Abstract

Various legislative and other proposals have promoted policies that would tax or place a price floor on petroleum-based transportation fuels such as gasoline because as President Obama stated in his recent address, “we’re running out of places to drill on land and in shallow water.”[1] Their object is to spur conservation and promote the manufacture of more efficient vehicles, as well as reduce greenhouse gas emissions, increase national security (by lessening our dependence on foreign oil), and decrease congestion. But such policies assume that oil is unduly scarce, even though current worldwide oil reserves are the highest ever. And reserves are only a fraction of potential oil resources, not to mention that technology is continually unlocking new resources. Moreover, as the experience of Europe has shown, setting an artificially high price for petroleum-based transportation fuels will not change the growth of U. S. carbon dioxide emissions, which are the largest component of greenhouse gas emissions. In any case, lessened U.S. carbon dioxide emissions would be dwarfed by future increases in those emissions from developing countries, particularly China, making unilateral action problematic.

Introduction

Numerous policy proposals advocate higher prices on gasoline and other transportation fuels in order to spur conservation by both producers and consumers. Advocates of such policies believe that charging customers a “fair” or “socially optimal” price for their use of a “depleting fuel” will promote the manufacture of more efficient vehicles and foster consumers’ use of mass transit, carpooling, home relocation, or other fuel-reducing endeavors. An example of such a policy is the tax on gasoline in the American Power Act, a legislative proposal by Senators Kerry and Lieberman to reduce greenhouse gas emissions.

Another proposal appears in a paper by Thomas Merrill and David Schizer,[2] where they advocate a plan that would both increase the stability of the price of transportation fuels by not allowing them to fall and be revenue neutral. According to the plan, a fee would be added to the price of transportation fuels, and that fee would rise if the price of crude oil fell, but fall if the price of crude oil rose. In theory, this would keep the price of transportation fuels more stable by setting a dynamic floor on the price. In any case, the price of transportation fuels would never fall below the prices they had when the plan was launched, since the fee would keep rising to offset any decline in the price of crude oil. In order to ensure revenue neutrality, and thus to sell the policy politically, the stabilizing fee would not be kept by the government but would be rebated back to citizens, minus administrative costs. The fee, however, would not be rebated back to purchasers but would be distributed to all persons of driving age, so that those who used mass transit or drove less than the average amount would garner a sizable share.

The goals of these policies are to reduce greenhouse emissions, improve national security by decreasing oil imports, and hopefully reduce road congestion. But another reason for promoting such a proposal is to “help the economy adjust to a future of scarce petroleum”. That is simply not an issue, as will be seen below. In addition, as history has shown and as forecasters continue to show, carbon dioxide emissions, the largest component of greenhouse gas emissions, will continue to grow despite increasing crude oil prices and thus despite any such policies.

Global Oil Reserves vs. Oil Resources

Almost as long as people have been using oil, people have been declaring that we are running out of it. Ronald Bailey, science correspondent for Reason Magazine, writes:[3]

Predictions of imminent catastrophic depletion are almost as old as the oil industry. An 1855 advertisement for Kier’s Rock Oil, a patent medicine whose key ingredient was petroleum bubbling up from salt wells near Pittsburgh, urged customers to buy soon before “this wonderful product is depleted from Nature’s laboratory.” The ad appeared four years before Pennsylvania’s first oil well was drilled. In 1919 David White of the U.S. Geological Survey (USGS) predicted that world oil production would peak in nine years. And in 1943 the Standard Oil geologist Wallace Pratt calculated that the world would ultimately produce 600 billion barrels of oil.

During the 1970s, the Club of Rome report The Limits to Growth projected that, assuming consumption remained flat, all known oil reserves would be entirely consumed in just 31 years. With exponential growth in consumption, it added, all the known oil reserves would be consumed in 20 years.

Some other interesting factoids from the past regarding oil depletion are:[4]

- In 1885, the U.S. Geological Survey indicated that there was little or no chance of discovering oil in California.

- In 1914, an official of the U.S. Bureau of Mines estimated total future production at 5.7 billion barrels. (By 1984, more than 34 billion barrels had been produced.)

- In 1920, the Director of the U.S. Geological Survey predicted that the U.S. had nearly reached peak production. (By 1984, production was over four times the 1920 rate.)

- In 1939, the Interior Department predicted U.S. oil supplies would last thirteen years.

- In 1949, the Secretary of the Interior predicted that the end of U.S. oil supplies was almost in sight.

On the other hand, and more currently:

- Edward L. Morse, an energy official in Carter’s State Department, indicates that the world’s deep-water oil and gas reserves are significantly larger than was thought in the 1990s, and high prices have spurred development of technologies for extracting them. The costs of developing oil sands are declining, so projects that were not economic last year with the price of oil under $90 a barrel are now viable with oil at $79 a barrel.[5]

- Daniel H. Yergin, co-founder and chairman of Cambridge Energy Research Associates, writes “careful examination of the world’s resource base . . . indicates that the resource endowment of the planet is sufficient to keep up with demand for decades to come.” [6]

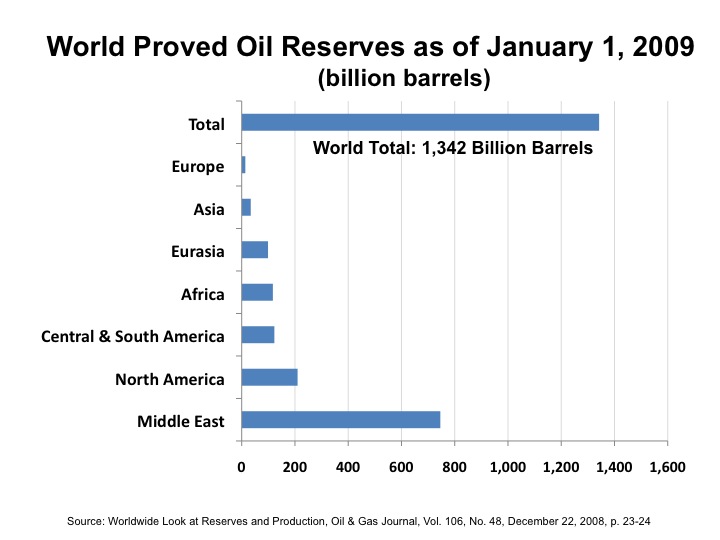

According to the Journal of Oil and Gas, global proved oil reserves as of January 1, 2009, were 1,342 billion barrels,[7] the highest level ever, and about 10 billion barrels higher than in 2008. Thus, enough reserves were found in 2008 to meet demand in that year and to add 10 billion barrels to the global reserve level. The Middle East holds the majority of proved oil reserves at 746 billion barrels,[8] followed by North America with 210 billion barrels. Canada with 178 billion barrels (85% of the North American share)[9] is second in rank only to Saudi Arabia with 267 billion barrels of proved oil reserves.

Proved reserves of crude oil are the estimated quantities that geological and engineering data indicate can be recovered from known reservoirs with existing technology and current economic and operating conditions. That is, they are quantities of oil that can be retrieved by producing companies to meet demand in the near future, without needing new technology or having to explore and develop a totally new oil well. As such, they represent the lowest estimate of petroleum supplies. Estimates of proved reserves are developed from data reported to the U.S. Securities and Exchange Commission,[10] foreign government reports, and international geologic assessments.

Thus, the term ‘proved reserves’ refers to oil deposits that have actually been discovered and carefully estimated. Although it is true that every barrel of oil removed from the ground reduces the physical total by one, the economically relevant fact is that humans historically go out and find more usable oil reserves in order to keep pace with consumption.

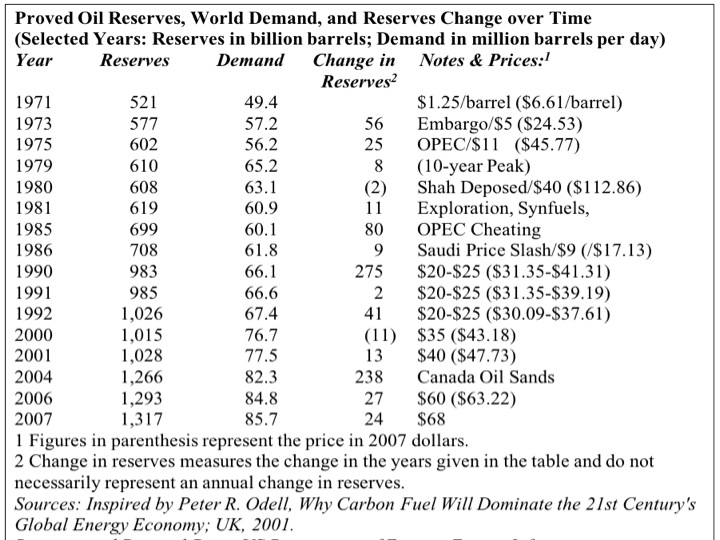

The Institute for Energy Research put together a table of global oil reserves beginning with the year 1971 (when proved reserves were at a level of 521 billion barrels) and continuing through 2007 (when they were at 1,317 billion barrels).[11] Between 1971 and 2007, the world consumed 910.3 billion barrels of petroleum[12], which would have made the reserve total 2,227 billion barrels were they not used. As the table shows, in this 36-year time span, proved oil reserves worldwide have grown by a factor of 2.5, while global oil demand over the same period has grown by a factor of 1.7. Thus, at the 2007 level of global demand, 31.3 billion barrels per year,[13] proved oil reserves were capable of meeting that demand for 42 years. As the table indicates, there have been periods during which global oil reserves have increased more than 200 billion barrels.[14] One such period occurred early this decade with the addition of Canadian oil sands reserves. Currently, the U.S. benefits from these reserves from our northern neighbor, but proposed government policies (such as a low-carbon fuel standard[15] or legislation enacting a cap-and-trade policy on greenhouse gas emissions[16]) could endanger this source of proved reserves, allowing other countries without such policies to benefit instead.

U.S. Oil Resources

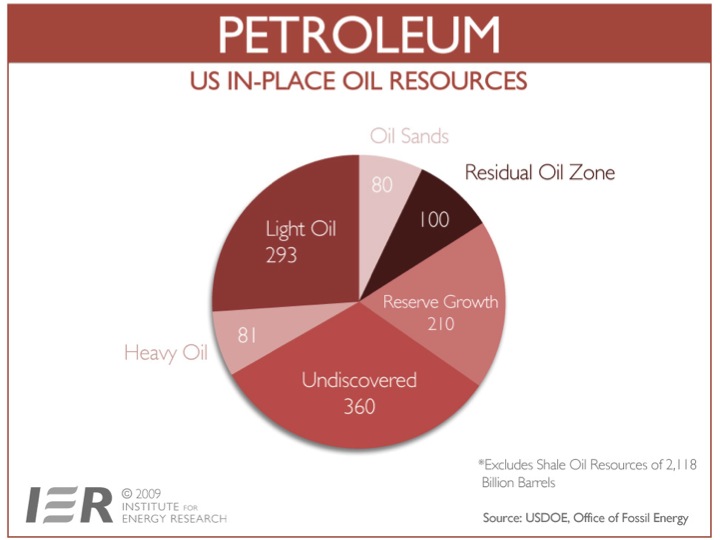

Proved oil reserves are a subset of the oil resource base, which includes estimated quantities of both discovered and undiscovered oil that have the potential of being classified as reserves in the future. These oil resources may be difficult to produce with current technology or their access may be limited by government policy. Thus, new technologies and better government oil recovery policies, as well as “risk mitigation” incentives, could help industry convert the higher-cost, undeveloped domestic oil resources into economically feasible reserves. Access to additional offshore, Alaskan, and public-land resources could be accelerated rather than stalled, as under the current Administration.[17]

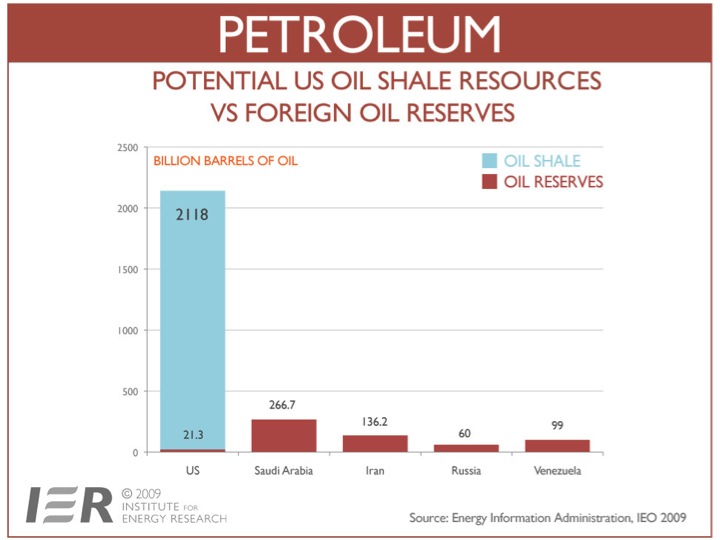

The U.S. Department of Energy estimates that light and heavy oil resources in the United States total 1,124 billion barrels, with 40% believed to be recoverable.[18] In addition, the U.S. has a world-leading 2,118 billion barrels of in-place oil shale,[19] of which 800 billion barrels is estimated to be recoverable.[20] Other estimates have the recoverable shale oil number even higher, at approximately 1.38 trillion barrels.[21] That’s five times the oil reserves in Saudi Arabia.

Oil shale is found largely in Utah, Colorado, and Wyoming, and the best sources are believed to be on public lands. Oil producers need to have access to these resources in order to demonstrate that they can produce shale oil at current prices with technologies they believe will work. However, access is currently being stalled by the owner of the public lands, the federal government. [22]

The Denver Post carried an article that addressed this issue:[23]

Colorado is sitting on a bounty of oil shale that could make energy cheaper in America and free it from the whims of Middle Eastern oil barons. Unfortunately, it looks like oil companies can’t do the work necessary to extract the fuel because of political roadblocks. And this attitude seems to go all the way to the top. Interior Secretary Ken Salazar, one of Colorado’s two U.S. senators until he joined the Obama administration this year, tossed the latest obstacle into the path to progress in February when he canceled leases for oil-shale development in Colorado, Utah and Wyoming. Salazar’s backward thinking is typical of the politicians who embrace environmental hysteria. They seem to despise fossil fuels and want to stop Americans from using them.

Price Stabilization Policy Formulation

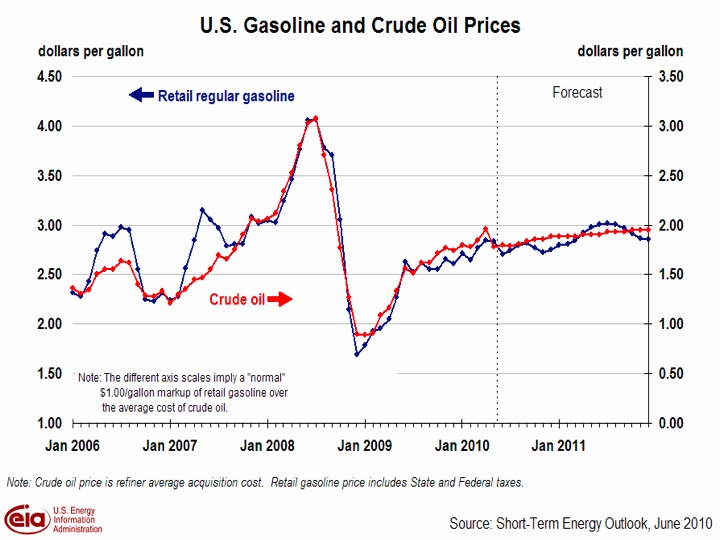

Analysts, such as Merrill and Schizer, who advocate policies that would stabilize transportation fuels, know that they need to make their fee formulation easy to implement and as free of administrative burden as possible. That is why they advocate having the IRS handle the fee: that agency collects the Federal taxes on gasoline. They also advocate that the fee should be based on the price of crude oil, since that is the largest component of the price of transportation fuels and is determined by global forces of supply and demand, making it less amenable to manipulation by domestic producers, refiners, and retailers. But one pitfall in their plan is that the price of the petroleum product does not always follow the price of crude oil, as can be seen by the following chart for gasoline.

The price of gasoline is based on four price components: crude oil, Federal and State taxes, refining operations and profits, and distribution and marketing.[24] In 2008, crude oil represented 69 percent of the gasoline price while the refining component represented only 7 percent. That was not typical of the past 9 years, however, when the refining component represented an average of 15 percent. Generally, there are certain times of the year when the refining component spikes gasoline prices. One example is in the spring, when refiners switch from winter grade gasoline to summer blends. This switch takes place the end of April and in May, causing the price of gasoline to spike, as seen in the chart for the years 2006 and 2007. Another phenomenon that affects the refining component is weather, and in the fall of 2005 the price of gasoline increased because many of the Gulf of Mexico refineries were shut in, owing to hurricane Katrina.

Another factor to note is that a price stabilization policy could in fact inflict a higher fee on petroleum transportation fuels than a likely cap-and-trade policy would provide. For example, if the price stabilization policy had been in effect in 2008, the world oil price increase would have resulted in a fee of about $2.50 per gallon, while according to EIA’s analysis of H.R. 2454, the American Clean Energy and Security Act of 2009, the “tax” on gasoline would have been closer to 35 cents per gallon.[25] Also, as we saw in 2008, the higher prices for petroleum-based transportation fuels had a secondary impact on consumer spending, increasing food prices and other products requiring transportation to move them to market.

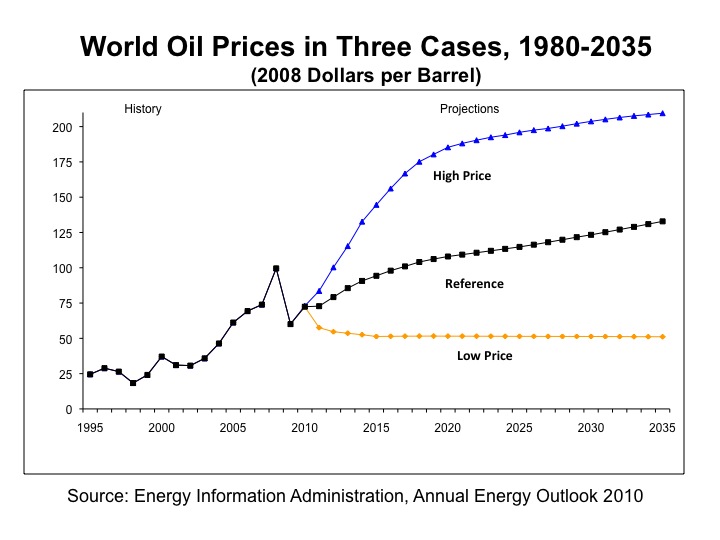

The question remains whether a price stabilization policy or a gasoline tax will have the desired affects of limiting greenhouse gas emissions and increasing national security by reducing oil imports. To evaluate these issues, we’ll examine three oil price scenarios that the Energy Information Administration’s Annual Energy Outlook 2010 forecasts using different prices of crude oil.[26] The cases are the reference case, the high oil-price case, and the low oil-price case. They are depicted in the graph below:

In the reference case, the crude oil price rises gradually, until by 2035 it reaches $133 per barrel (in 2008 dollars), about $60 per barrel more than the current price. In the low price case, the crude oil price decreases to $51 per barrel during the next several years and remains there through 2035, the end of the forecast period. In the high price case, the crude oil price increases to $209 per barrel (in 2008 dollars) by 2035. Both the high price case and the reference case could very well represent a price stabilization scenario since the price of crude oil never falls and steadily rises.

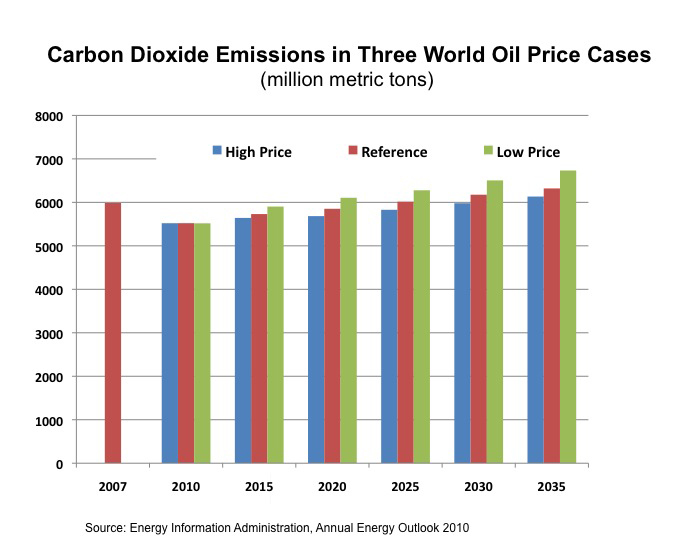

The following graph depicts the carbon dioxide emissions, the largest component of greenhouse gases, in the 3 scenarios. Note that in each of the three cases, U.S. carbon dioxide emissions increase over time and by 2035 range from 2.5 percent to 12.5 percent higher than they were in 2007.

Another way to look at this issue is with the European experience in mind. Since World War II, European countries have had a hefty tax on gasoline to encourage the use of more efficient transportation fuels. Over the past 25 years, carbon dioxide emissions in Europe have ranged between 4,300 and 4,750 million metric tons, and in 2008 they were 5.5 percent higher than in 1983.[27]

The next graph depicts the net petroleum import share for each of the three price cases. The imported amount varies with the demand for liquid fuels, which is dependent on the price of crude oil, and which in 2035 varies by less than 4 million barrels per day across the three cases: 20.8 million barrels per day in the high price case and 24.5 million barrels per day in the low price case.

The petroleum import share also varies with the amount of ethanol production, which is mandated by the Energy Independence and Security Act of 2007 (EISA2007). That Act mandates the production of 36 billion gallons of biofuels, such as ethanol, by 2022.[28] It also requires the sale of flex-fuel vehicles that can burn E85, a blend of 85 percent ethanol and 15 percent gasoline—a much higher percentage of ethanol than the 10 percent blend that conventional gasoline vehicles can safely use without causing damage to the vehicle.

A further factor is the stricter mandates for Corporate Average Fuel Economy. EISA2007 requires the fuel efficiency of the combined fleet of all new passenger cars and light trucks sold in the U.S. in model year 2020 to be equal to or exceed 35 miles per gallon, 34 percent higher than the current fleet average of 26.4 miles per gallon.[29] In none of the three cases are petroleum imports at a level that is independent from foreign oil, and in fact, in none of the cases is the U.S. independent of petroleum imports from non-North American countries. In the high price case, where petroleum imports are the least, the higher oil prices increase the penetration of biofuels and the use of flex fuel vehicles.

World Implications

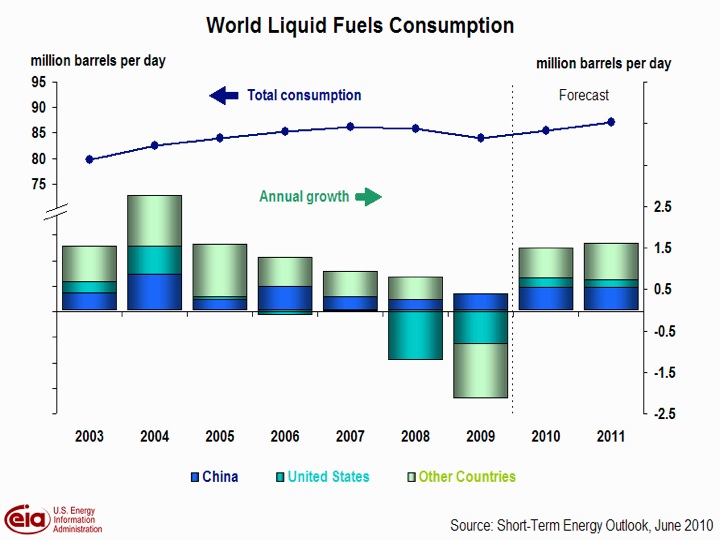

The Energy Information Administration provides forecasts of the next 18 months in their Short-Term Energy Outlook.[30] The next chart shows world demand for petroleum and the annual change in demand for the United States, China, and the rest of the world from 2003 through 2011. In 2008 and 2009, U.S. demand for petroleum declined. However, China’s petroleum demand increased in both 2008 and in 2009, even though the U.S. and the rest of the world’s demand decreased in 2009, and its demand is expected to continue to increase. Thus, any reduction in U.S. petroleum consumption will be made up by China or other countries.

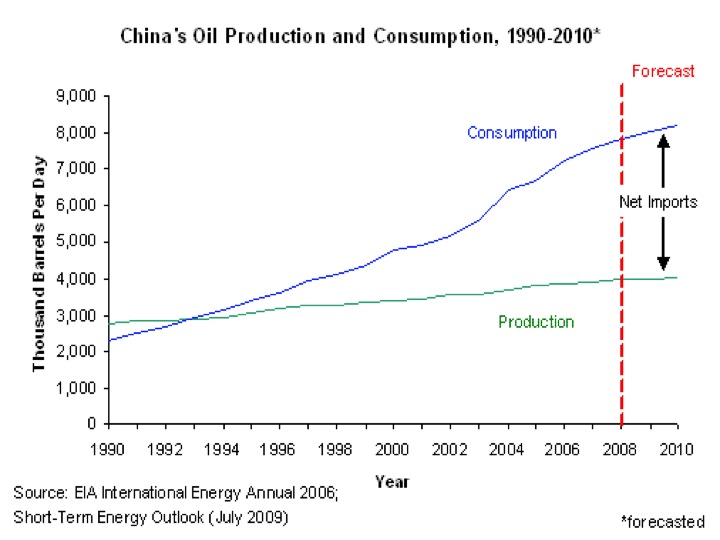

As can be seen from the next chart, China’s domestic oil production is fairly flat, but its oil consumption is increasing at a fast pace, making its reliance on oil imports grow. The growth in oil consumption is primarily to provide for its expanding transportation sector. From 1996 to 2006, growth in the combined length of China’s highways averaged 11.3 percent per year. With this level of highway construction, China is on track to exceed the United States in total highways in the next decade.[31]

Infrastructure projects in China account for 15 percent of China’s gross domestic product, which grew by 8.7 percent in 2009, when the economies of the United States and Europe did not grow at all. Besides highway construction, their inventory projects include almost 100 new airports, some in isolated cities, and dozens of subways.[32]

In 2006, China became the world’s second-largest vehicle market, after the United States, and in 2009, it has overtaken the U.S market in vehicle sales.[33] New passenger car sales rose 55 percent in February of this year from a year earlier, following a 116 percent increase in January, aided by the extension of government incentives to boost purchases of smaller vehicles and spur rural demand for cars.[34]

In 2007, China produced nearly 8.9 million motor vehicles, an increase of 22 percent over production in 2006. The country is now the third largest vehicle producer in the world, after Japan and the United States. According the Energy information Administration, China’s passenger transportation use per capita is projected to triple by 2030.[35]

China is not endowed with a lot of oil resources. Its oil reserves totaled 16 billion barrels in January 2009.[36] As a result, China has spent nearly $200 billion on oil deals during the past few years, joining with more than 19 countries —including Russia, Turkmenistan, Kuwait, Yemen, Libya, Angola, Venezuela and Brazil[37]— and paying for exploration, production, infrastructure construction, as well as “loans for energy” deals.[38] Recently, China’s Sinopec International Petroleum Exploration and Production Company agreed to buy, for $4.65 billion, the 9 percent interest that ConocoPhillips holds in Syncrude,[39] a Canadian business involved in the production of oil sands (an asphalt-like heavy oil). .It is even pursuing buying leases in U.S. waters, in the Gulf of Mexico.[40]

During the first quarter of this year, China set records with huge year-over-year increases in oil demand. In February, China’s oil demand rose 19.4 percent over a year earlier, the second fastest rise on record. China is the world’s second largest oil user (second to the United States).[41] China’s oil imports were up 13.8 percent in March over February, reaching 4.95 million barrels per day, according to preliminary data from China’s General Administration of Customs.[42] In part, these large oil increases are fueling China’s passenger car fleet.

China’s economic and energy profile can be summarized as follows:[43]

- Between 2000 and 2008, China’s real gross domestic product averaged 10 percent per year. While its economic growth in 2008 and in the first half of 2009 is less than this average rate, its $586 billion economic stimulus package is expected to stimulate more normal growth in the second half of 2009 and in 2010.

- China is the world’s most populous country and the second largest energy consumer behind the United States. Rising oil demand and imports have made China a significant factor in world oil markets.

- China is the world’s second-largest consumer of oil behind the United States, and the third-largest net importer of oil after the U.S. and Japan.

- China’s largest oil fields are mature and production has peaked, leading companies to focus on developing largely untapped reserves in the western interior provinces and offshore fields.

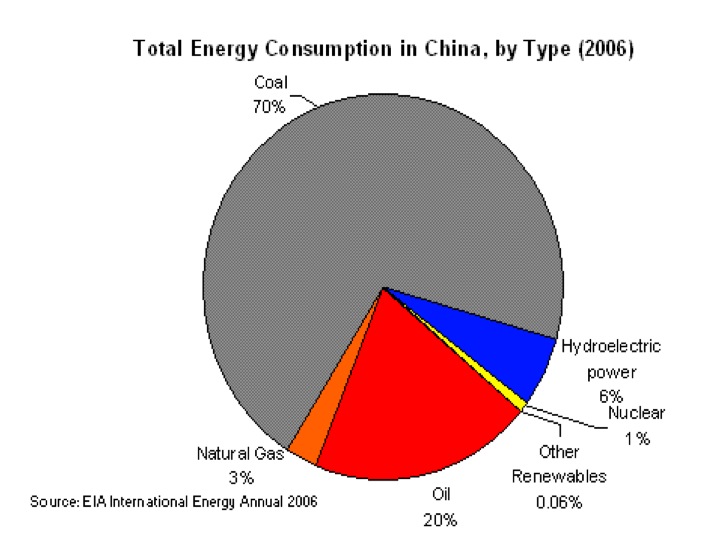

- In 2006, 93 percent of China’s energy consumption was from fossil fuels. (See figure below.)

China is the largest producer and consumer of coal in the world, with 70 percent of its demand for energy coming from coal. In the late 1980s, China surpassed the U.S. in coal consumption and the Energy Information Administration expects China’s coal consumption to be 4.5 times that of the U.S. by 2035.[44] Many of China’s large coal reserves have yet to be developed.

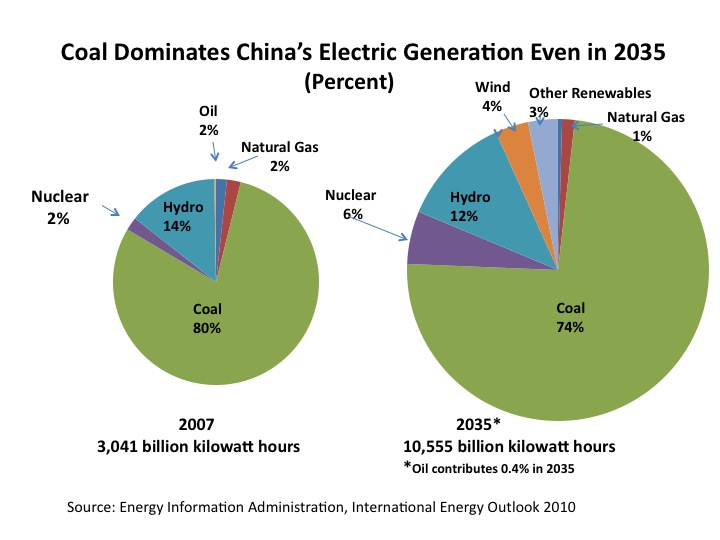

- China’s electricity generation is dominated by fossil fuel sources, particularly coal. In 2007, coal-fired generators produced 80 percent of China’s electricity and the Energy Information Administration predicts that, by 2035, coal-fired generators will produce 74 percent of its electricity, with mainly wind and nuclear power making up the difference in coal’s lower share.[45] (See figure below.)

Because of China’s large population, high economic growth rate, and large consumption of fossil fuels, it is the world’s largest emitter of carbon dioxide, which is the largest component of greenhouse gas emissions. China surpassed the United States in emissions of carbon dioxide in 2006 and is expected to emit over twice as much carbon dioxide than the United States in 2035.

Since 2002, the average annual increase in China’s carbon dioxide emissions has been over 550 million metric tons.[46] In 2009, U.S. carbon dioxide emissions from transportation uses were 1,851 million metric tons.[47] Thus, if China continues its high level of economic growth and its use of fossil fuels as forecast, in just over 3 years, its increase in carbon dioxide emissions will equal the total carbon dioxide emitted from the U.S. transportation sector. Small, incremental changes in U.S. transportation emissions will not have an effect on overall global greenhouse gas concentrations.

And while China has professed that it will meet renewable generation goals, it will not partake in meeting targets for greenhouse gas reductions that will hurt its projected economic growth and its future status as a major world power.[48] Instead, China is willing to make reductions in greenhouse gas intensity (greenhouse gas emissions per unit of GDP), a measure proposed by the U.S. almost a decade ago, that allows for both economic growth and lower emissions per unit of GDP from improved efficiency and technology.[49]

Conclusion

Concerns about traffic congestion, greenhouse gas emissions, and the use of foreign oil are valid concerns, but increasing the price of oil does not do a good job of addressing those concerns. Policies that artificially raise the price of petroleum-based transportation fuels will have the desired effects of limiting usage and reducing demand. But even with the price of crude oil at a $200 per barrel (in 2008 dollars) the U.S. will still increase its carbon dioxide emissions and will still be dependent on non-North American sources of imported oil. Reductions of petroleum demand in the United States will just make crude more available for other countries to use, with little progress in reducing global carbon dioxide emissions.

The U.S. has transitioned to other sources of energy in the past without the need for government policies. The picture below from a 1910 Midwestern town depicts the transition from horse and buggy transportation to the horseless carriage. The smoke from the early autos was felt to be far less polluting than the horse excrement and carcasses on the street. Early autos were noisy and belched smoke, but they kept the streets clean of tons of waste and dead bodies of thousands of horses.[50] Now, of course, technology has improved automobile engines so that they are more powerful, efficient, and cleaner than those of the past, supporting our thirst for increased transportation, better mobility, and a higher quality of life—all at reduced emissions of criteria pollutants. The “ultimate resource” of human ingenuity has indeed improved the economic and environmental characteristics of petroleum.

[1] The Washington Post, Obama presses for action on energy bill, June 16, 2010, http://www.washingtonpost.com/wp-dyn/content/article/2010/06/15/AR2010061505595.html

[2] Thomas Merrill and David Schizer, “Advancing Energy Policy Goals in an Economic Downturn: A Proposed

Petroleum Fuel Price Stabilization Plan”, November, 2009.

[3] Ronald Bailey, “Peak Oil Panic”, May 2006, http://reason.com/archives/2006/05/05/peak-oil-panic

[4] William M. Brown, “The Outlook for Future Petroleum Supplies,” in Julian Simon and Herman Kahn, eds., The Resourceful Earth (Malden, MA: Blackwell, 1984), p. 362.

[5] www.foreignaffairs.com

[6] www.foreignpolicy.com

[7] “Worldwide Look at Reserves and Production,” Oil and Gas Journal, Vol. 106, No. 48, December 22, 2008, pp. 23-24.

[8] Since the Middle East has had a high concentration of global oil reserves for decades, its reserve level is not an indicator of market share.

[9] A large portion of Canadian reserves are oil sands, which cannot be produced at the same rate as conventional oil, so the 178 billion barrels of Canadian reserves are not functionally equivalent to 178 billion barrels of conventional oil.

[10] Companies whose stocks are publicly traded on U.S. stock markets are required to report their holdings of domestic and international proved reserves to the SEC.

[11] Institute for Energy Research, August 26, 2008, www.instituteforenergyresearch.org/2008/08/26/has-oil-reached-its-peak/

[12] Energy Information Administration, Annual Energy Review 2008, Table 11.10, http://www.eia.doe.gov/emeu/aer/pdf/pages/sec11_21.pdf

[13] In 2007, the U.S. demand for petroleum was 20.68 million barrels per day or 7.548 billion barrels per year, approximately one-fourth of the world total. See Energy Information Administration, Annual Energy Review 2008, Table 5.1, www.eia.doe.gov/emeu/aer/petro.html

[14] The increase in Middle Eastern oil reserves in the late-1980s is somewhat controversial and has been questioned by some to be, in part, paper increases.

[15] A Low Carbon Fuel Standard reduces the carbon intensity of transportation fuels by requiring that the mix of fuels sold reaches pre-specified targets of carbon reduction. Since oil sands yield heavier crude, more energy is required for producing and refining it, thus giving that crude a higher carbon intensity than conventional crude.

[16] H.R. 2454 is a cap-and-trade proposal that the House of Representatives has passed to reduce future levels of greenhouse gas emissions. It requires that lower targets for emissions be met by manufacturers and other producers, either by reducing emissions themselves or by purchasing emissions permits from producers that can economically reduce their emissions at lower cost. The American Power Act is the Senate’s version of H.R. 2454 that proposes a cap and trade regime on electric utilities and later (in 2016) on industrial sources, and taxes gasoline consumption.

[17] Greenwire, “Oil and Gas: Industry knocks Obama admin claims on Utah leases,” November 20, 2009, www.eenews.net/Greenwire/2009/11/20/archive/9?terms=salazar; and Land Letter, “Oil and Gas: Interior agencies showing marked shift in leasing policies”, November 19, 2009, www.eenews.net/Landletter/2009/22/19/archive/3?terms=salazar ; Greenwire, Offshore Drilling: Lift shallow-water moratorium, Landrieu tells Obama admin, May 20, 2010, http://www.eenews.net/Greenwire/2010/05/20/archive/6?terms=offshore+oil+moratorium, the Washington Post, “Obama presses for action on energy bill”, June 16, 2010, http://www.washingtonpost.com/wp-dyn/content/article/2010/06/15/AR2010061505595.html?sub=AR , and the Wall Street Journal, Crude Politics, The drilling experts speak out on the Obama deepwater moratorium, June 17, 2010, http://online.wsj.com/article/SB10001424052748704198004575311033371466938.html?mod=WSJ_Opinion_LEADTop

[18] U.S. Department of energy, Office of Fossil energy, “Undeveloped Domestic Oil Resources: The Foundation for Increasing Oil Production and a Viable Domestic Oil Industry,” February 2006, http://www.fossil.energy.gov/programs/oilgas/publications/eor_co2/Undeveloped_Oil_Document.pdf

[19] The U.S. Geological Survey recently updated its assessment of the Piceance Basin in western Colorado and found it to have oil shale resources that are 50% higher than the previous estimate of 1 trillion barrels. That resource update would increase the total U.S. shale oil resources to 2.6 trillion barrels. See http://www.usgs.gov/newsroom/article.asp?ID=2182

[20] Strategic Unconventional Fuels Integrated Program Plan, February 2007, http://www.unconventionalfuels.org/publications/reports/executiveSummary.pdf

[21] The Congressional Research Service, October 20, 2009, http://epw.senate.gov/public/index.cfm?FuseAction=Files.View&FileStore_id=01feb68b-ef57-4748-8f5c-d88c0e7d6bd5

[22] E&E Publishing, “Oil and Gas: Industry chafes over Interior’s revised oil shale leases,” October 29, 2009, www.eenews.net/Landletter/2009/10/29/archive/1?terms=oil+shale

[23] The Denver Post, “Oil shale opponents aren’t just evil—they’re just wrong,”’ November 23, 2009, http://www.denverpost.com/commented/ci_13846941?source=commented-

[24] Energy Information Administration, “Factors Affecting Gasoline Prices,” http://tonto.eia.doe.gov/energyexplained/index.cfm?page=gasoline_factors_affecting_prices

[25] Energy Information Administration, “Energy market and Economic Impacts of H.R. 2454, the American Clean Energy and Security Act of 2009,” August 4, 2009, www.eia.doe.gov/oiaf/servicerpt/hr2454/index.html

[26] Energy Information Administration, Annual Energy Outlook 2010, www.eia.doe.gov/oiaf/aeo/index.html

[27] Energy Information Administration, http://tonto.eia.doe.gov/cfapps/ipdbproject/IEDIndex3.cfm?tid=90&pid=44&aid=8

[28] Energy Information Administration, Annual Energy Outlook 2010, http://www.eia.doe.gov/oiaf/aeo/leg_reg.html

[29] Ibid.

[30] Energy Information Administration, Short-Term Energy Outlook, June 2010, www.eia.doe.gov/emeu/steo/pub/contents.html

[31] The Washington Post, China may have dug a financial hole, June 18, 2010, http://www.washingtonpost.com/wp-dyn/content/article/2010/06/17/AR2010061705794.html

[32] Ibid.

[33] “China’s Car Sales Down in October—To 80 Percent Growth”, November 7, 2009, http://www.thetruthaboutcars.com/china%E2%80%99s-car-sales-down-in-october-%E2%80%93-to-80-percent-growth/

[34] Reuters, China oil demand rise second fastest, inventories drag, March 22, 2010, http://in.reuters.com/article/oilRpt/idINTOE62L01Z20100322?sp=true

[35] Energy Information Administration, International Energy Outlook 2009, http://www.eia.doe.gov/oiaf/ieo/index.html

[36] “Worldwide Look at Reserves and Production,” Oil and Gas Journal, Vol. 106, No. 48 (December 22, 2008), pp. 23-24.

[37] For example, Venezuela signed a deal with China under which the latter would invest $16 billion over three years. The deal could raise oil output by several hundred thousand barrels a day. http://www.eenews.net/Greenwire/2009/09/18/. China National Petroleum Corp. received a $30 billion low-interest loan from a state-run bank to finance overseas acquisitions, Beijing’s latest bid to secure mineral resources to fuel the country’s burgeoning economy. http://www.eenews.net/Greenwire/2009/09/09/. CNOOC and Sinopec have agreed to buy a 20 percent stake in an oil field off the coast of Angola for $1.3 billion, the latest in a series of Chinese acquisitions of overseas energy and mining assets. http://www.eenews.net/Greenwire/2009/07/20/

[38] Politico, To compete with China, U.S. must tap natural gas, April 13, 2010, http://www.politico.com/news/stories/0410/35689.html#ixzz0kyYru8gb

[39] Reuters, China bags oil sands stake, not finished yet, April 13, 2010, http://www.reuters.com/article/idUSTRE63C17X20100413 and www.conocophillips.com

[40]David Pierson, “China’s push for oil in the Gulf of Mexico puts U.S. in awkward spot,” Los Angeles Times, http://www.latimes.com/business/la-fi-china-oil22-2009oct22,0,2776603.story?track=rss.

[41] Reuters, China oil demand rise second fastest, inventories drag, March 22, 2010, http://in.reuters.com/article/oilRpt/idINTOE62L01Z20100322?sp=true

[42] Reuters, Oil falls as demand, inventories weigh, April 12, 2010, http://www.reuters.com/article/idUSTRE6142V820100412

[43] Energy Information Administration, Country Analysis Brief on China, www.eia.doe.gov/emeu/cabs/China/Background.html

[44] Energy Information Administration, International Energy Outlook 2010, Table A7, http://www.eia.doe.gov/oiaf/ieo/pdf/ieorefcase.pdf

[45]Energy Information Administration, International Energy Outlook 2010, Appendix H, http://www.eia.doe.gov/oiaf/ieo/pdf/ieoecg.pdf

[46] Energy Information Administration, Annual Energy Review 2008, Table 11.19, http://www.eia.doe.gov/emeu/aer/pdf/pages/sec11_39.pdf, and International Energy Outlook 2010

[47] Energy Information Administration, U.S. Carbon Dioxide Emissions in 2009: A Retrospective Review, May 5, 2010, http://www.eia.doe.gov/oiaf/environment/emissions/carbon/index.html

[48] Institute for Energy Research, Lost in Translation, https://www.instituteforenergyresearch.org/2009/07/28/lost-in-translation/.

[49]http://online.wsj.com/article/SB125409730711245037.html

[50] Robert L. Bradley, Jr. and Richard W. Fulmer, Energy: The Master Resource (Kendall/Hunt Publishing Company, 2004), page 49.