President Biden’s goal is a net-zero economy by 2050. According to an International Energy Agency (IEA) report, to reach net-zero emissions by 2050, governments should refuse to approve any new oil and gas fields, as well as any new unabated coal power plants by the end of 2021, and new sales of fossil fuel boilers should be phased out by the end of 2025. It seems like Biden is intent on complying, based on his executive orders. Yet, the world’s coal producers are planning 432 new mine projects with 2.28 billion metric tons of annual output capacity—a 30 percent expansion of capacity by 2030. China, Australia, India, and Russia account for more than three-quarters of the new projects.

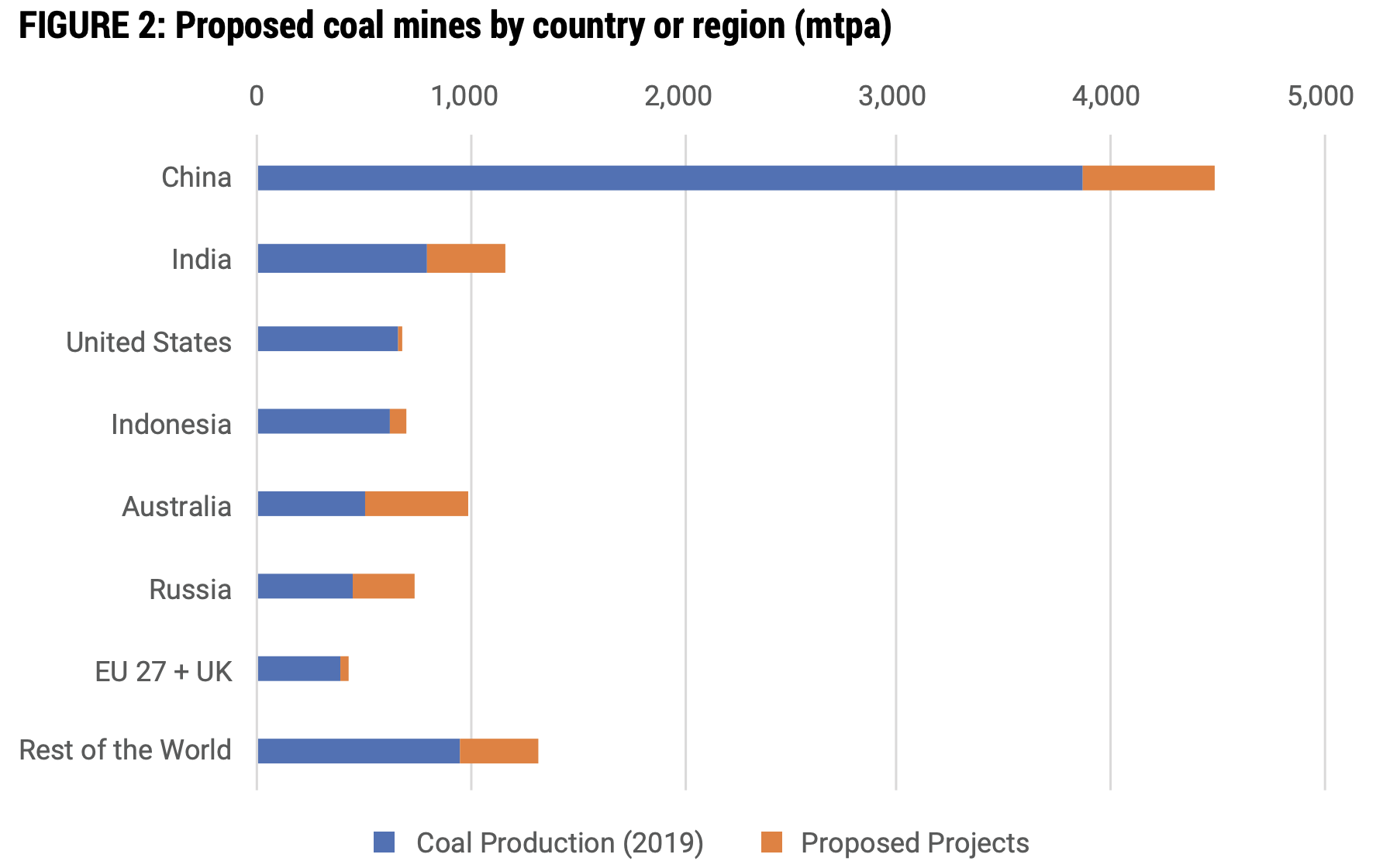

China is building 452 million metric tons of new annual production capacity and has another 157 million metric tons in planning for a total of 609 million metric tons. That means China’s planned new mine capacity will be 26 percent higher than all the coal that the United States produced in 2020. China already produces almost 50 percent of the world’s coal and 53 percent of the world’s coal-fired electricity—nine percentage points more than five years earlier. According to the report by Global Energy Monitor, four Chinese provinces and regions—Inner Mongolia, Xinjiang, Shaanxi and Shanxi—account for nearly a quarter of all the proposed new coal mine capacity in the country.

Despite global coal-fired generation being on the decline since 2019, thermal coal operations still dominate the new proposed mines, making up 71 percent of the proposed new mine capacity. In North America, however, the numbers are reversed, with metallurgical coal used for steel-making accounting for 70 percent of the small increase in proposed new mine capacity.

The emissions from coal mine projects now on the drawing board are estimated to total between 5,000 and 5,800 million metric tons of carbon dioxide equivalent each year from combustion and methane leakage, which is comparable to the annual carbon dioxide emissions of the United States prior to the coronavirus pandemic—5,140 million metric tons in 2019.

New Coal Mine Capacity

The majority of the proposed coal mines in China and India are sponsored by state-owned enterprises. That is, public money continues to subsidize mine projects to fuel province and state economies. India has 13 million metric tons under construction and 363 million metric tons in planning stages. Australia has 31 million metric tons under construction and 435 million metric tons in planning and Russia has 59 million metric tons under construction and 240 million metric tons in planning. Unlike China, where 74 percent of projects are already under construction, the vast majority of proposed mining capacity in Australia (94 percent), India (96 percent), and Russia (80 percent) are in pre-construction phases and have yet to undergo the build-out of mine infrastructure.

While much of Western Europe is phasing out coal, Poland (32 million metric tons) and Turkey (22 million metric tons) continue to build new operations, accounting for 60 percent of Europe’s new mine development. Most new capacity remains under development in coal communities, such as Łódź and Lower Silesia in Poland, and Turkey’s Black Sea province of Bartin. As of 2020, 12 percent of the 453 million metric tons per annum proposed capacity in these regions is under construction, with the remaining 88 percent of capacity in pre-construction phases and subject to financial constraints or institutional and government restrictions in the future.

Mine development is also occurring in South Africa, Indonesia, and Mozambique. South Africa accounts for 65 percent of the proposed capacity in Africa and the Middle East. If all proposed mines went into operation, it would undergo a 51 percent increase in current coal production. Indonesia, the major driver of capacity growth in Southeast Asia, would undergo a 12 percent increase in production.

Stranded Asset Risk

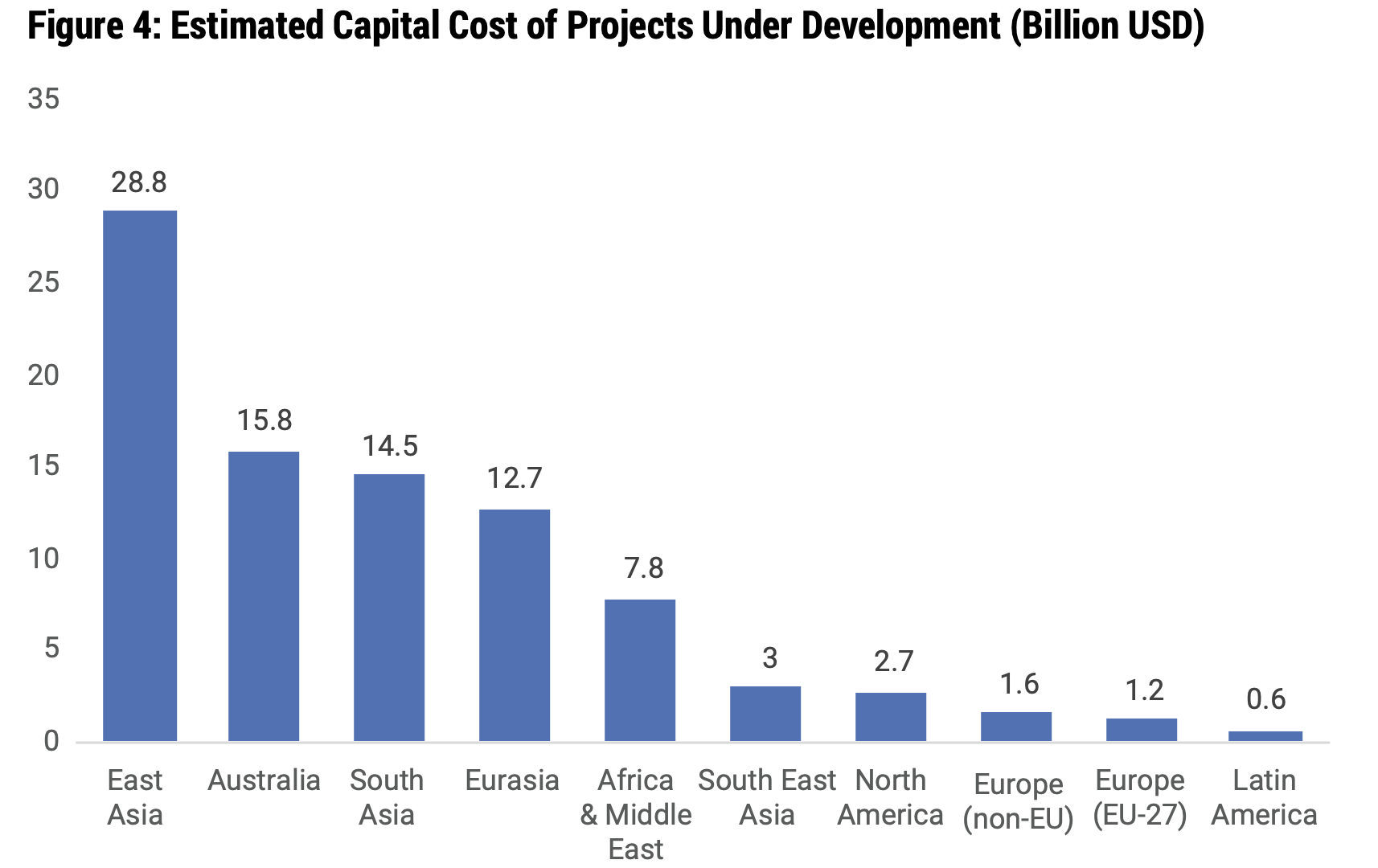

Coal mines and related infrastructure such as ports and railways are capital-intensive projects that cost tens of millions of dollars. The capital expenditures necessary to bring all 432 mine projects into operation is $91 billion, based on the average capital costs to open a coal mine. If planned coal mines open as intended, but are forced to lower production levels or shut down early, they represent a significant stranded asset risk, which the governments who in many cases own them are unlikely to willingly absorb.

Conclusion

Here in the United States—with the world’s largest coal reserves by far—policymakers, utilities and the media are pronouncing coal’s demise. Meanwhile, around the world, new coal mine development is taking place led by China, who already produces almost 50 percent of the world’s coal. While China’s government states that they will eventually take actions to reduce greenhouse gas emissions and be carbon neutral by 2060, the country’s current actions are vastly different from opening new coal mines to building new coal generating capacity at home and abroad that can operate for 40, 50 or even 60 years. Not only is China developing new coal mines, so are Australia, India, Russia, Poland, Turkey, South Africa, Indonesia, and Mozambique. The United States, under Biden, will be taking actions to reduce greenhouse gas emissions that will be costly while most of the rest of the world will develop energy industries that are less expensive and more reliable.