Last summer I testified before a Senate subcommittee on the numerous problems with the estimates issued by the Administration’s Working Group on the Social Cost of Carbon. The Working Group’s estimates of the “social cost of carbon” were artificially inflated because of several modeling decisions that it made, including the very significant omission of a 7 percent discount rate as OMB (the regulatory overseers within the White House) requires (as I explain here).

In the current post, I walk through another quirk in the Working Group’s procedure, which ends up yielding a very counterintuitive result: The richer we expect our grandchildren will be, the more the Working Group’s approach would impoverish ourselves today on their behalf. This is just another example of how the Working Group’s use of computer simulations ends up producing a nonsensical outcome.

Background: The “Damage Functions” in Computer Models

The Obama Administration’s Working Group chose three computer models from the economics of climate change literature—specifically, the DICE, FUND, and PAGE models—in order to estimate the social cost of carbon (SCC). The SCC is supposed to represent the present discounted value (in dollar terms) of the net harms that an additional ton of emitted CO2 will wreak on humanity over the coming centuries, because of climate change.

As we explained in this post, these computer models use a “damage function” that transforms temperature increases into an estimated percentage reduction of future GDP. In other words, the models don’t take a stipulated amount of warming—let’s say 3 degrees Celsius by the year 2100—and then directly spit out such-and-such trillions of dollars (at that time) in forecasted damages from climate change. Instead, the computer models have different estimates of the fraction of the potential economic output that will be forfeited in the year 2100, if humans allow (say) 3 degrees Celsius of cumulative global warming.

Combining Damage Functions With Growth Forecasts

In our earlier post, we quoted from an MIT professor who explained that this approach to the computer models’ “damage functions” was based on arbitrary mathematical relationships that had no basis in theory or empirical observation. However, for our purposes now, there is a separate problem: Since the damage functions are expressed as a fraction of global GDP, it means that the actual dollar value of estimated future damages from climate change are proportional to the forecast for economic growth. This will lead to an absurd outcome, but to see why we need to develop the logic of the Working Group’s output.

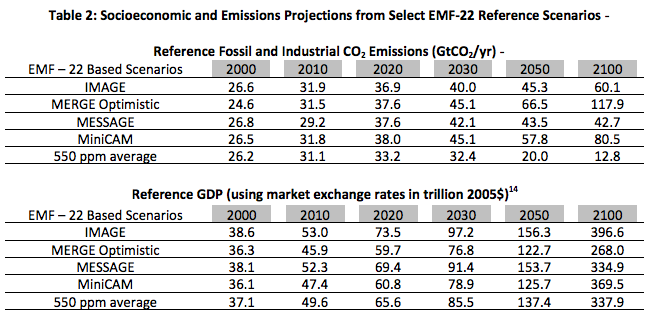

First let’s walk through (a portion of) Table 2 from the Working Group’s 2010 report:

The portion of Table 2 that we have reproduced shows the different scenarios that the Working Group used when forecasting the trajectory of global CO2 emissions and economic growth. There are several different scenarios with interesting names (“MERGE,” “IMAGE,” etc.), the last of which shows what would be needed to maintain average atmospheric concentrations of CO2 at 550 parts per million (ppm).

For our purposes in the present blog post, let’s just focus on the MERGE scenario in Table 2. Notice that by the year 2100, there is far greater annual emissions of CO2 in MERGE than in any other scenario; the MERGE scenario projects 117.9 gigatons of emissions in the year 2100, while the second-highest scenario (MiniCAM) projects only 80.5 gigatons, a level that is only 68 percent as high as emissions in MERGE.

On the other hand, if we look at the second section in Table 2, we see that MERGE has by far the smallest growth in total economic output. By the year 2100, the MERGE scenario projects global GDP of $268 trillion (in 2005$), while the second-lowest is MESSAGE at $334.9 trillion, which is about 25 percent higher than economic output under MERGE.

So let’s put these two facts together: Relative to all of the other scenarios, the MERGE scenario assumes much higher growth in global CO2 emissions over the coming decades, while it simultaneously projects that people in the future will be much poorer.

Intuitively, what would we expect the “optimal” approach to carbon policy to look like, across these various scenarios? Since more emissions leads to higher global temperatures, and since global climate change damages grow worse more than proportionally as the temperature increases (in the simulated world of the models), we would expect the damage inflicted on humanity under the MERGE scenario to be far worse than in the other scenarios.

At the same time, because the MERGE scenario assumes our descendants in future generations will be much poorer than in any of the other scenarios, we who are alive today ought to be willing to sacrifice more of our economy in order to help them. Remember that the conventional wisdom calls for limiting carbon dioxide emissions in the near-future, thereby making us poorer, in order to spare our grandchildren from excessive climate change damages. The richer our grandchildren will be, therefore, the less willing we should be to sacrifice our wealth in order to make them even richer.

Putting these two intuitive notions together—that under the MERGE scenario, (1) there will be far more human-caused global warming, and (2) our descendants will inherit a much smaller baseline economy—we would expect that government policy today would penalize carbon-intensive activities the most under the MERGE scenario, compared to the other scenarios. In particular, since the whole point of the Working Group is to generate “social cost of carbon” (SCC) estimates to guide policymakers, we would expect that the SCC would be highest under the MERGE scenario.

Working Group Gives the Opposite Result

To review: In the previous section, we established that of the various scenarios the Working Group plugged into its three representative computer models, the “MERGE” scenario assumed (by far) the highest level of CO2 emissions, and the slowest pace of baseline conventional economic growth.

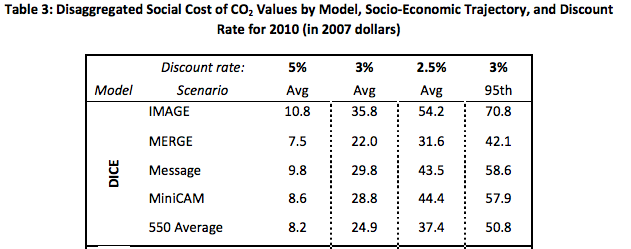

Intuitively, we therefore would expect the Working Group to recommend placing the most pressure on scaling back emissions today for the MERGE scenario, relative to the others. Since the SCC represents the “benefit” of cutting back on a unit of emissions, that means we intuitively expect the Working Group to report the highest values of the SCC (for a given discount rate) for the MERGE scenario, compared to the others. And yet, as Table 3 (again taken from the Working Group’s 2010 report) shows below, the opposite holds true:

As Table 3 shows, MERGE has the lowest estimated social cost of carbon (SCC) for a given discount rate, among all of the scenarios that the Working Group considered. For example, using a 3 percent discount rate, MERGE estimated an SCC of $22/ton, which was lower than the $24.90/ton corresponding to the 550ppm scenario—in which emissions (eventually) fall off drastically, limiting total global warming and thus (at least one would have thought) containing the impact of climate change.

The Mystery Explained

What is going on here? How could the Working Group’s procedure be spitting out results that seem to be the opposite of common sense?

A big part of the answer is that the “damage functions” of the three computer models don’t project actual monetary damages from, say, rising sea levels or worse crop yields. Instead—to repeat what we said earlier—they model the impact of global warming as a percentage of lost potential global GDP. Therefore, other things equal, because the MERGE scenario projects much slower economic growth, the future damages from climate change—when measured in absolute dollars—will of course be much lower than in the other scenarios, where baseline absolute global GDP is so much higher.

In principle, the economic analyst could account for this subtlety by appropriately adjusting the discount rate. In other words, the richer we think people will be in the year 2100, the higher the discount rate we should apply to damages (measured in 2100 dollars) they suffer from climate change, in order to decide how much we should be prepared to sacrifice today on their behalf.

Unfortunately, in practice arguments over the discount rate occur in a separate compartment. For (a spurious) “consistency,” most analysts would probably look at Table 3 above and think that we have to pick a given discount rate, then move down the relevant column to read off the various estimates of the SCC under various scenarios.

Yet as we have explained, such a move is illegitimate. If we change the scenario, then we are changing the assumptions about economic growth, and thus should alter our choice of discount rate accordingly.

Conclusion

If we take the framework of the Working Group on the Social Cost of Carbon at face value, we would intuitively expect that a scenario involving more emissions and slower (baseline) economic growth would imply the most aggressive action against emissions today. On the flip side, we would expect a scenario involving modest emissions and robust economic growth to imply modest impediments to emissions today, because our grandkids won’t have as big a climate change problem to deal with, and they will be so much richer than us.

Yet as we explained in this post, the actual procedure used by the Working Group (and those who follow their recommendations) yields the opposite outcome: It generates the lowest estimates of the social cost of carbon for the scenario where—according to the logic of the exercise—we would want to see the highest estimates. This is just another example of how, in practice, the Working Group on the Social Cost of Carbon is generating outputs that defy common sense.