Key Takeaways

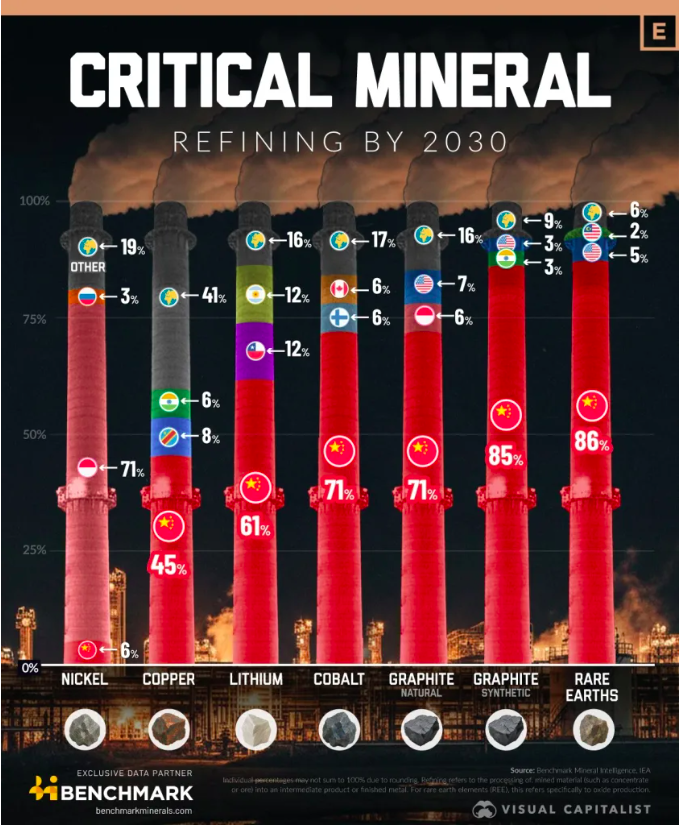

Critical mineral supply chains are highly concentrated within China, especially at the refining and processing stage, where the country currently controls 90% of the market.

It is expected to keep its dominance through 2030, controlling over 80% of the market in synthetic graphite and rare earths.

China has used its dominance as leverage in trade and other disputes with the United States and Japan.

Some critical metals, including copper and silver, which are key to the production of cars, military equipment, and more, have seen their prices soar due to supply shortages and/or restrictions.

China remains the dominant refined mineral supplier, both in terms of country of origin and overseas Chinese corporate-owned supply, as China has spent decades developing the industry. According to the Epoch Times, China controls about 90% of global capacity for the processing, smelting, and separation of these materials, as well as for the manufacturing of magnetic materials. While the United States, Australia, Brazil, India, and parts of Africa are establishing new mines, most of their concentrates still have to be shipped to Chinese refineries, where the country processes them with cheap coal power and lax environmental and other standards.

China’s dominance with regard to refined critical mineral supply is expected to continue through the end of the decade. It is expected to have a market share of over 80% in both rare earths and synthetic graphite. Despite the Trump Administration’s focus on onshoring critical mineral refining and processing, the United States is expected to gain only relatively small market shares in the natural and synthetic graphite and rare earth markets. Canada and Finland will each account for 6% of the refined cobalt production.

The Epoch Times explains that China knows it has the leverage and has used it recently during a trade war with the United States by restricting exports of rare earths, germanium, and other critical materials in 2025. In 2010, China cut off rare earth exports to Japan for about two months during a territorial dispute. China has again restricted exports of rare earths and rare-earth magnets to Japan to punish it for Prime Minister Sanae Takaichi’s remarks late last year suggesting the country could become involved in a conflict over Taiwan. China’s new rules for 2026 are restricting exports of tungsten and antimony, widely used in defense and advanced technologies. It is also limiting the export of silver in the same way it has restricted rare earths, as noted below.

Copper

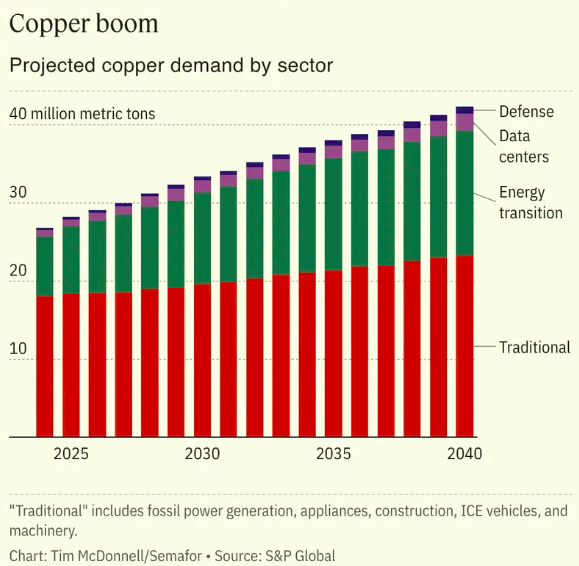

Via Semafor, although China dominates refined copper processing, global output is expected to become increasingly diversified, with about 55% of refined production forecast to come from outside China by 2030. Copper underpins modern economies, used in everything from consumer electronics and household appliances to electric vehicle batteries, artificial intelligence data centers, military drones, and construction and wiring. Supply is tightening as new mines are slow and costly to develop, while existing operations face rising costs as ore grades deteriorate. The market is already undersupplied, a problem compounded in 2025 when several of the world’s largest mines were temporarily shut by mudslides, earthquakes, and tunnel collapses. Analysts warn the supply gap could widen to as much as 10 million metric tons — roughly a quarter of projected demand — by 2040, keeping prices elevated. To ease shortages, governments will need to accelerate mine development, expand recycling, and broker new trade arrangements between producers, processors, and end users; the Trump administration has moved to encourage more U.S. mining, but results will take years to materialize.

Nickel

Indonesia is expected to remain the world’s dominant nickel refiner, accounting for 71% of global refined nickel production, but around 80% of Indonesian refined nickel production is currently owned by Chinese companies. Similarly, Chinese companies have invested heavily in upstream cobalt assets in the Democratic Republic of the Congo.

Rare Earths

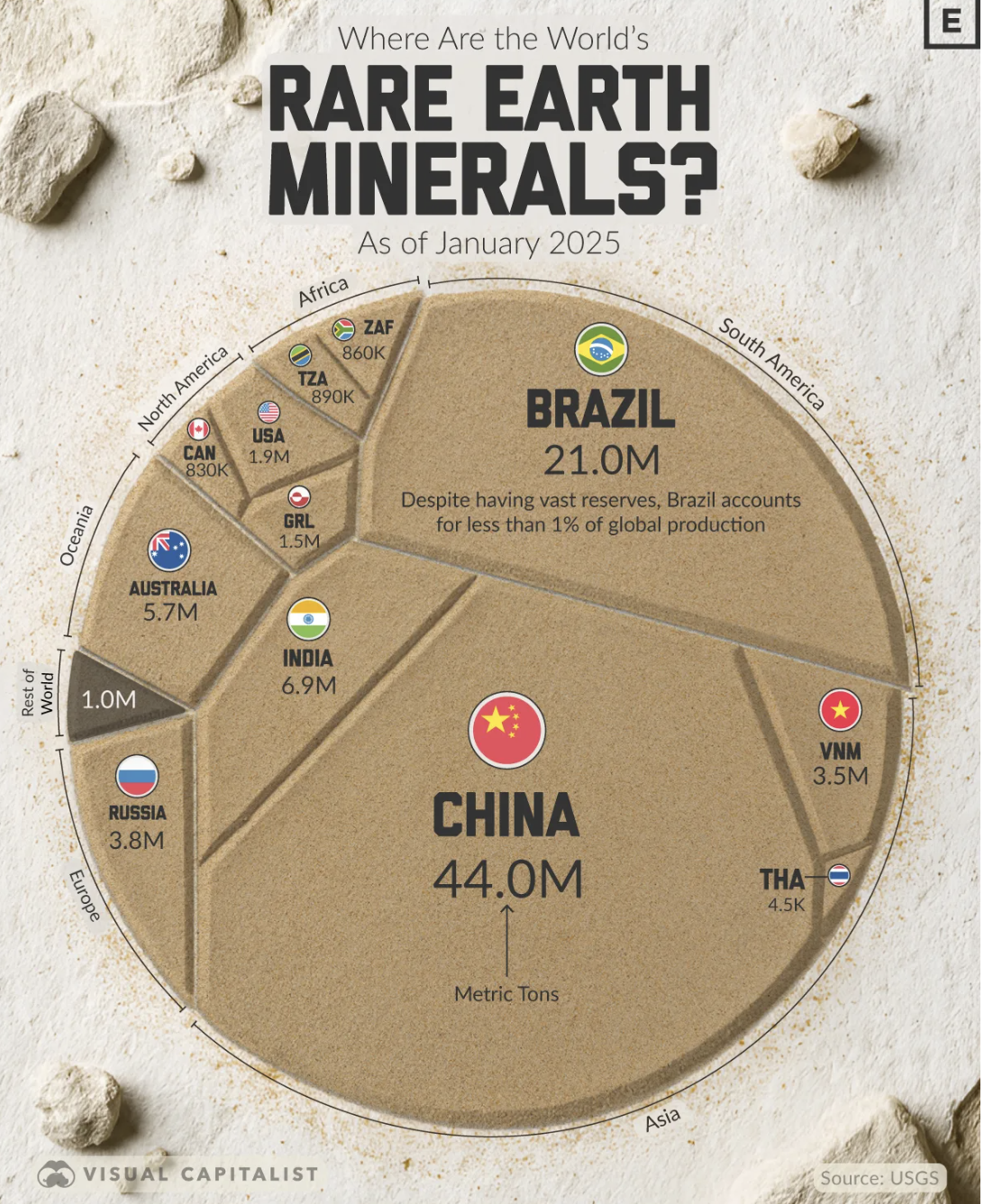

China holds nearly half of the world’s reserves, followed by Brazil. As reported by OilPrice, China has 44 million metric tons, about 48% of the world’s total of 91.9 million metric tons. Brazil has 21 million metric tons (23%), with large ionic clay and hard-rock deposits that have just begun development. Together, the top six countries account for roughly four-fifths of known reserves. (See graph below.)

OilPrice explains that the United States has just 1.9 million metric tons of rare earth reserves (2%), underscoring its reliance on trade and midstream processing to secure supply. In recent months, the Trump administration has sought to reduce U.S. dependence on Chinese materials by funding domestic mining projects, streamlining permits, and partnering with allies to diversify supply chains. In October, President Trump and President Xi Jinping agreed to reduce tariffs in exchange for China maintaining the flow of rare earth exports.

Silver

China, a top supplier of refined silver, began to enforce new export limits on the metal to ensure ample supplies for Chinese companies. Silver is used in manufacturing, especially by the automotive, aerospace, and defense sectors. Silver was recently added to the U.S. critical mineral list and may face new supply constraints due to these export restrictions that took effect in January.

According to the American Action Forum, “Chinese silver producers and distributors had to apply for permission to export in October based on export performance between 2022 and 2024. For new applicants, the domestic production threshold to receive approval was 80 tons, which effectively puts large, state-owned enterprises at the forefront of China’s silver exports. Out of 50 applications, six were rejected, which will further concentrate the market and raise global price-risk premiums as companies look to de-risk supply chains.” China was one of the world’s largest producers of silver in 2024, and has the fourth largest reserves.

Analysis

China dominates the processing of critical minerals and shows no sign of relinquishing this control anytime soon. The Trump administration is attempting to combat this control through trade policy, announcing via executive order “that it is necessary and appropriate to enter into negotiations with trading partners to adjust the imports of [processed critical minerals and their derivative products] so that such imports will not threaten to impair the national security of the United States.” Unfortunately, the Trump administration’s conclusion ignores the fact that permitting and regulatory issues are the main cause of the U.S.’s lackluster mineral processing industry. A lack of mineral processing facilities is a downstream effect of the fact that it takes 29 years to open a mine in the U.S.

For inquiries, please contact [email protected].