The following is testimony provided by IER’s Vice President for Policy, Kenny Stein, to the Senate Energy and Natural Resources Committee on January 11, 2024.

______

Near-term mass adoption of electric vehicles is a central element of the forced green transition sought by the Biden administration and heavily subsidized through the Inflation Reduction Act. But a major impediment to the rapid rollout of many of the energy technologies that would help achieve this forced transition is that they require far more minerals and materials than are currently being produced. As the International Energy Agency (IEA) explains:

An energy system powered by clean energy technologies differs profoundly from one fueled by traditional hydrocarbon resources. Solar photovoltaic (PV) plants, wind farms, and electric vehicles (EVs) generally require more minerals to build than their fossil fuel-based counterparts. A typical electric car requires six times the mineral inputs of a conventional car, and an onshore wind plant requires nine times more mineral resources than a gas-fired plant. Since 2010 the average amount of minerals needed for a new unit of power generation capacity has increased by 50 percent as the share of renewables in new investment has risen.

According to the IEA’s “sustainable development scenario,” these new energy technologies will require a 42-fold increase in lithium demand, a 25-fold increase in graphite demand, a 21-fold increase in cobalt demand, a 19-fold increase in nickel demand, and a 7-fold increase in rare earth demand by 2040 to meet carbon dioxide emissions goals set by some governments around the world.

New mining projects are not projected to keep up with this incredible increase in demand. For example, EV expert Steve Levine recently argued that “the EV industry is in a decades-long battery metals crisis.” He went on to explain that in 2022, lithium and nickel production only support the production of 3.8 million pure EVs, however, automakers said they wanted to make

7.7 million EVs in 2022.4 Levine used major metals production forecasts and calculated that by 2030 there will only be enough lithium and cobalt for 15.6 million EVs, while automakers say they want to produce over 40 million in 2030. What makes this situation even more unrealistic is that demand for lithium-ion batteries is not just coming from EVs, but also storage on the electrical grid made necessary by part-time renewable energy sources being mandated and subsidized into the system.

Not only are there projected shortages for minerals and materials used for EVs and batteries, but there is a massive project shortfall in necessary copper production as some of the world’s largest copper mines have operated for more than a century. S&P Global recently released a report which found that “Unless massive new [copper] supply comes online in a timely way, the goal of net zero emissions by 2050 will be short- circuited and remain out of reach.” S&P Global projects that copper demand would have to double between now and 2035 to meet the goal of net zero by 2050.

The increase in demand for these minerals and materials will put upward pressure on prices. For example, according to Benchmark Minerals Intelligence, from April 2021 to April 2022, the raw materials that constitute NCM (nickel, cobalt, magnesium) lithium-ion batteries increased in price by 164 percent, and the raw materials that make-up lithium-ion phosphate batteries increased by 393 percent. Prices have since come down, but these types of price swings can be expected to continue given ongoing government subsizidization of electric vehicles.

The problem is not just with minerals and materials shortages, but energy security as well. Russia’s leverage over Europe due to its dependence on Russian oil and natural gas is a reminder of the importance of energy security. The United States Geological Survey (USGS) recently estimated that there were 50 minerals critical to the security of the United States. In 2021, imports comprised more than half of the U.S. consumption for 47 of these mineral commodities, and the U.S. was 100 percent net import reliant for 17 of them.

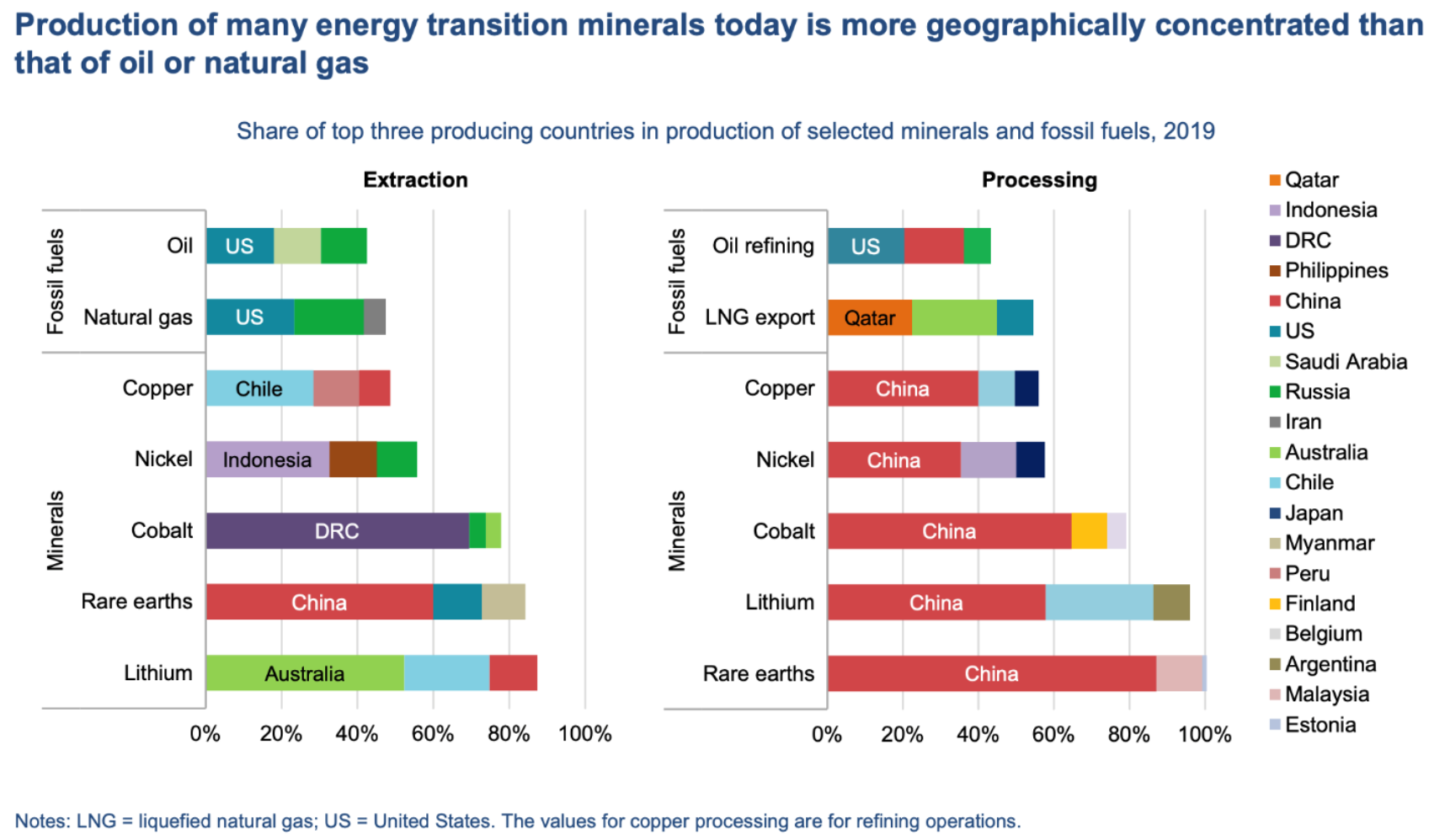

It’s not just the U.S. As the IEA has stated, “the production of many energy transition minerals today is more geographically concentrated than that of oil or gas.” The processing of these minerals is even more.9 China is the largest processor of copper, nickel, cobalt, lithium, and rare earth—processing between 35 percent and 85 percent of these minerals. At the moment, the United States and the rest of the world are utterly dependent on China to meet the growing demand for critical minerals and materials necessary for electric vehicles.

The minerals needed for electric vehicles have to come from somewhere, dug up out of the ground and processed into a usable form. Unlike oil and natural gas, which are found and produced around the world, the production of the main battery minerals is quite concentrated. In 2019 for example, the top three extractors of copper and nickel produced more than half of global production, and the top three extractors of cobalt, rare earths, and lithium produced 75- 85% of global production. In contrast, the top three producers of oil and natural gas (both of which include the United States) produce less than 50% of global production. But this mining concentration pales in comparison to the concentration in processing, where China dominates.

China now processes a majority of the world’s nickel, cobalt, lithium, graphite, manganese and rare earths, which are key inputs for wind turbines, solar panels, and batteries. For several of those categories, such as graphite, manganese and rare earths, China accounts for 80-100% of global production. China’s dominance goes beyond the processing itself; China also controls the manufacturing and production of many green energy products: around 80% of lithium-ion battery cell production; 80-90% of anode and cathode production; between 60-80% of polysilicon, wafers, crystalline silicon cells, and solar modules.

What all this means is that green energy is truly made in China. Thus, the vast spending from IRA subsidies will be spent on Chinese products and inputs and enrich Chinese companies. Now the IRA did include some incentives to try to produce many of these inputs domestically, but the process of opening a new mine stretches for many years if not decades. And that is assuming all goes well with the permitting and approval process, which has not been the case under the Biden administration, with mines such as Twin Metals and Polymet in Minnesota, Resolution and Rosemont in Arizona, and Pebble and the Ambler Mining District in Alaska, just to name a few prominent examples, all facing obstacles or outright disapproval. The processing of these minerals is also a very dirty and energy-intensive business, which is part of why so much of it is done in China where what minimal environmental standards as may exist are easily ignored if you have the right connections and cheap coal-powered electricity is on offer. Trying to build these processing facilities in the United States will inevitably be stymied by the National Environmental Policy Act or other environmental regulations, to say nothing of the lawsuits from every green organization under the sun (organizations which ironically also support increased use of green energy). Some final assembly of imported Chinese components will probably happen in the US in foreign-owned facilities in order to game IRA subsidy eligibility, but that façade cannot hide what’s really happening. To subsidize electric vehicles today is to subsidize China.

None of this is to say that electric vehicles are bad in of themselves. But there is little justification for massive subsidies and mandates for the purchase and use of electric vehicles as a public policy matter. In the near term, subsidies for electric vehicles enrich Chinese suppliers. Mandates that make conventional cars more expensive or less available, combined with the higher costs of electric vehicles, means that it is harder and harder for Americans to afford a vehicles at all. Thus current public policy is subsidizing the Chinese while making the lives of Americans harder.

Instead of hurting Americans and subsidizing Chinese companies, public policy should make it as easy and affordable as possible for Americans to purchase the vehicle that best fits their needs.

____

The testimony, and accompanying report, may be dowloaded here.