President Donald Trump recently accused major oil companies of “gouging” consumers by failing to lower gas prices at the pump quickly enough despite sharply falling crude oil prices. In a late-night Truth Social post, he instructed the Justice Department to immediately investigate. We have heard this clarion call before from numerous politicians, though admittedly it usually comes from the Democratic side of the aisle. Let’s set the record straight on this – again.

Gasoline prices at the pump often increase immediately when crude oil prices rise, yet they decline at a frustratingly slow pace when oil prices drop. This asymmetry frustrates drivers and fuels accusations of price gouging from politicians. The reason, however, stems from the economics of the petroleum supply chain, not conspiracy or corporate greed.

Gasoline sold today is typically refined from crude oil purchased weeks earlier. Refining, transportation, storage, and distribution to retail stations take time, often 2 to 6 weeks or longer, depending on logistics, contracts, and regional infrastructure. When crude oil prices fall sharply, refiners and retailers continue to process and sell fuel made from higher-cost inventory already in the system. Cheaper crude must first be purchased, refined, and moved through the pipeline before it reaches the pump. Gas stations, the vast majority of which are independently owned, rotate their existing stock gradually rather than dumping it at a loss. This creates a natural delay on the downside.

On the upside, the dynamic reverses. Rising crude prices prompt quicker adjustments because businesses look forward. They anticipate higher replacement costs for future inventory and begin raising prices to protect margins. Consumer demand also plays a role, as drivers often accelerate purchases when prices are expected to rise, thereby tightening near-term supply. This is not unique to gasoline. Similar inventory lags appear in many commodity markets with long production and distribution chains, from coffee to steel. The difference with fuel is its visibility at every corner station, and thus, the price is more politically sensitive.

Multiple economic studies have examined this “rockets and feathers” phenomenon, in which prices rise like rockets, but fall like feathers. After controlling for taxes, seasonality, competition levels, and other variables, the asymmetry persists across regions and time periods, though its intensity fluctuates with market conditions, refinery utilization rates, and inventory levels.

Importantly, researchers have found little evidence that the pattern results from widespread collusion among oil companies or retailers. Instead, it emerges from rational incentives to hold higher-cost inventory during price drops and to hedge against future cost increases during price rises.

Despite periodic political claims of gouging during, official findings tell a sustained and consistent story. In 2008, in a period of very high gasoline prices, the Institute for Energy Research asked a straightforward question: How many times has the Federal Trade Commission found evidence of price gouging by energy companies? The answer was none. Subsequent investigations into the 2021–2022 price increases reached the same conclusion: price movements reflected global crude prices, supply disruptions, OPEC+ decisions, refinery outages, and seasonal demand, not domestic collusion or misconduct. Any investigation done by the Trump administration will surely return the same findings.

Proposals for price-gouging statutes or windfall-profits taxes surface quickly whenever prices rise, because they allow politicians to assign blame to identifiable “big oil” villains. These measures rarely lower prices at the pump. In many cases, they risk creating the opposite problem in shortages. When retailers cannot recover replacement costs or face penalties, they may reduce supply or exit marginal markets. Historical precedents are instructive, as Nixon-Carter era price controls in the 1970s produced long lines, rationing, and widespread shortages. Additionally, the 1980s windfall profits tax on domestic producers reduced investment, slowed U.S. output, and increased reliance on imported oil. Raising taxes or imposing punitive measures on U.S. energy companies today would likely produce similar results with higher long-term costs for consumers and greater dependence on foreign suppliers.

If the Trump administration wants gas prices to fall (as we all do), it should withdraw the EPA’s latest Renewable Fuel Standard (RFS) mandates. The RFS program, created in 2005, requires refiners and importers to blend ever-increasing volumes of biofuels into the nation’s gasoline and diesel supply. Originally designed to reduce dependence on foreign oil, the program has become obsolete: the United States is now a net exporter of petroleum and refined products.

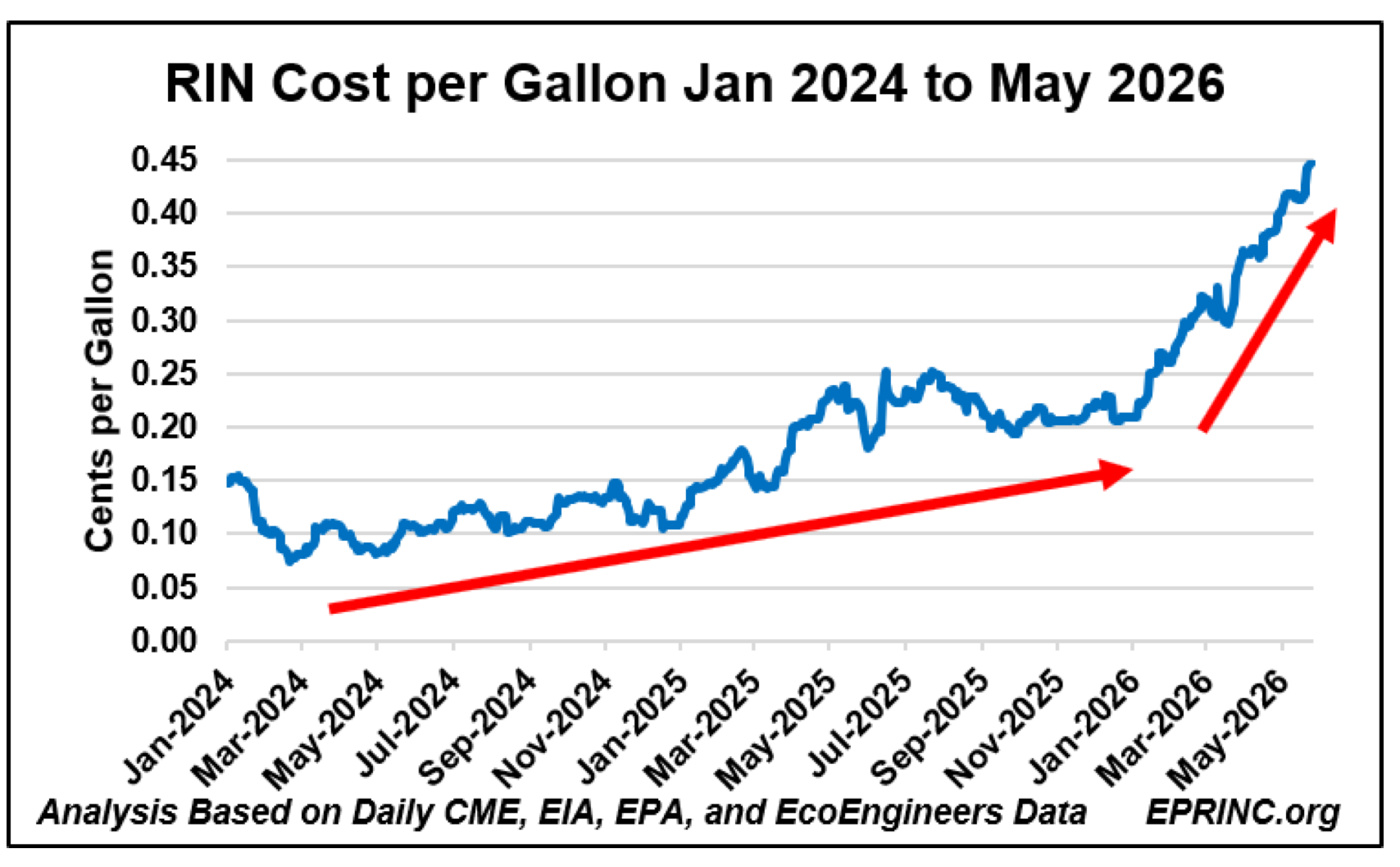

According to EPRINC, the estimated additional cost from the RFS has risen sharply from 15 cents per gallon in January 2024 to 45 cents per gallon as of May 2026. Based on the current 45-cent-per-gallon estimate and annual U.S. gasoline consumption of approximately 140 billion gallons, the total annual economic burden on consumers exceeds $66 billion.

As you can see, these RFS mandates function as a regressive tax on American workers, families, and businesses, hitting hardest at the pump, even as inflation and high energy costs remain top concerns.

Gasoline prices are a predictable consequence of how crude oil is refined into fuel at the pump. Inventory lags, forward-looking pricing on the way up, and gradual stock rotation on the way down explain most of the observed behavior. Regulatory records and economic studies show that market fundamentals, rather than malicious behavior, drive the vast majority of price movements. Blaming energy companies may score short-term political points, but it distracts from the policies that actually influence long-term supply. Withdrawing the EPA’s latest RFS mandate is a more tangible path to lower prices than another senseless investigation from the Department of Justice.