According to BP’s energy outlook, fossil fuels will continue to provide most of the world’s energy, supplying 81 percent of global supply in 2035. Renewable energy, excluding hydroelectric power, is expected to almost triple its share by 2035, but still only represent just 8 percent of global supply. In the BP forecast, about one-third of the increase in global demand by 2035 is supplied by natural gas, another one-third by oil and coal together, and another third by non-fossil fuels. Carbon dioxide emissions from energy consumption are expected to increase by 25 percent between 2013 and 2035, but their growth slows in the latter decade of the forecast.[i]

Source: BP, http://www.bp.com/content/dam/bp/pdf/Energy-economics/energy-outlook-2015/Energy_Outlook_2035_booklet.pdf

Demand for Energy

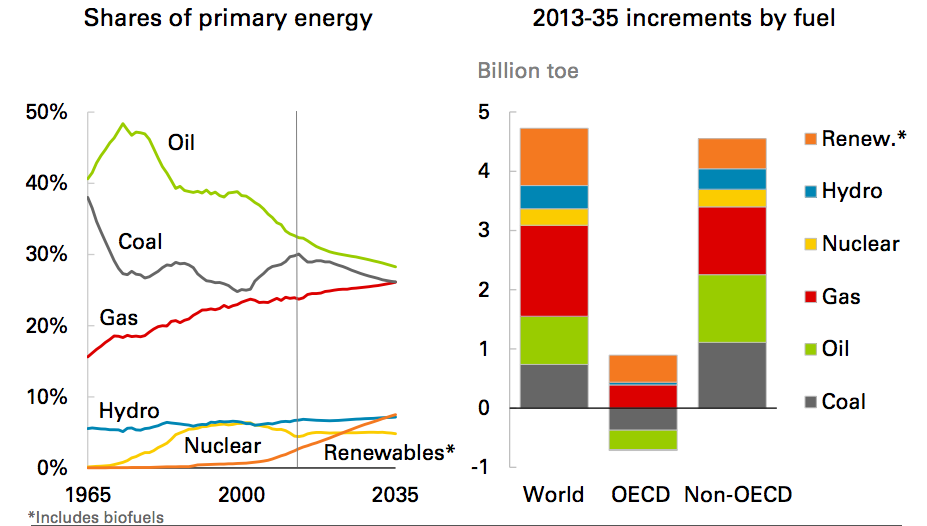

According to BP, primary energy consumption is expected to increase by 37 percent between 2013 and 2035, with annual growth averaging 1.4 percent. Almost all of the projected growth (96 percent) is from the developing countries with energy consumption growing at 2.2 percent per year. Developing Asia, where energy growth had averaged 7 percent per year since 2000, is projected to slow to 2.5 percent between 2013 and 2035, ending the rapid growth there, which was driven by industrialization and electrification. The slowing of energy demand is due to slower economic growth and a reduction in energy intensity (energy consumption per unit of GDP).

In the developing countries, energy demand growth is fairly evenly spread among the major fuel categories in BP’s forecast—a quarter each for oil, natural gas, coal, and non-fossil fuels. In the developed countries, reductions in the demand for oil and coal are countered by increases in natural gas and renewables, in roughly equal parts.

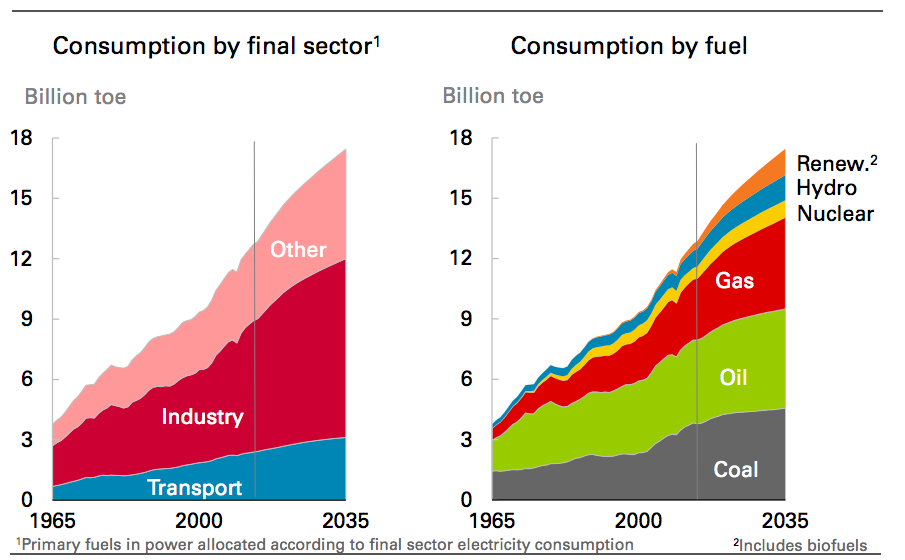

The industrial sector is expected to grow at 1.4 percent per year during the forecast period, about half its growth rate since 2000. The transportation sector is expected to grow at 1.2 percent per year, accounting for 15 percent of the growth in demand between 2013 and 2035. The ‘other’ sector (residential, services and agriculture) is projected to be the fastest growing sector, averaging 1.6 percent per year between 2013 and 2035.

Source: BP, http://www.bp.com/content/dam/bp/pdf/Energy-economics/energy-outlook-2015/Energy_Outlook_2035_booklet.pdf

Globally, coal was the fastest growing fossil fuel since 2000, but between 2013 and 2035, but BP expects it to be the slowest growing fuel, growing at 0.8 percent per year due to the slowing of coal-based industrialization in Asia, the impact of environmental regulations in many countries, and low natural gas prices in major markets. Natural gas becomes the fastest growing fossil fuel, growing at 1.9 percent per year. Similar to coal, oil grows at just 0.8 percent per year, just marginally ahead of coal. The fastest growth in percentage terms is in non-hydroelectric renewable energy, growing at 6.3 percent per year. Nuclear power grows at 1.8 percent per year, and hydroelectric power at 1.7 percent per year.

Electric Power Sector

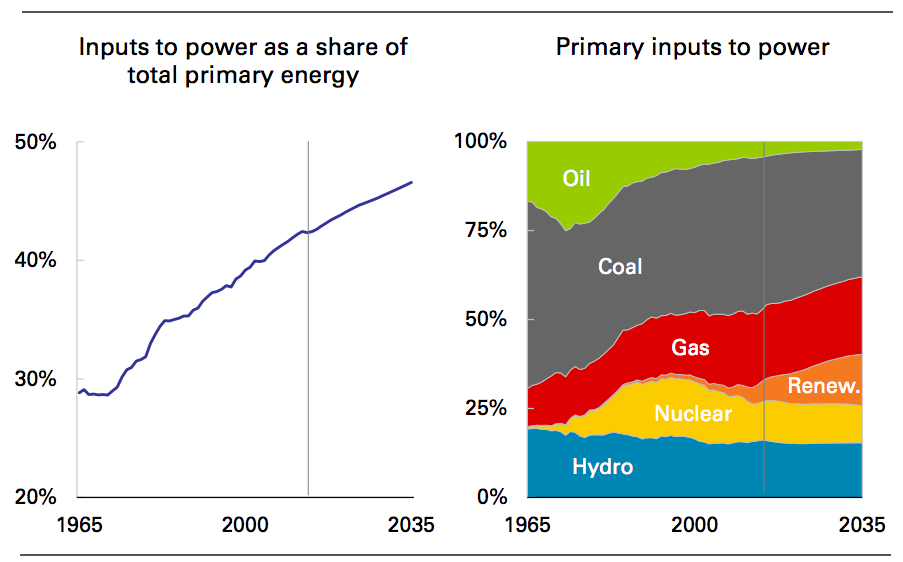

BP expects the world to continue its trend toward electrification with primary energy consumption from power generation increasing from a 42 percent share today to a 47 percent share in 2035. Fuel shares in the global power generating sector have historically shifted over time with oil gaining in the 1960s and losing share in the 1970s, nuclear power increasing share in the 1970s and 1980s and then falling after 2000, and natural gas’ share increasing through the 1990s and 2000s. In BP’s outlook, the largest future shifts are an increase in the renewable inputs in electric power generation and a decline in the share of coal inputs to power generation. However, coal still remains the dominant fuel input for power generation with over a third share, but down from a 44 percent share today.

Source: BP, http://www.bp.com/content/dam/bp/pdf/Energy-economics/energy-outlook-2015/Energy_Outlook_2035_booklet.pdf

Technological Development and Productivity

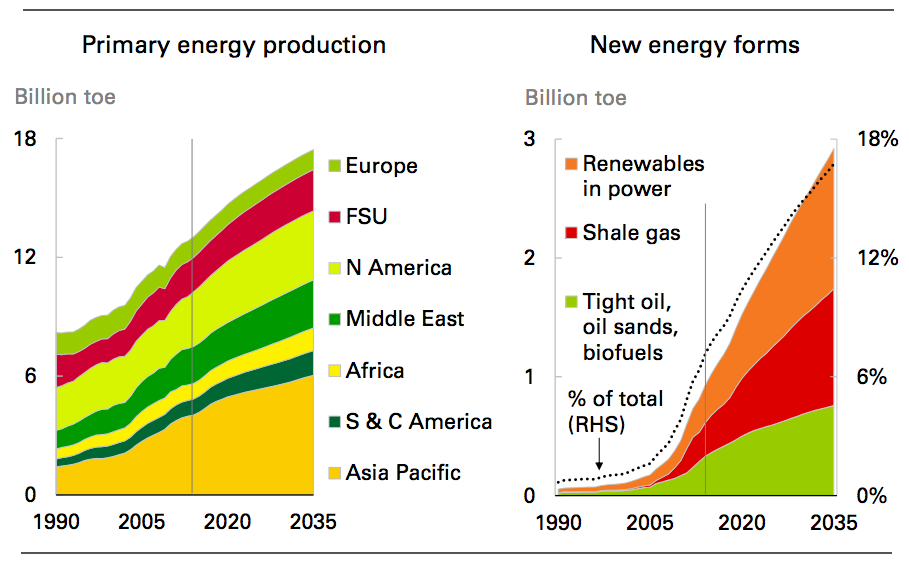

The BP Outlook assumes continued growth in new forms of energy, which have been enabled by technological development and large investments. Improved technology and productivity are expected to make a significant contribution to supply growth in the BP forecast. New sources of energy—renewable energy, shale gas, tight oil, oil sands, among others—together increase at a rate of 6 percent per year and contribute 45 percent towards incremental energy production in 2035.

Source: BP, http://www.bp.com/content/dam/bp/pdf/Energy-economics/energy-outlook-2015/Energy_Outlook_2035_booklet.pdf

Oil Sector

According to BP, “technological innovation and high oil prices have unlocked vast unconventional resources in North America, significantly increasing U.S. oil and gas production and altering global energy balances.” Despite production increases outside of North America, BP does not expect other parts of the world to replicate the dramatic growth in unconventional oil and gas production seen in North America.

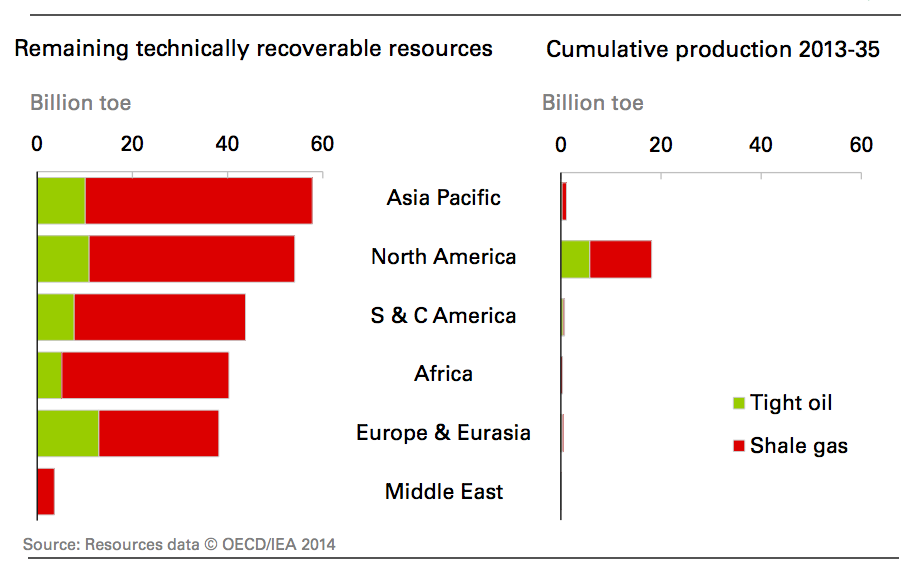

According to BP, global technically recoverable resources are estimated to be about 340 billion barrels for tight oil (shale oil) and 7500 trillion cubic feet for shale gas. The largest resources are found in Asia, followed by North America. BP expects cumulative North American production of tight oil between 2013 and 2035 to be 50 percent of total tight oil technically recoverable resources and cumulative North American production of shale gas to be about 30 percent of total shale gas technically recoverable resources. The comparable numbers for the rest of the world are expected to be 3 percent and 1 percent, respectively.

Source: BP, http://www.bp.com/content/dam/bp/pdf/Energy-economics/energy-outlook-2015/Energy_Outlook_2035_booklet.pdf

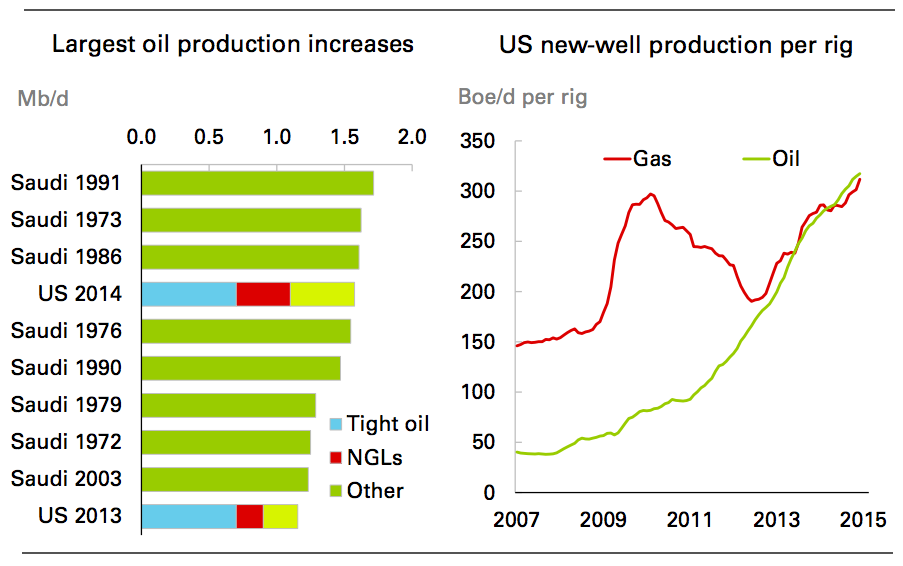

In 2014, U.S. oil production grew at roughly 1.5 million barrels per day and was the largest in U.S. history, driven by increased production of tight oil and natural gas liquids. The recent increases in U.S. oil production have been among the largest in the world, with only Saudi Arabia recording larger annual production growth. Productivity, measured by new well production per rig, increased by 34 percent per year for oil and 10 percent per year for gas in the United States between 2007 and 2014.

U.S. shale gas production is expected to grow rapidly in the BP Outlook at 4.5 percent per year, although growth rates moderate slowly. Growth in U.S. tight oil, however, is expected to flatten in the forecast, due to high well decline rates and less extensive resources than for shale gas.

BP expects the Organization of Petroleum Exporting Countries (OPEC) to regain oil market dominance and exceed their historic record production levels by 2030 as U.S. tight oil growth flattens out in the forecast. But, in the near term, demand for oil from OPEC is expected to remain under pressure as U.S. tight oil production remains strong. U.S. production of tight oil has been the main driver in supply growth that prompted the large drop in oil prices since June 2014.

Source: BP, http://www.bp.com/content/dam/bp/pdf/Energy-economics/energy-outlook-2015/Energy_Outlook_2035_booklet.pdf

U.S. tight oil production is expected to increase by about 3 million barrels per day between 2013 and 2035. However, slower U.S. tight oil production coupled with higher global demand is expected to increase the demand for OPEC oil, which BP expects to exceed its historic 2007 high of 32 million barrels per day by 2030. OPEC’s market share by 2035 is expected to reach 40 percent, similar to its average over the past 20 years. Global oil and liquids supplies are expected to increase by 20 million barrels per day by 2035, with North American production expected to lead global supply growth until 2020, increasing by 9 million barrels per day by 2035. Oil production in the Middle East is expected to increase after 2020 by 5 million barrels per day by 2035.[ii]

BP expects the global demand for oil and other liquids such as biodiesel to increase by about 19 million barrels per day, reaching 111 million barrels per day in 2035. China is expected to replace the United States as the world’s top oil consumer by 2035. BP expects the United States to become self-sufficient by the 2030s due to its increased oil production and lower demand for energy.

[i] BP, Energy Outlook 2035, February 2015, http://www.bp.com/en/global/corporate/about-bp/energy-economics/energy-outlook.html

[ii] Reuters, BP’s 2035 outlook sees OPEC oil gaining ground as U.S. shale slows, February 17, 2035, http://www.reuters.com/article/2015/02/17/oil-bp-idUSL5N0VR3J720150217