This post is converted from Dr. David Kreutzer’s official comment submitted June 21 on behalf of the Institute for Energy Research for Docket No. OMB-2021-0006.

_________

The Technical Support Document (TSD) on the social cost of carbon, methane, and nitrous oxide interim estimates under Executive Order 13990, like the previous ones on the social cost of carbon dioxide in 2010 and 2016, is almost more fiction than science. Though the integrated assessment models that generate the cost estimates are academically interesting and mathematically sophisticated, they are not robust enough to produce estimates with the confidence necessary for regulating such a large fraction of our economy. Further, at least as employed by the Interagency Working Group (IWG), the assumptions and inputs for these models exaggerate the cost estimates.

In work with my former colleague, Kevin Dayaratna, we showed reasonable variations in the assumptions and inputs for the integrated assessment models (IAMs) led to wild variations in estimates for the Social Cost of Carbon. In fact, some of the estimates were negative, indicating CO2 emissions generated positive externalities, implying CO2 emissions should be encouraged rather than reduced.

Without endorsing any of the social cost of greenhouse gases (SC-GHG) estimates, I will point out several of the more egregious problems with the calculations.

Too Much Warming

The IAMs translate CO2 levels to global warming using estimates of equilibrium climate sensitivity (ECS) or, sometimes, transient climate response (TCR). The working group should not use model-generated values (as they have done). Empirical estimates, based on actual historical data, consistently produce lower estimates of warming and, therefore, lower and more reasonable cost estimates.

Dayaratna, McKitrick, and Kreutzer employed an empirical ECS in two of the three IAMs used by previous working groups. We found this one improvement reduced SCC estimates by 30-80 percent.

The working group should use empirical estimates of ECS and TCR. At a minimum, they should provide the SC-GHG estimates using the lower ECS and TCR estimates for comparison.

Discounting

In principle, the SC-GHG is an economic tool to guide decisions on how much we should spend to reduce greenhouse gases. The social cost of carbon dioxide, methane, or nitrous oxide is a measure of the value of cutting one ton of the gas and, therefore, the maximum we should be willing to spend to reduce emissions by one ton.

Since the regulatory process would cut emissions now, for benefits in the future, this process is an investment decision. The regulations or taxes guided by the SC-GHG would impose costs in the present for benefits in the future. People in the future receive net benefits from costly actions taken by people today. Because there are unlimited possible investment activities and limited resources available to pay for them, efficiency mandates that investment undertaken should provide a future benefit that is at least as large as the highest valued reasonable alternative investment. This is the basic concept of opportunity cost. Resources used to make a poor investment today, preclude using those resources to make a better investment. Making a worse investment costs us the benefit not received from the better investment.

Different investments have different patterns of costs and benefits across time. Given these differing patterns, it is not a simple matter to compare a given investment to others. To overcome these difficulties, a tool called discounting is used.

Discounting is simply compounding in reverse. The discounted value of the future cost/benefit, or present value, is the amount that would need to be invested today to generate the future value.

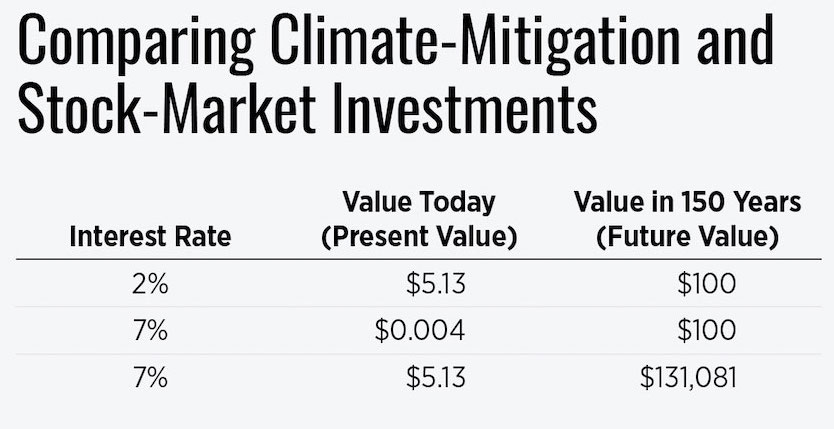

For instance, using seven percent as the rate of return on an alternative investment, the discounted present value (or just present value) of $100 benefit received 150 years from now is only $.004, today. If seven percent is that rate of return that could reasonably be expected from an alternative investment, then we should spend no more than $.004 today for each $100 received 150 years from now.

Some have argued that this market-based rate of return is too high to use as the discount rate because it undervalues benefits to those living in the future. They have suggested it would be more equitable to discount at two percent (or even lower).

One hundred dollars discounted for 150 years at two percent gives a present value of $5.13. This means we should invest up to $5.13 today to create a $100 benefit in 150 years, but that would be a bad deal for the future.

Discounting and the discount rate (the rate of return number used in discounting) are not tools for weighing the relative value of people’s welfare in different time periods, instead they are tools for ranking different investments. For example, if grandparents were creating a trust fund for their grandchildren and they could invest the money at either two percent or seven percent, choosing the worse investment (two percent) is not more equitable, nor would it be a sign that the grandparents loved their grandchildren more than if they invested at seven percent.

Table 1 helps illustrate this situation.

The present value of $100 received in 150 years would only be $.004 today when the discount rate is seven percent. Using the “more equitable” discount rate of two percent per year would give a present value of $5.13. Eschewing the seven-percent rate for the two-percent rate argues for spending up to $5.13 on greenhouse-gas mitigation for a $100 climate benefit 150 years later. However, investing that $5.13 at seven percent would provide a benefit of $131,081 150 years later, clearly a much better deal for the future.

Table 1

The Ramsey Equation?

The technical support document uses the Ramsey equation to determine the discount rate(s). This is a logically flawed approach. The Ramsey equation describes the productivity of capital (and, hence, the appropriate opportunity cost of capital to use as a discount rate) in an optimal equilibrium. This rate of return is a function of the rate of pure time preference, the income elasticity of utility, and the real growth rate of the economy. Neither the rate of pure time preference nor the income elasticity of utility is directly observable. Even if they were, aggregating and homogenizing these very personal values presents serious conceptual and practical hurdles.

However, a greater flaw is that we already have an observable return to capital, and it is greater than the Ramsey-derived rates in the TSD. The TSD’s implicit argument that the observed return to capital is higher than optimal and optimal decisions for allocating capital across time (in particular, investing in climate improvement) should use the Ramsey-derived optimal rate. Unless, this Ramsey optimality holds across all investments, it is not optimal to use this calculated rate for discounting. The Ramsey-derived rate in the TSD is significantly lower than the observed rate of return to capital. We can do better for those in the future than the low Ramsey-optimal rate.

The inflation-adjusted (before-tax) rate of return to capital is at least seven percent. This is true looking at the entire New York Stock Exchange for the past two centuries and is similar to the return to the Standard and Poor’s 500 for nearly the past century.

By using the Ramsey-derived rates, the authors of the TSD dream up an economy organized according to their own preferences. In their imaginary world, investment and saving levels are so much higher than what we know to be true, that the Ramsey equation (with the authors’ choices for pure time preference and income elasticity of utility) fits. Whether the TSD’s version of optimality is actually optimal is debatable, but we need not bother with that debate since the TSD’s optimality does not hold in the real world.

Equity

Basing their appeal on concerns for equity, the IWG argues for lower than efficient rate of return when discounting future benefits of greenhouse-gas mitigation. As noted above, getting a worse return on climate investment does not provide a greater benefit for future generations, but odder still is the notion that equity requires reducing the welfare of the poor in order to increase the welfare of the rich.

The IWG projects impacts of current greenhouse-gas emissions for nearly 300 years. That is, it estimates the damage done in the year 2300 from today’s emissions. It is a terrible policy to make investments that return $100 instead of $131,081, but it is virtually brain-dead to argue the bad return is justified on equity grounds. Those alive centuries from now are almost certain to be much wealthier, healthier, and possessed of technology to better overcome any adversity—including climate change.

One hundred and fifty years ago, the average American earned about one-fifteenth as much as the average American today. Similar growth is expected over the next 150 years. Taking from the poor to give to those twenty or more times as rich is no justification for inefficient investment.

Summary

- The IWG should use empirically determined equilibrium climate response and transient climate response values in the integrated assessment models.

- The IWG should discount future costs and benefits with a discount rate that is at least seven percent per year.

- Since future generations are likely to be orders of magnitude wealthier than the current one, if anything, appeals to equity argue for raising the discount rate, not lowering it.