Key Takeaways

Europe is facing higher costs to secure natural gas supplies for next winter due to its own depletion and the conflict with Iran.

Europe’s gas storage levels were below normal when hostilities began. Still, Qatar’s inability to move LNG through the Strait of Hormuz and the closure of its LNG facility have made LNG more expensive, as the United States and Australia are running near capacity.

Europe now relies on LNG for more of its natural gas supplies than it has historically, after reducing flows of pipeline gas from Russia in the wake of its invasion of Ukraine.

Prospects are that Europe will have much higher energy bills as a consequence of the Iran conflict and poor planning.

Europe’s task of refilling natural gas storage for next winter has become more expensive, as Qatar has stopped LNG production and shipments due to the U.S.-Israel conflict with Iran, raising global prices, and due to Europe’s poor planning. Europe is refilling its gas storage facilities after using a sizable amount of natural gas this winter for heating and power production, leaving stocks well below normal levels. Europe turned to LNG after cutting off most of its pipeline gas supplies from Russia due to its invasion of Ukraine. As a result of the transition away from Russian natural gas, Europe expects to get about 45% of its gas supplies from LNG this year, up from 19% before Russia invaded Ukraine. The LNG price increases do not significantly affect U.S. domestic natural gas consumption, as the United States has abundant natural gas resources that it produces and transports, priced outside the global LNG market.

EU gas storage is at best 30% full. Germany’s inventories were about 21.6% in late February, while France’s inventories are also in the low-20s. European buyers in Europe need to find the equivalent of around 700 cargoes of LNG, or 67 billion cubic meters, to fill storage this summer, totaling about 180 cargoes (17 billion cubic meters) more than last year. While most of it will come from LNG cargoes, some natural gas will be shipped via pipeline from Norway, Algeria, and Russia. However, Norway, Europe’s largest gas supplier, is already producing at maximum capacity.

Gas futures in Europe nearly doubled in the days after the Iran conflict began, hitting their highest levels since 2023. After Qatar shut down its gas fields, which provide a fifth of global LNG supply, natural gas prices in Europe rose nearly 50%. According to Reuters, Europe’s bill for the extra 180 cargoes had increased to about $10.1 billion from $6.7 billion before the attack on Iran. For the full 67 billion cubic meter refill, the news agency reports that the price would increase by about $13.6 billion to $40 billion should gas prices remain elevated.

Qatar provides an estimated 12% to 14% of Europe’s LNG imports. In 2025, Qatar accounted for 3.5% of EU gas supply, while the U.S. share was 25.4%.

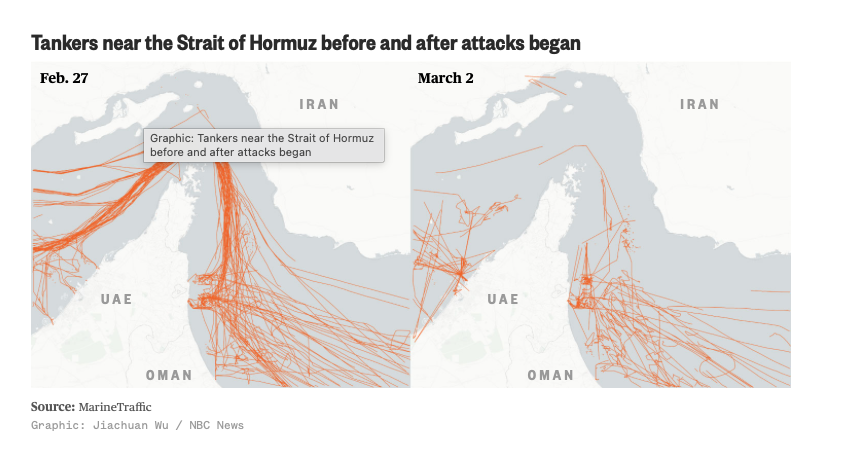

About 20% of global LNG supply passes through the Strait of Hormuz, where ship traffic has stopped due to the war. As reported by Reuters, based on one month of disruption, about 7 million tons of LNG (9.7 billion cubic meters) would be removed from the global market. Europe could effectively lose around 5.5 million tons (7.6 billion cubic meters) due to competition from Asia for available cargoes, which receives about 80% of the LNG that flows through the Strait.

Despite the U.S. being the world’s largest LNG producer, U.S. LNG plants are running at or near full capacity. New trains scheduled to come online in the near term will add no more than 2 billion cubic feet per day of capacity, limiting the industry’s ability to replace supply lost after Qatar halted production at its Ras Laffan LNG plant.

Venture Global, which has been selling 2 million metric tons per month in commissioning volumes on the spot market, can redirect cargoes as its Plaquemines plant in Louisiana ramps up. Still, that volume would cover only a fraction of the shortfall. Cheniere Energy also has some ability to redirect cargoes. Cheniere recently began production at Train 5 of its Stage 3 expansion at Corpus Christi, with a capacity of 1.5 million tons per year. That train should take about a month to reach full output, but most of its output has been contracted out. There is only about 5% of U.S. LNG capacity available to cover the shortfall, as most U.S. cargoes are locked into long-term contracts. Australia, another major LNG producer, is in a similar situation.

Gas supplies in Egypt and Turkey are also affected by the war with Iran. Egypt receives pipeline gas supplies from Israel, which temporarily shuttered some gas fields as a precaution against Iranian attacks. Turkey gets pipeline gas exports from Iran, which, if interrupted, would put additional pressure on LNG supplies.

Analysis

The war with Iran has elevated LNG prices as Qatar has halted production at its Ras Laffan LNG plant, removing about 20% of LNG supplies from the market. Shipping traffic in the Strait of Hormuz has also been severely reduced by the conflict, from which 20% of the LNG is shipped, most of it to Asian markets. Europe’s natural gas supplies are below normal levels for this time of year, as more gas was used for heating and power generation this winter, and Europe did not immediately act to refill. Restocking its storage facilities will thus be more expensive due to the lack of LNG from Qatar and because other major suppliers, the United States and Australia, have limited excess LNG capacity, as most of the LNG is secured under long-term contracts. There will be fierce global competition for whatever LNG is available on the spot market, particularly under a prolonged conflict.

For inquiries, please contact [email protected].