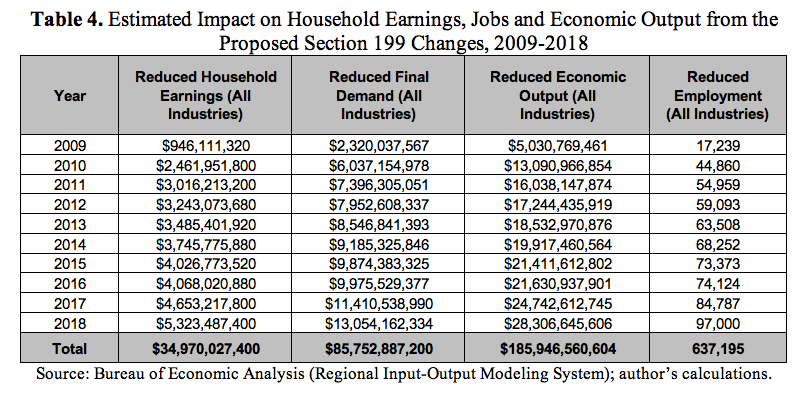

Estimates of the total economic impact of the proposed Section 199 changes are presented in Table 4. As earnings of workers in the petroleum manufacturing industry are depressed by the proposed tax increase, final demand in other industries is also depressed. This reduction in final demand has a corresponding impact on employment, household earnings, and total economic output in industries throughout the economy.

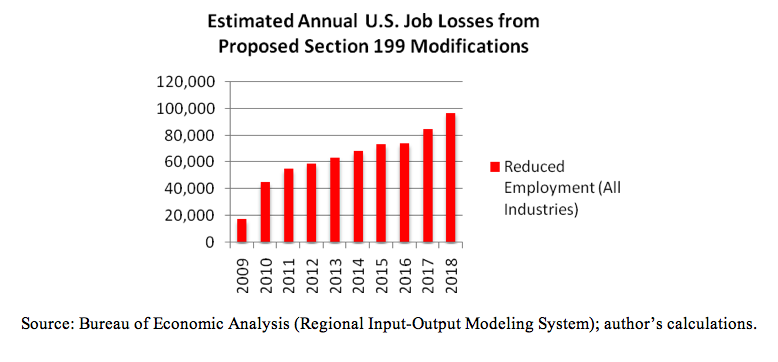

Overall, the proposed changes are estimated to reduce U.S. employment by approximately 637,000 jobs over 10 years. Compare that figure to the 966,000 jobs lost due to mass layoffs in 2007, as reported by the Bureau of Labor Statistics. Put differently, the estimated 10-year job losses from the proposed changes are equivalent to two-thirds of the annual job losses for the U.S. economy as a whole. Job losses represent an even higher cost borne by Americans for this change in energy policy.

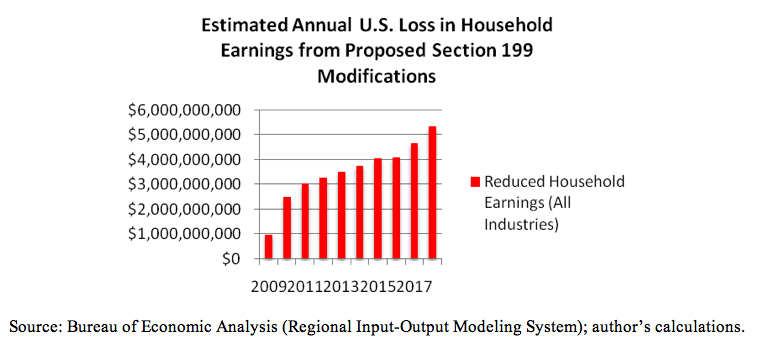

In addition to employment effects, the proposed changes are estimated to reduce household earnings across all U.S. industries by $34.97 billion over 10 years, or roughly $330 per U.S. household. Taking the impact on all U.S. industries into account, the proposed changes are estimated to reduce total economic output by $185.95 billion over 10 years.

Increasing the tax burden carried by U.S. energy companies is likely to further decrease domestic oil production relative to world production. Since America’s energy demand is forecast to grow 34 percent in the next two decades, any hindrance to domestic production will increase U.S. dependence on imported oil, including petroleum from politically unstable regimes such as Venezuela, Nigeria and Russia. Currently, the U.S. produces 5.1 million barrels of oil per day, which meets less than 25 percent of the nation’s energy demand. The impact of the Section 199 changes is likely to further reduce the nation’s capacity to meet its own energy demands and will further increase its reliance on imported oil. To the extent that the U.S. relies on unstable political regimes for imported oil, the proposed tax plan increases risk for both U.S. energy markets and national security.

Figures 3, 4 and 5 illustrate graphically the year-by-year economic impact of the proposed changes on employment, household earnings and economic output. In general, the magnitude of the annual impacts mirrors the pattern of the original revenue estimates from the Joint Committee on Taxation, which shows relatively small impacts in 2009 rising to the largest impacts in 2018.

Figure 3: Estimated Reduction in U.S. Employment from Proposed Section 199 Changes

Figure 4: Estimated Reduction in U.S. Household Earnings from Proposed Section 199 Changes

Figure 5: Estimated Reduction in U.S. Economic Output from Proposed Section 199 Changes

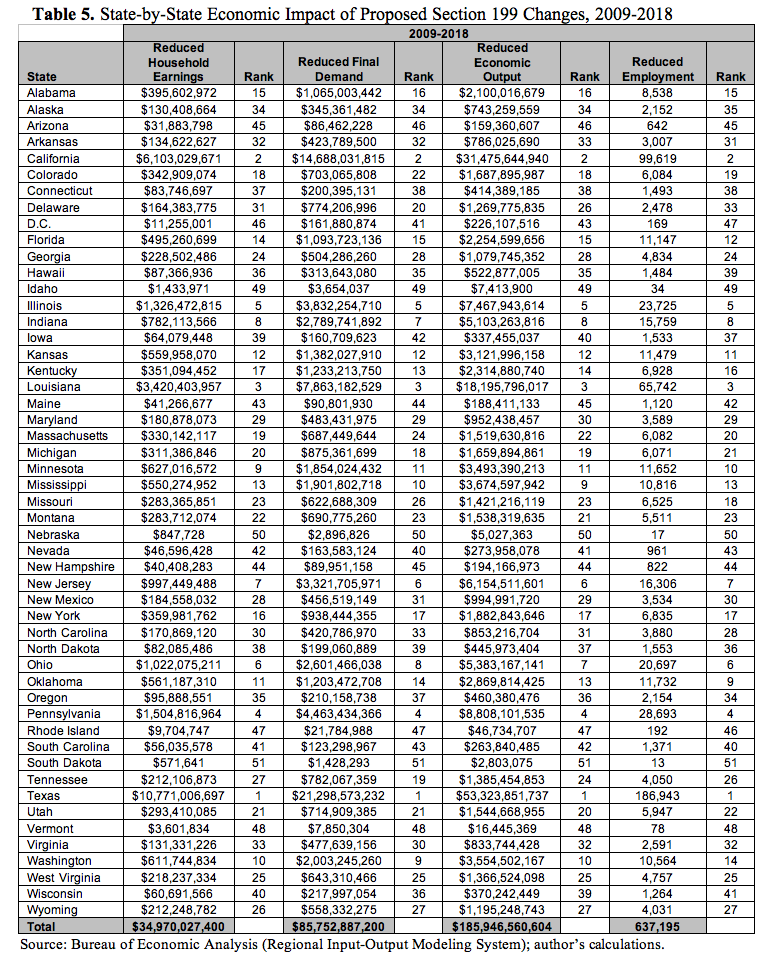

C. State-by-State Economic Impact

In this section we present the state-by-state economic impact of the proposed changes. Using state-level RIMS II multipliers for the petroleum and coal products manufacturing industry and state-level estimates of the tax burden on labor, we estimate the impact on jobs, household earnings and economic output in each state.

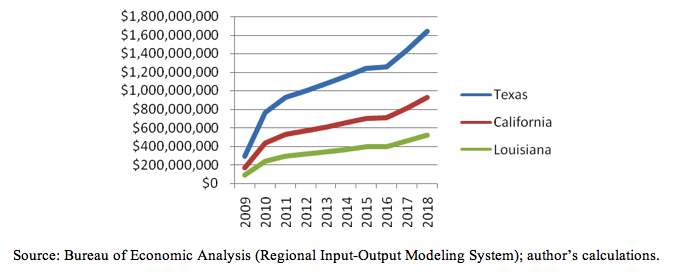

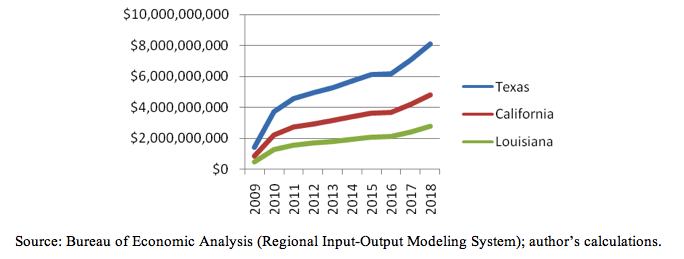

Table 5 presents state-by-state economic impacts of the proposed changes. As with the tax burden estimates of from Section III, states with large petroleum manufacturing sectors would face the largest declines in employment, earnings and output from the proposed changes. Texas alone is estimated to lose roughly 186,900 jobs over 10 years, with California losing 99,600 and Louisiana losing approximately 65,700.

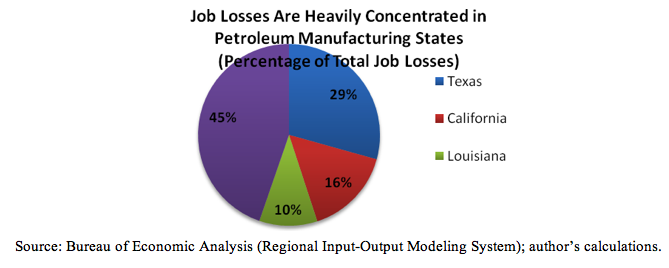

Figure 6 illustrates the concentrated geographic impact of the estimated job losses. Texas, California and Louisiana alone would bear roughly 55 percent of total U.S. job losses from the proposed changes. This is largely the result of the heavy concentration of households employed by the petroleum manufacturing industry in these coastal states. The other 47 states and the District of Columbia collectively share just 45 percent of the estimated job losses.

Figure 6: Texas, California and Louisiana Bear an Estimated 55 Percent of the Job Losses from Proposed Section 199 Changes

The impact of the proposed changes on household earnings and total economic output is similarly concentrated in the nation’s largest petroleum manufacturing states of Texas, California and Louisiana. The combined decline in economic output in these three states reaches nearly $103 billion over 10 years, or 55 percent of the U.S. total. Similarly, these three states bear 58 percent or $20.3 billion of the nation’s total $34.97 billion loss in household income from the proposed Section 199 changes.

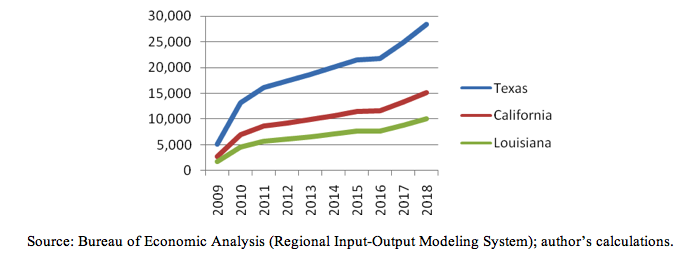

Figures 7, 8 and 9 illustrate graphically the annual impact on jobs, household earnings and economic output in the three most heavily affected states of Texas, California and Louisiana.

Figure 7: Estimated Annual Job Losses in Texas, California and Louisiana from Proposed Section 199 Changes

Figure 8: Estimated Annual Loss of Household Earnings in Texas, California and Louisiana from Proposed Section 199 Changes

Figure 9: Estimated Annual Loss of Economic Output in Texas, California and Louisiana from Proposed Section 199 Changes

As expected, the least affected states in Table 5 are those with relatively low investment earnings, few workers in the petroleum manufacturing industry, or both. South Dakota, Nebraska and Idaho are the least affected states overall, losing a combined 64 jobs and $2.9 million in household earnings over 10 years.

V. Conclusion

One of the goals of the New Energy Reform Act of 2008 is to make the U.S. less dependent on foreign sources of oil. However, by increasing corporate tax burdens on the U.S. oil and gas industry, the revenue offsets in the plan are unlikely to do so. Along with the impact on jobs and investment, the proposed repeal of the Section 199 deduction will likely shrink domestic production of oil and gas relative to world production, making the United States more dependent on imported oil from foreign sources, including politically unstable regimes such as Venezuela, Nigeria and Russia.

Because the proposed Section 199 will increase U.S. corporate tax burdens, investment in U.S. businesses is likely to decline relative to growing investment abroad. To the extent that repealing the Section 199 deduction specifically discourages domestic energy production and shifts capital from the domestic industry to companies overseas, the repeal will boost foreign production relative to U.S. production.

The United States currently produces less than one quarter of the oil required to meet its own energy demands. With America’s energy demand forecast to grow 34 percent in the next two decades, any reduction in domestic oil production would further increase U.S. reliance on imported oil; many sources of which are increasingly unstable, weakening U.S. energy security.

The “Gang of Ten” energy proposal also aims to offset the cost of its alternative energy subsidies and tax credits with revenues gained through the repeal of Section 199 for the oil and natural gas industry. However, an examination of the total economic costs of that repeal suggest the losses in household earnings alone would total roughly 2.6 times the benefit the federal government would derive from the increased revenues.

The proposal is also costly in terms of domestic jobs that will be lost, particularly in the oil-producing states in the Gulf Coast region. But it is worth noting the mechanism influencing this unemployment. The primary reason for the projected job loss stems from investment dynamics. Investors allocate their resources to maximize returns. Industries that are increasingly burdened by domestic corporate income taxes attract fewer investors, reducing employment, productivity and wages for workers in those industries.

If Congress aims to reduce America’s reliance on imported oil from foreign suppliers, legislation that increases corporate tax burdens on the domestic oil and gas industry is unlikely to achieve that goal. Levying punitive taxes on U.S. oil companies by repealing Section 199 is likely to reduce investment in the industry, providing an economic advantage to overseas suppliers, and increase U.S. reliance on imported oil. As illustrated above, the policy is also likely to have a significant negative impact on U.S. jobs, household earnings and economic output.

VI. Methodology and Data Sources

Revenue estimates of the proposed “Gang of Ten” changes to Section 199 are based on the Joint Committee on Taxation’s estimate of the revenue impact of the Section 199 changes in H.B. 5351, the “Renewable Energy and Energy Conservation Tax Act of 2008.”

To divide this tax burden between labor and capital, researchers used the estimate of domestic corporate tax incidence from Randolph (2006), allocating 70 percent to labor and 30 percent to capital. Allocation of the capital burden to states was derived from 2006 IRS Statistics of Income Tax return data for net capital gains and ordinary dividend income reported by state. Allocation of the labor burden to states was based on Bureau of Economic Analysis data on state-by-state household compensation for the petroleum and coal products manufacturing industry.

To generate estimates of economic impact on employment, household earnings and economic output, researchers modeled the tax burden on labor as an earnings reduction for households in the petroleum and coal products manufacturing industry (NAICS code 3240). Because of uncertainty of the input-output impact of reduced household capital earnings, the capital portion of the tax burden is excluded from the economic impact analysis. As a result, the impact estimates presented in this study should be considered conservative lower-bound estimates.

Using BEA RIMS II multipliers for the petroleum and coal products manufacturing industry, researchers calculated the impact on final demand, output and employment from an initial reduction in household earnings in the petroleum manufacturing industry. First, the final demand multiplier for earnings was divided by the direct-effect multiplier for earnings, which gave the change in earnings per dollar of final demand. Next, the initial change in household earnings was divided by the change in earnings per dollar of final demand, yielding the change in final demand associated with the initial change in earnings. This change in final demand was then used to calculate the impact on earnings, employment and total output.