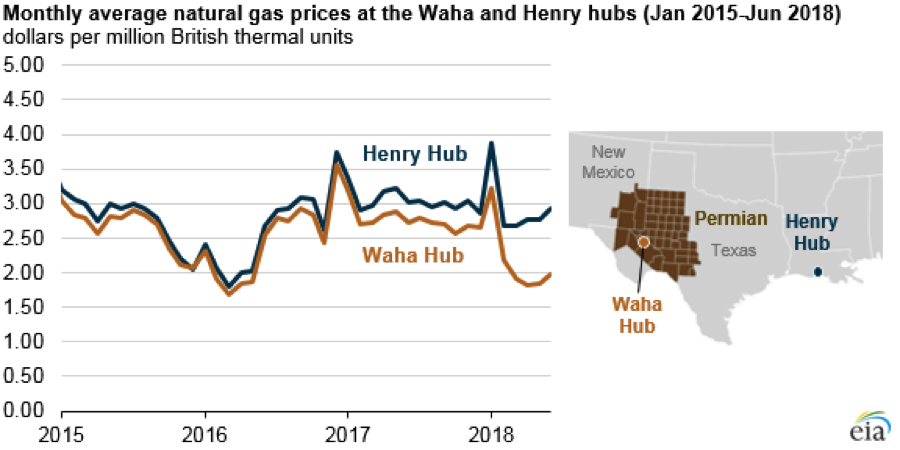

A lack of pipeline capacity is hampering Permian Basin crude oil and natural gas production. Pipelines that were adequate a few years ago are now overwhelmed due to the tremendous growth in production. New pipeline projects are being considered to alleviate the bottlenecks, which are causing some of the region’s oil and gas to trade at steep discounts compared to benchmark prices. Producers selling oil in Midland, Texas, are receiving about $16 a barrel less than what sellers are getting in Oklahoma for crude oil, and the natural gas price differential between Waha Hub in Western Texas and Henry Hub in Louisiana is about $1 per million Btu.

Oil in the Permian Basin

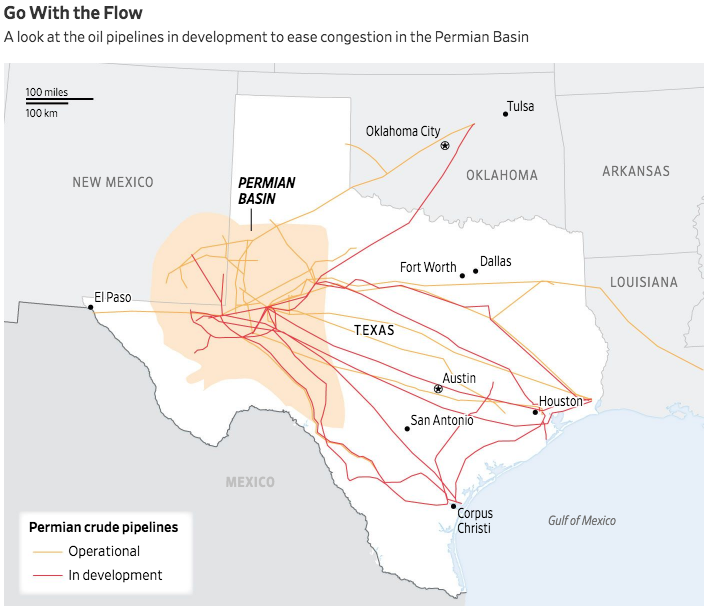

Oil drillers in the Permian Basin produced 3.3 million barrels of oil per day in June 2018—0.9 million barrels per day higher than in June 2017. That makes the oil field one of the world’s leading producers—producing more, for example, than the average daily crude output of the United Arab Emirates last year. Almost all the crude pipelines leaving the Permian Basin were operating at full capacity last quarter—up from an average of 94-percent capacity during the previous quarter. The congestion is expected to become worse over the next year and a half before new pipelines will begin to alleviate the bottlenecks that are depressing local crude prices.

Pipeline builders are planning new oil and gas projects in Texas, where there is increased demand from customers willing to pledge to contracts. Epic Midstream Holdings, Plains All American Pipeline LP, and Phillips 66 in a partnership with refiner Andeavor are building new oil pipelines aimed at Corpus Christi that are expected to add about 1.8 million barrels of combined capacity late next year. Epic Midstream Holdings LP had been planning to build a pipeline with a capacity of 440,000 barrels a day from West Texas to Corpus Christi on the Gulf Coast, but is now considering enlarging it to 675,000 barrels a day. Enterprise Products Partners LP is considering converting a gas liquids pipeline to oil.

Magellan Midstream Partners LP locked in longer-term customers at premium rates because it is expected that the oil price differential will remain high until new pipelines are built.

Some believe the new pipelines could face delays and increased costs that could be exasperated by the 25-percent tariffs on steel imports. Plains All American indicated the tariff would increase the cost of its $1.1 billion pipeline project by about $40 million, but despite the cost, the company plans to move ahead with the project. Phillips 66, however, indicated that the tariff would have “minimal” impact on the company’s planned West Texas pipeline because most of the pipe is American-made.

Morgan Stanley projected slowdowns of three to six months for some of the new pipeline projects because of concerns regarding right-of-way acquisition and the complexity of the proposed lines. The lack of pipelines is expected to limit annual oil production growth in the Permian to 360,000 barrels a day, down from a once expected 650,000 barrels per day. Since Midland producers receive about $16 per barrel less for their oil due to pipeline shortages, these delays equate to about $4.64 million per day for those investing in production in the Permian. The number of drilled but uncompleted wells continues to rise in the Permian. It was over 3,300 wells in June.

While there is about 300,000 barrels per day of train capacity, most of that capacity is being used to carry sand that is needed for the hydraulic fracturing process. While trucks could move some, it is a very expensive option—at least $12 per barrel and could be as high as $15 to $18 per barrel. (Shipping oil by pipeline only adds $2 to $4 per barrel.) Only about 10,000 barrels per day is being moved by truck and that figure could be capped at 40,000 barrels per day because of constraints on trucking. There is also a labor shortage in the Permian Basin making trucking oil a less viable option.

Natural Gas in the Permian Basin

According to the Energy Information Administration (EIA), natural gas production in the Permian Basin averaged 10.4 billion cubic feet per day in June 2018—2.1 billion cubic feet per day greater than in June 2017. Much of the increased production is associated natural gas—natural gas produced as a byproduct of oil production. The widening price differential between Waha and Henry Hub indicates pipeline capacity is constrained. If natural gas production continues to grow, and natural gas prices continue to fall, some producers may be forced to discontinue oil production to avoid producing associated natural gas.

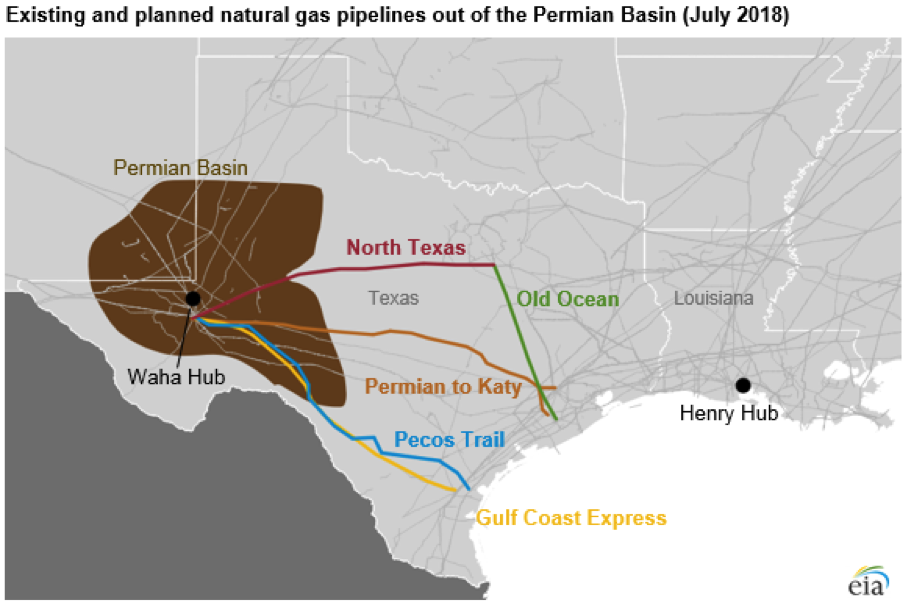

Two pipelines—Comanche Trail and Trans-Pecos—were completed in 2017 to export Permian natural gas to Mexico. Although these pipelines have a combined capacity of 2.6 billion cubic feet per day, they are not expected to see significant flows until late 2018 or early 2019 due to insufficient pipeline infrastructure in Mexico. The expansion of the North Texas Pipeline and resumption of service on the Old Ocean Pipeline are also expected to become available this year and together will increase gas pipeline capacity by 0.15 billion cubic feet per day.

Several new pipelines are currently under consideration: the Gulf Coast Express Pipeline (2.0 billion cubic feet per day), the Permian to Katy Pipeline (1.7 to 2.3 billion cubic feet per day), and the Pecos Trail Pipeline (1.9 billion cubic feet per day). Of these three projects, only the Gulf Coast Express is under construction, with an expected in-service date of October 2019. The proposed pipelines from the Permian Basin are to meet Gulf Coast demand for natural gas, including liquefied natural gas to be exported and regional industrial gas use.

Resources in the Permian Basin

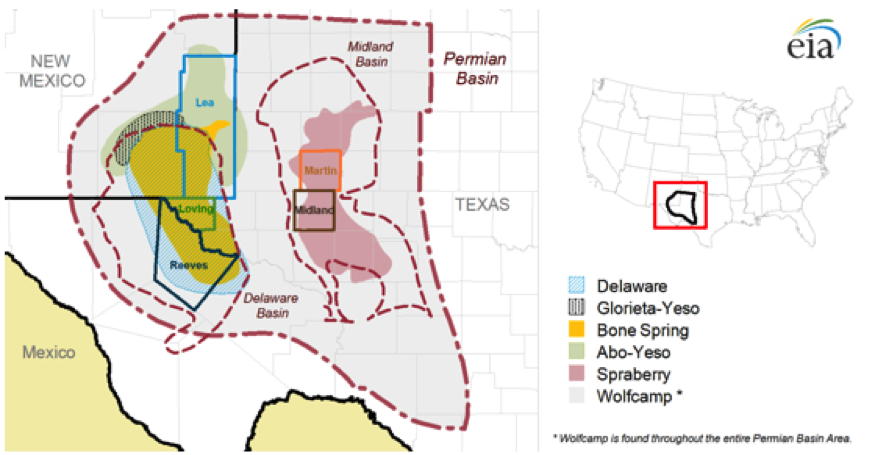

In November 2016, the U.S. Geological Survey (USGS) estimated that technically recoverable tight oil and shale gas resources in the Midland Basin portion of Texas’s Permian Basin (specifically the Wolfcamp shale formation) could exceed 20 billion barrels of oil, 16 trillion cubic feet of natural gas, and 1.6 billion barrels of hydrocarbon gas liquids.

Conclusion

The Permian Basin is making Texas one of the largest oil producers in the world with its large endowment of resources and the ability to reach them through hydraulic fracturing and directional drilling. However, a lack of pipeline capacity for both oil and natural gas shipments has resulted in drilled but uncompleted wells and their number is rising. It is expected that over the next year and a half there will be insufficient pipeline capacity, resulting in significant price differentials for Permian Basin oil and natural gas compared to that of other Hubs. Pipelines are under development but delays could occur due to rights-of-way issues and the complexity of some of the proposed pipelines.

It is important to note that some groups who oppose additional production of oil and gas because they link such production to global warming are challenging pipelines throughout the United States because they see the direct economic consequences of tightening pipeline capacity. By making production of oil and gas more expensive and less economical, they understand that this is a way to reduce investment in U.S. energy production.

A previous article on this issue is located here.