Goldman Sachs expects gasoline prices to reach $4.35 a gallon by the end of the year—8.5 percent higher than the current national average of $4.01 a gallon—and average $4.40 a gallon in 2023, peaking at around $4.53 a gallon in the second quarter of next year. The increase is due to continued supply shortages and sustained high demand. Goldman’s analysts expect U.S. gasoline demand to increase again after showing signs of slowing over the past month. According to the Energy Information Administration, fuel demand dropped off dramatically, hitting levels not seen since the pandemic in July 2020. Goldman’s analysts also expect more congestion at oil refineries from the coming fall maintenance season and from possible hurricanes that would limit supply.

According to the investment bank, balancing supply and demand would require more “demand destruction on top of the ongoing economic slowdown.” Apparently, the divergence between benchmark Brent prices, which averaged $110 a barrel in June and July, and the corresponding Brent-equivalent global retail fuel price of $160 per barrel was not enough to trigger enough demand destruction to end the supply deficit. The discount of Brent prices is due to the worsening energy crisis created by Russia’s invasion of the Ukraine, as the costs of transforming oil out of the ground (Brent) into global retail pump prices increase due to surging E.U. gas prices, freight rates, and global refining utilization.

Goldman Sachs forecasts U.S. retail diesel prices to rebound to $5.50 per gallon by the fourth quarter—7.9 percent higher than the current national average of $5.098 per gallon—and average $5.25 per gallon in 2023. The Goldman Sachs forecast indicates that U.S. retail fuel prices will rally into year-end then eventually decline from second quarter 2023 as refining and marketing margins start to normalize.

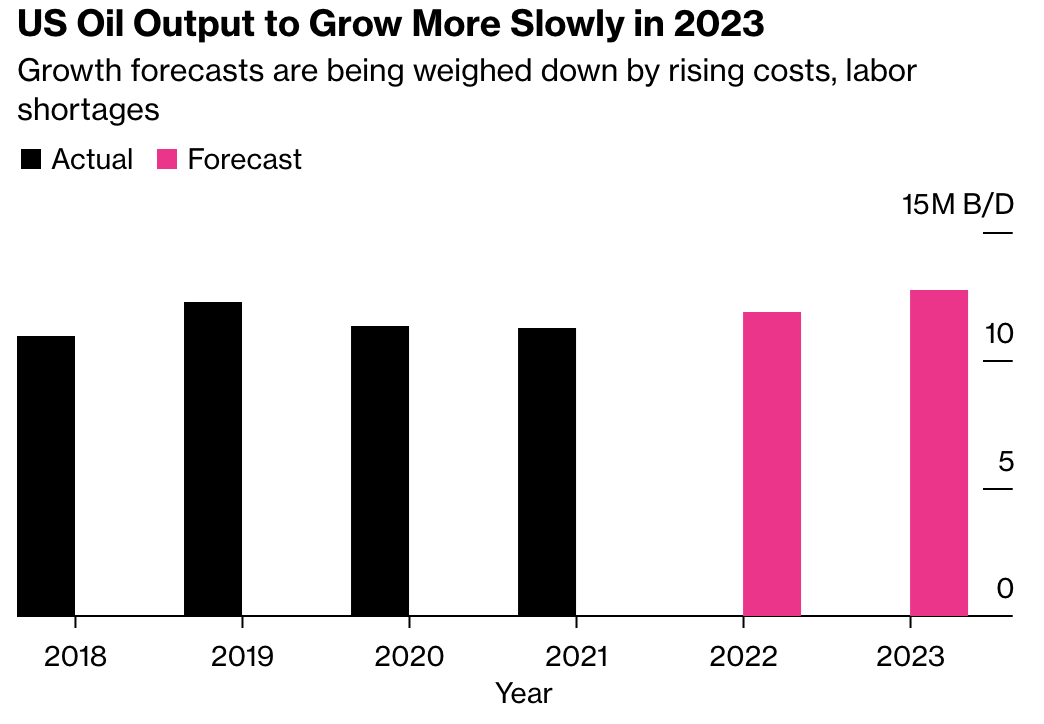

According to the Energy Information Administration, U.S. oil production is expected to reach a new record in 2023 of 12.7 million barrels per day with output growing more slowly than previously anticipated due to surging costs and labor shortages in America’s shale oil fields. Output is expected to expand at an average rate of 840,000 barrels a day next year, down from a prior forecast of 860,000 barrels a day. The current annual record is 12.3 million barrels per day set in 2019. EIA also lowered this year’s oil production forecast, estimating U.S. output will average 11.86 million barrels a day in 2022.

Those production increases are against a forecast of global petroleum consumption growing by 2.1 million barrels per day each this year and next year, reaching 101.5 million barrels per day in 2023. The United States was previously a key swing producer, usually capable of ramping up supply quickly as global demand shifts. But, since President Biden took office, shale oil drillers have limited growth in favor of increasing shareholder returns in the face of soaring oilfield costs and anti-oil and gas policies of the Biden Administration. Further, the Inflation Reduction Act will not help given the increased costs and taxes it puts on U.S. oil producers, which have not been taken into account in EIA’s forecast.

{kind=link}

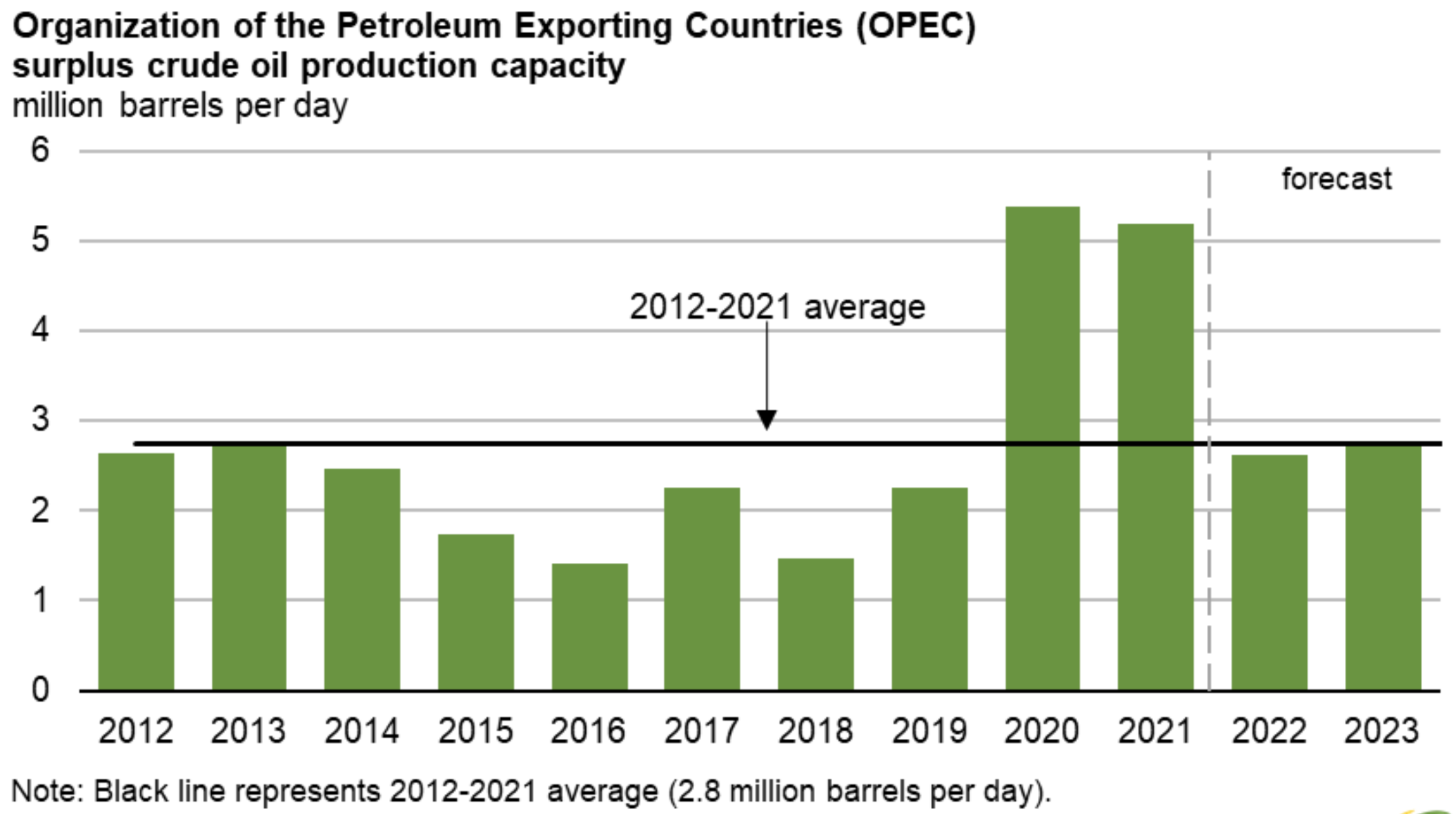

EIA’s forecast for OPEC spare capacity in 2022 is below the 2012 to 2021 average of 2.8 million barrels per day and is at that average for 2023, which shows that President Biden’s begging the bloc for more oil production is a relatively fruitless ambition. Its spare capacity in 2020 and 2021, during most of the period of COVID lockdowns was almost double the current amount. (See graph below.)

{kind=link}

EIA sees U.S. refineries averaging 93 percent utilization in the third quarter 2022, as a result of high wholesale product margins with refining margins for gasoline and diesel that are at or near record highs amid low inventory levels. During COVID lockdowns, the United States lost about a million barrels a day of refining capacity to closure as well as refineries converting to biofuels to capture lucrative state and federal subsidies, which are being extended in the Manchin/Schumer Inflation Reduction Act.

EIA’s forecast of the level in the Strategic Petroleum Reserve (SPR) is 365.5 million barrels by the fourth quarter 2022—about half of its capacity as President Biden continues to sell the oil in his hopes to get gasoline prices down by putting more oil on the market. The SPR release of 1 million barrels per day will end in about 80 days and contribute to the tight market that Goldman Sachs sees increasing gasoline and diesel prices at year end. In 2023, EIA estimates the SPR level at an even lower level—340.8 million barrels, despite Biden indicating that he will be buying oil to refill the reserve. Some have expressed concern that the United States is selling off its most valuable type of oil…medium sour crude…leaving it with product unsuited for most American refiners.

Conclusion

Goldman Sachs is forecasting higher gasoline and diesel prices by the end of this year as supply will continue to be short of continuing sustained demand. The investment bank does not see enough demand destruction to balance supply and demand creating higher prices. EIA has reduced its increase in the oil production forecast, now expecting the increase in U.S. oil production to be 840,000 barrels per day in 2023, making a record U.S. production level of 12.7 million barrels per day for the year. But that increase is only 40 percent of the increase in global demand of 2.1 million barrels per day. During the shale oil renaissance, the United States was producing 80 percent of increased global production. The Biden Administration’s anti-oil and gas policies as well as increased costs and a labor shortage are the major reasons for the lower level of production increase.