The Energy Information Administration (EIA) in its August Short-Term Energy Outlook (STEO) is forecasting higher oil production than it did in its July Short-Term Energy Outlook and lower oil prices for the second half of 2013 compared to earlier this year. The increased oil production is expected mainly onshore on private and state lands. EIA continues to forecast lower oil production in the federal offshore Gulf of Mexico for 2013 and only a slight increase in 2014. Oil production in Alaska is expected to continue to decline over the next 2 years in EIA’s forecasts.[i]

Oil Prices

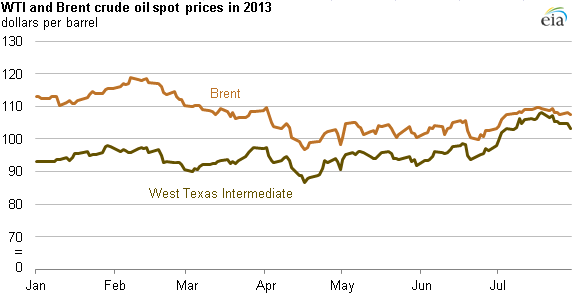

Oil prices are expected to drop for the second half of the year, making the Brent crude oil price for 2013 average almost $106 per barrel, and West Texas Intermediate’s oil price average almost $97 per barrel. EIA expects the Brent oil price to average about $100 a barrel and the West Texas Intermediate price to average almost $93 per barrel in 2014.

The interesting aspect relating to the price data is that the spread between the price of West Texas Intermediate crude oil and Brent crude oil has narrowed, averaging $3 per barrel for the month of July from an average of $18 per barrel in 2012. The reason EIA cites for the narrowing of the spread is: “The strong demand for light, sweet crude oil in the Midwest and new pipeline capacity to deliver production from the West Texas Permian Basin directly to the Gulf Coast contributed to the price of West Texas Intermediate rising relative to Brent crude oil.”

Source: Energy Information Administration, http://www.eia.gov/todayinenergy/detail.cfm?id=12391

The spread had reached wide levels in 2012 as increasing oil production from North Dakota and Texas outpaced the ability of the existing pipeline infrastructure to bring that oil to refineries on the Gulf Coast. As a result, shippers had to turn to more expensive modes of transport (railroads and trucks), causing the price of inland domestic oil to decrease to account for the increased shipping costs.

Thus, EIA is indicating that the increased pipeline capacity is no longer keeping domestic crude oil land locked at the terminal in Cushing, Oklahoma. Several new pipelines and crude-by-rail terminals came on line in early 2013.[ii] The new pipelines, which are less expensive than rail and truck, have supplied domestic crude oil to Gulf Coast refineries without incurring the higher shipping costs. And, according to EIA, it has been the relief of the bottlenecks that has enabled domestic light sweet crude oils that are of similar quality to Brent crude to displace some U.S. oil imports, in turn keeping Brent crude oil prices low. [iii]

EIA expects the price difference between West Texas Intermediate and Brent crude to widen to $6 per barrel by the end of 2013 as oil production in the United States and Canada increases.

Oil Production

Domestic crude oil production in July was at the highest monthly level of production since 1991, averaging 7.5 million barrels per day. EIA now expects production to be about 0.1 million barrels per day higher than its July STEO forecast, averaging 7.4 million barrels per day in 2013 and 8.24 million barrels per day in 2014. That is an increase of 14 percent in 2013 from an average production level of 6.5 million barrels per day in 2012. The majority of the increase is expected to come from onshore production in the Williston and Permian Basins as federal offshore Gulf of Mexico production and Alaskan oil production both decline in 2013. Offshore production from the Gulf of Mexico is forecast to average 1.25 million barrels per day in 2013, down from 1.27 million barrels per day in 2012, and 1.39 million barrels per day in 2014.

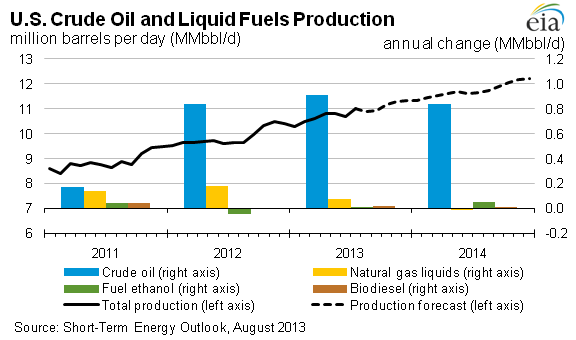

Crude oil is only one component of our domestic petroleum production. Also, contributing to domestic petroleum production are natural gas plant liquids and biofuel production in the form of ethanol and biodiesel. The graph below shows the annual change in each of these components based on data for 2011 and 2012 and EIA’s forecast for 2013 and 2014, using the right hand axis. Also, shown is total petroleum liquids production that is the black line, measured by the left-hand axis. Not shown is another component of liquids petroleum supply, which is refinery gain that occurs in the conversion of crude oil to petroleum products that increases the volumetric output.

Source: Energy Information Administration, http://www.eia.gov/forecasts/steo/images/Fig13.png

{kind=link}

Increased domestic oil production along with lower oil demand and increased petroleum product exports has resulted in a lower share of net oil imports. U.S. net imports of liquid fuels reached their highest level in 2005 totaling 12.5 million barrels per day and have been falling ever since. In 2012, they averaged 7.4 million barrels per day. EIA expects net liquid fuel imports to continue to decline, averaging 5.6 million barrels per day by 2014. The share of total U.S. petroleum consumption met by liquid fuel net imports peaked at 60.3 percent in 2005, falling to an average of 40 percent in 2012. EIA expects the net import share to continue to fall to 30 percent in 2014–the lowest level since 1985.[iv]

Conclusion

Production increases of crude oil are helping the United States to lower its oil imports to levels not seen in 3 decades. These increases are primarily on private and state lands where permitting takes significantly less time than on public lands that are administered and regulated by the federal government. Further, new technology such has hydraulic fracturing coupled with directional drilling has brought additional production that was unattainable just a decade ago. Obviously, this is good news for U.S. consumers.

Besides the pure benefits of increased production to the energy system and our economy, U.S. oil prices are having a dampening effect on North Sea Brent crude oil prices. This occurred once the bottleneck at the terminal in Cushing, Oklahoma was alleviated when new pipelines came on line earlier this year. According to EIA Administrator, Adam Sieminski, “the boom in U.S. oil production is helping to hold down global oil prices, and so is benefiting American consumers. Greater U.S. exports would actually help keep domestic prices lower by enhancing the global trend.”[v]

Imagine the effect even more production could have on world oil prices if the Keystone Pipeline could bring additional crude down from Canada and North Dakota or if the federal government reversed course and followed the lead of the states in regulating oil and natural gas production instead of working to restrict development.

[i] Energy Information Administration, Short-Term Energy Outlook, August 6, 2013, http://www.eia.gov/forecasts/steo/

[ii] Energy Information Administration, Spread narrows between Brent and WTI crude oil benchmark prices, August 5, 2013, http://www.eia.gov/todayinenergy/detail.cfm?id=12391

[iii] The Guardian, U.S. oil boom pressures import prices, helping drivers, August 6, 2013, http://www.energyguardian.net/us-oil-boom-pressures-import-prices-helping-drivers?utm_source=&utm_medium=email&utm_campaign=7919

[iv] Energy Information Administration, Monthly Energy Review, http://www.eia.gov/totalenergy/data/monthly/pdf/sec3_7.pdf

[v] Bloomberg, Senators Grill Refiners Over High Prices Amid Oil Boom, July 16, 2013, http://www.bloomberg.com/news/2013-07-16/senators-grill-refiners-over-high-prices-amid-oil-boom.html