- As oil prices near $100 per barrel, the United States finds itself with lower supplies at the critical oil hub of Cushing, Oklahoma.

- Physical and technical limitations also reduce the efficacies of those supplies and reduce their value to consumers when stock levels are very low.

- Rig counts for new wells to produce more oil have been falling despite EIA’s prediction of record production this year.

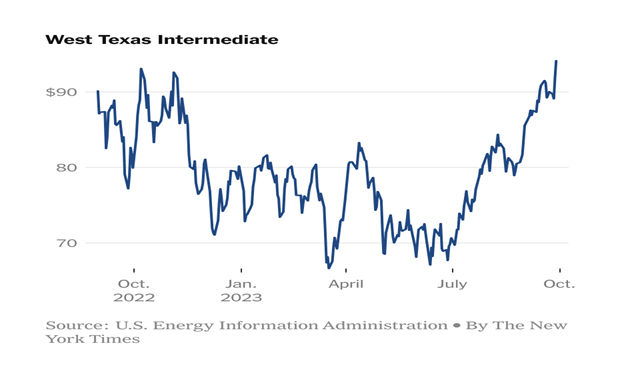

The Energy Information Administration is forecasting record annual oil production for this year at 12.78 million barrels per day—7.3 percent higher than last year’s production and 3.8 percent higher than oil production in 2019. The 2023 expected level of production is in spite of the policies that President Biden has instituted against the industry, as we have been documenting since Biden took office. But, consumers need to be aware that the indicators for prolonged records of production are not there. U.S. oil and gas rig counts are falling precipitously and U.S. oil stockpiles at the key Cushing, Oklahoma, storage hub are at their lowest level in 14 months due to strong refining and export demand. Traders and analysts are concerned about the quality of the remaining oil at the hub and the potential to fall below minimum operating levels. Further drawdowns at Cushing could provide upward pressure on oil markets as it would compound supply tightness from OPEC+ supply cuts. Brent oil was recently trading near $94 a barrel and West Texas Intermediate oil (WTI) was trading over $90 a barrel.

Since hitting a two-year high in June of over 43 million barrels, Cushing’s levels have dropped to just under 23 million barrels on September 15—a drop of 47 percent and the lowest since July 2022. Tank storage of below 20 million barrels, or between 10 percent and 20 percent of Cushing’s 98+ million barrels of capacity, is considered close to an operational low because below those levels, the oil is difficult to remove. If the oil level drops too low, the oil can get sludgy and even if it is obtainable, it would be unusable. Water and sediments settle at the base of storage tanks, making the oil at the bottom unable to meet quality standards for refiners or exporters. While some tanks have outlets at the bottom that can be used to empty oil and sludge, others do not. At the lower storage levels, it becomes more expensive for companies to get the remaining low value oil out of the tanks.

Roofs of storage tanks also float on the oil, preventing vapors from building up or escaping into the atmosphere. When the legs of the roofs touch the base, it creates a gap between the oil and the roof, causing combustible vapors to form.

Autumn maintenance at refineries could help build stocks somewhat, but refiners may exit maintenance quickly and run full out to keep up with the high petroleum product demand. Planned maintenance will peak in mid-October and cut refinery oil intake by about 1.8 million barrels per day, greater than last year’s fall maintenance peak of 1.5 million barrels per day. Typically, when Cushing inventories drop, relative prices at the hub increase to attract barrels from the Permian and limit outflows to the Gulf Coast. Alternatively, pipeline or storage terminal operators may limit outflows for operational purposes as inventories near the floor.

Cushing is strategically located to receive oil from top U.S. shale fields and Canada and its tanks are tied to pipelines that supply U.S. mid-continent and southern refineries and funnel oil to Gulf Coast export ports. Since Cushing is the delivery point for the WTI futures contract, the stock levels at Cushing are among the oil market’s most closely followed trends. Inventories there are now near their 2014 lows below 20 million barrels. In 2014, major consequences were avoided as stocks were quickly rebuilt due to rising prices at the hub and as the United States was not an oil exporter due to a 40-year export ban that was lifted in 2015. Any incremental production is likely to get exported as the world is hungry for oil and much U.S. shale production is more suited by quality for foreign refineries.

Conditions Are Ripe for Higher Oil Prices

According to Harold Hamm, Chairman of Continental Resources and a pioneer in shale oil boom, oil is headed as high as $150 a barrel unless the U.S. government does more to encourage exploration. Such prices will send a shock through the system. He also believes that oil and gas will still be around in a century’s time despite growing calls for the world to wean itself off fossil fuels. Shale executives are issuing calls for the Biden administration to adopt consistent policies that will allow them to drill more oil and that transcends politics–policies that can last from one administration to the next. Failure to do so will lead to tighter supplies and even higher prices. After reaching an all-time high in July, oil production in U.S. shale fields is contracting and government analysts are forecasting a third straight monthly decline in October. Oil output in the Permian Basin will peak one day, as it already has in rival shale fields such as the Bakken region of North Dakota and the Eagle Ford in Texas, although additional technological progress can turn in-place resources into reserves.

According to Hamm, when federal leases were halted by the current administration, it took a whole year to modify drilling plans because not getting a permit means executing “plan B.” The chronic underinvestment in new production from poor policies can result in repercussions such as Europe’s supply crisis last year. Producers cautioned against a speedy energy transition when the world is not quite ready to give up fossil fuels and with a global population that is set to expand rapidly. The focus on ESG and clean energy over the past several years has taken away investment from oil and gas, even though oil demand continues to increase. Fossil fuels still make up about 80 percent of primary energy consumption and the world is demanding more energy of all kinds.

Conclusion

Cushing’s tank farms have been drained by strong refining demand, increasing oil exports and future prices that have been weaker than spot prices. High interest rates have also pushed up the costs for storing oil, encouraging outflows. Because the oil levels at Cushing are an indicator for the market, oil prices are likely to go higher unless stocks are quickly replenished, which is not likely. Rather, federal policies are needed that are consistent and that can transcend administrations to encourage oil and gas development. Biden and his administration have been doing the opposite since taking office in January 2021 and have even sold off 260 million barrels of oil from the Strategic Petroleum Reserve to keep gasoline prices in check before the mid-term election last year.