The Energy Information Administration recently released its reserves report, noting that proven reserves of natural gas increased 36 percent to 464.3 trillion cubic feet—a record that surpasses the previous high set in 2014. Natural gas production in 2017 increased by almost 3 percent from 2016 production levels—another record high. Most of this natural gas is coming from the Marcellus and Utica shale plays in Pennsylvania and neighboring states. Over a decade ago, companies began combining horizontal drilling techniques with hydraulic fracturing to unlock natural gas from shale rock.

The Permian Basin, however, is also a major player in natural gas production, as the Department of the Interior recently found the Wolfcamp Shale and overlying Bone Spring Formation in the Delaware Basin of Texas and New Mexico’s Permian Basin to contain 281 trillion cubic feet of natural gas, or about 48 billion barrels of oil equivalency. However, that production is hampered by pipeline constraints to get the gas to demand centers. Benchmark gas prices in Permian gas markets recently averaged only $0.625 per million Btu because new pipeline capacity is at least 10 months away.

Further, at least 10 new offshore platforms in the Gulf of Mexico are expected to begin producing natural gas by the end of 2018 and another eight are expected to begin production in 2019.

Last year, the United States became a net exporter of natural gas and U.S. liquefied natural gas (LNG) exports are increasing as export terminals are coming on line. U.S. LNG exports are poised for a big year in 2019.

New Offshore Fields

Offshore natural gas production in the Gulf of Mexico has been declining since fiscal year 2009. With the growth in exploration and production activities in U.S. shale basins, onshore drilling for natural gas became more economic than offshore drilling. As a result, the number of natural gas wells in the Gulf of Mexico fell from 3,271 in 2001 to 875 in 2017.

The new offshore field starts are expected to slow or reverse the declining trend. The 18 new projects are believed to hold 836 billion cubic feet of natural gas reserves, with the energy equivalency of around 144 billion barrels of oil. Most of the natural gas produced in the Gulf of Mexico is associated-dissolved natural gas produced from oil fields.

The largest of the new offshore natural gas fields is Cesar/Tonga Phase II in the Green Canyon area—about 186 miles south of New Orleans. The project is believed to contain 158 billion cubic feet of natural gas. Recently, Chevron announced that it had started production on its Big Foot deep-water project, located about 225 miles south of New Orleans. It is expected to produce up to 25 million cubic feet of natural gas per day.

U.S. LNG Industry

U.S. LNG exports almost quadrupled from 2016 to 2017 to 1.94 billion cubic feet a day, according to the U.S. Energy Information Administration. The U.S. is expected to become the world’s second-largest exporter by 2022 as new LNG projects start operating.

By the end of next year, the United Sates is expected to increase its LNG export capacity to around 10 billion cubic feet per day. And, some believe the United States could become the world’s largest exporter before 2025. Further, there are an additional 13 pending projects that regulators could approve by the end of 2019.

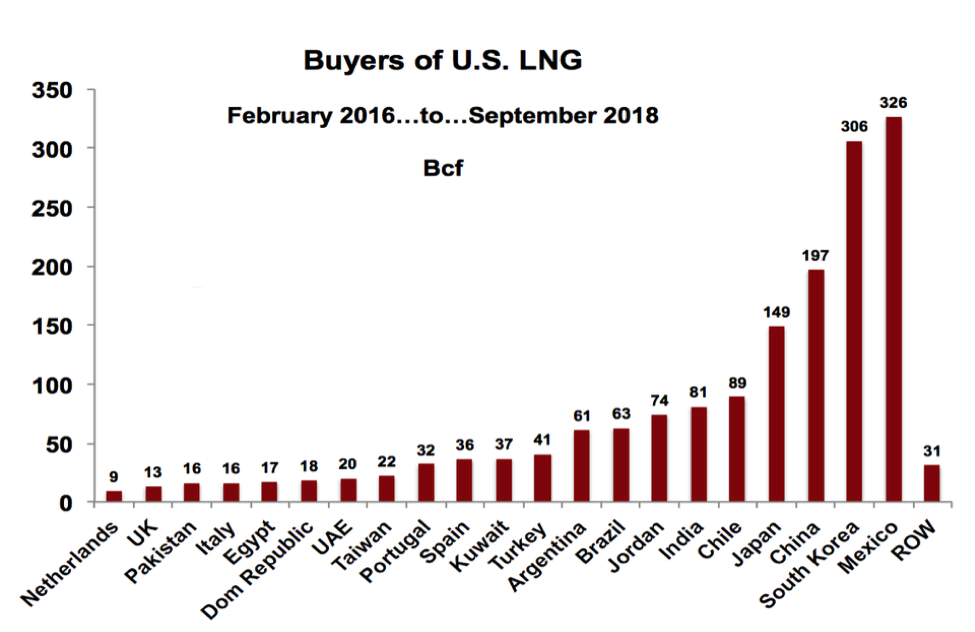

Mexico is currently the largest importer of U.S. LNG. Mexico received 20 percent of U.S. LNG exports; South Korea was second at 19 percent. Mexico, however, would like to produce more of its own natural gas and build more pipelines to gain greater access to cheaper U.S. piped gas. For example, U.S. piped gas to Mexico averaged $3.18 per million Btu so far this year, compared to $4.59 for U.S. LNG to Mexico.

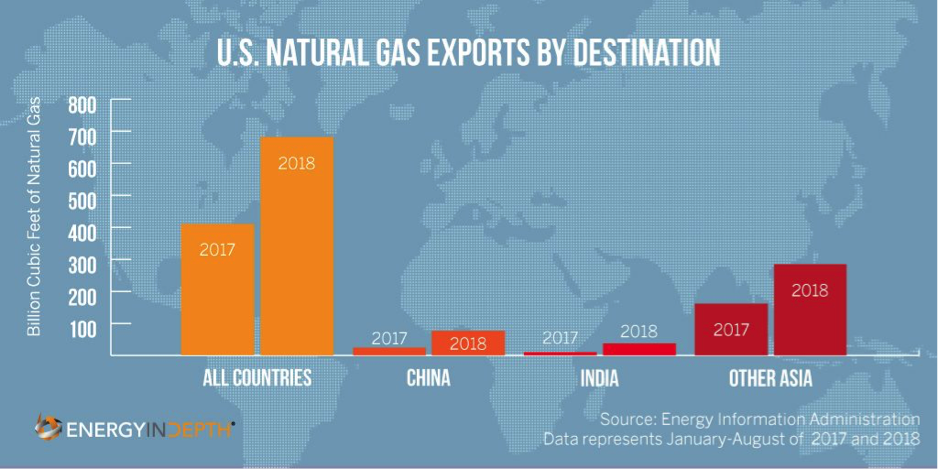

Other countries are also interested in U.S. LNG, including in Asia where China, India, and others are buyers. In 2017, the U.S. exported 15 percent of its LNG to China, which ranked third in acquiring U.S. LNG that year. Asia’s interest is noted below, depicting its growth in 2018. The United States exported approximately 681 billion cubic feet of natural gas from January to August 2018. About 58 percent of those exports went to India, China, and other Asian markets—more than double the gas sent to Asia for the same period of time in 2017.

Poland signed a long-term deal with Cheniere for future U.S. LNG supplies. Russia currently supplies over half of Poland’s natural gas demand but its long-term contracts are expiring in 2022. Despite the fact that Russian natural gas is piped, the price Poland pays for U.S. gas is 20-30 percent lower than for Russian gas.

Germany is expected to build its first LNG import facility to potentially access more U.S. gas. Germany has also been working with Russia to construct the Nord Stream 2 gas pipeline while pledging to support domestic LNG import facilities.

EIA in its Annual Energy Outlook projects that U.S. gas production will grow at almost twice the rate of U.S. demand, leaving a large amount available for export. By 2040, EIA projects that domestic production could reach 40 trillion cubic feet—almost 50 percent higher than today.

Conclusion

The growth in U.S. natural gas production in shale basins and offshore is expected to provide access to world markets through our vastly growing LNG terminals, as the United States becomes a major player in world gas markets. As outgoing U.S. Secretary of the Interior Ryan Zinke stated, “American strength flows from American energy, and as it turns out, we have a lot of American energy…Now, I know for a fact that American energy dominance is within our grasp as a nation.”