A “bubble” in financial terms typically refers to a situation where the prices of certain assets, such as stocks or real estate, become significantly inflated beyond their actual value. This is often driven by speculative investing, where people buy assets solely with the expectation that their prices will keep rising, rather than based on their fundamental value or performance.

In the context of “green energy,” which refers to renewable and supposedly environmentally friendly sources of energy like solar and wind, a potential “green energy bubble” could refer to a situation where there is an unsustainable and excessive investment in companies, projects, or technologies.

Here’s how such a bubble could form:

- Hype and Speculation: As concerns about climate change and environmental sustainability grow, there might be a surge in public and investor interest in green energy solutions. This heightened attention could lead to speculative investing in green energy companies, causing their stock prices to rise rapidly.

- Government Policies and Incentives: Favorable government policies, subsidies, or incentives designed to promote the adoption of green energy could attract a large influx of investment into the sector. Investors might see these policies as opportunities for high returns. Additionally, central bank policy plays an important role in driving periods of boom and bust.

- Media and Public Sentiment: Non-stop positive media coverage and a strong public sentiment toward green energy could fuel the perception that investing in these companies is a guaranteed path to success, attracting even more speculative investors.

- Overvaluation: As more investors pour money into green energy companies, their stock prices could become disconnected from their actual earnings and growth prospects.

- Reality Check: At some point, the market may realize that the valuations of green energy companies have become inflated and unsustainable. This realization could trigger a sell-off as investors rush to cash in their profits, leading to a rapid decline in stock prices.

- Bursting of the Bubble: If the bubble bursts, it could have broader implications for the economy and investor confidence, like past financial bubbles. There could be bankruptcies, job losses, and a general loss of trust in the green energy sector, even though the underlying technologies and goals are still valid.

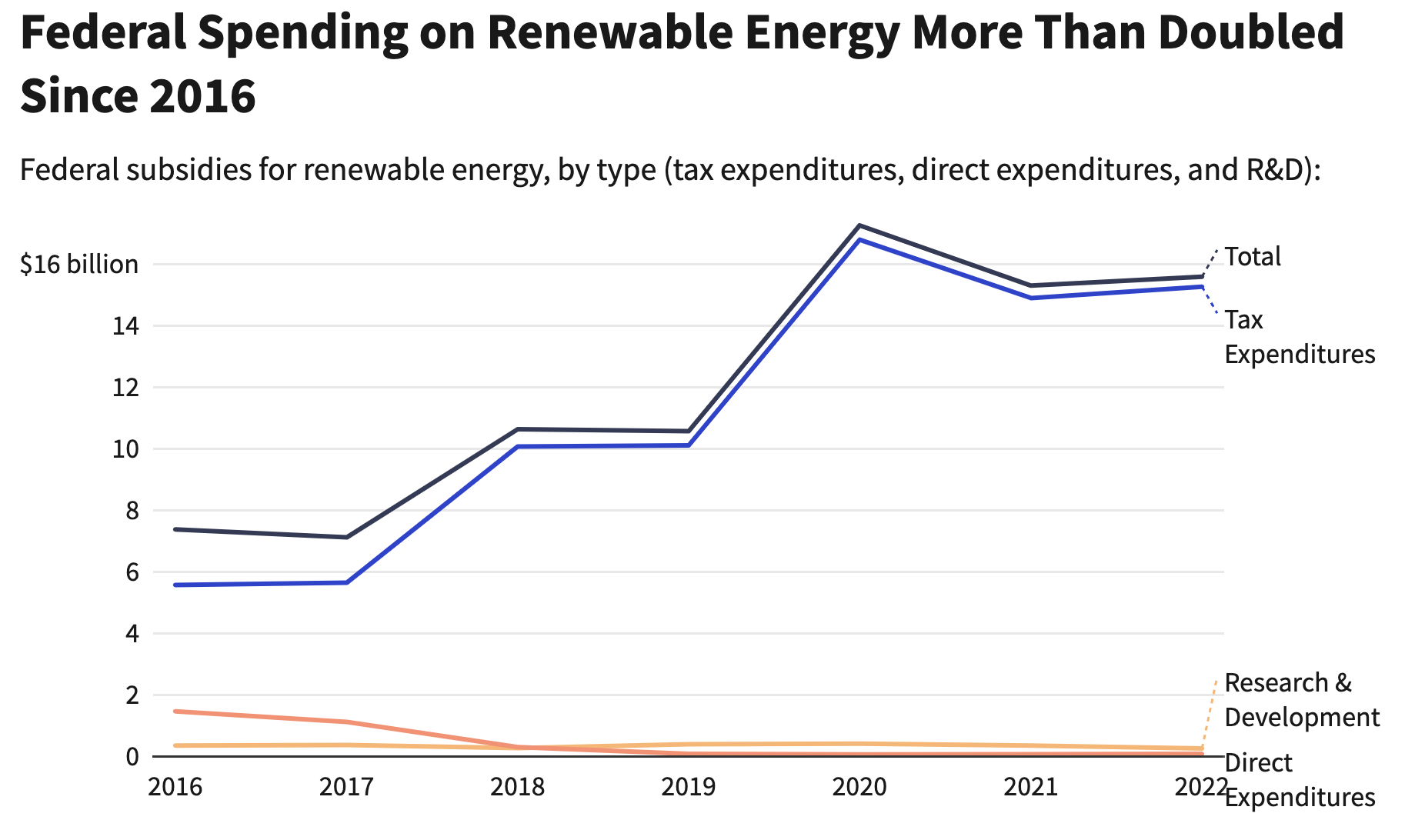

The governmental energy bubble starts with federal subsidies for renewable energy projects more than doubled from 2016 to 2022, according to a recent report from the U.S. Energy Information Administration (EIA). As a result, companies like First Solar now receive nearly 90 percent of their operating profit from government subsidies.

It’s worth contextualizing all of this with the backdrop of our recent monetary policy: the shift from low to high interest rates to try to tame inflation.

As Michael Munger explains:

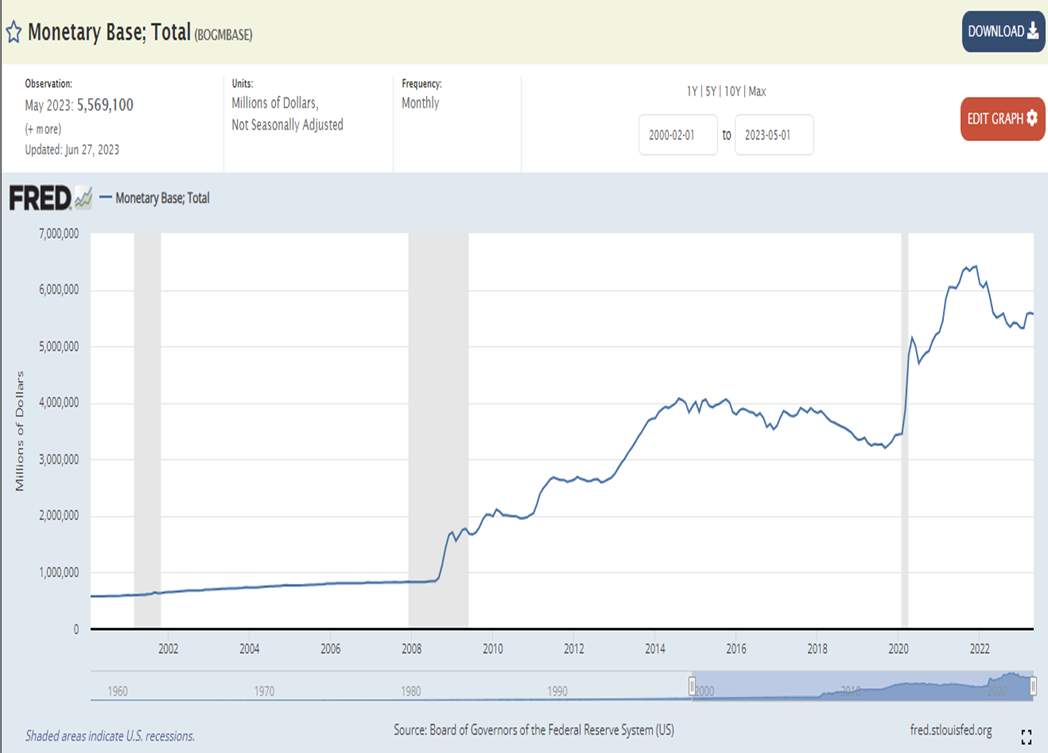

Is it plausible to think that there has been such a large growth in the US money supply that the increase in prices is old-fashioned inflation, rather than a real expansion of economic activity? Consider the table below, from the St. Louis Fed “FRED” website:

The “monetary base” has increased before; it was increased by $1 trillion in 2009 in response to the “Great Recession.” But look at 2020: The monetary base increased by $3.5 trillion in two years. That is an unimaginable infusion of currency into the hands of banks, companies, and …well, almost everyone, when you consider the enormous transfers and “stimulus funds” shoveled out during the COVID shutdown. The government had a highly expansionary fiscal policy, accommodated by an even more highly expansionary monetary policy from the Federal Reserve.

The resulting inflation (and even Paul Krugman admits now he was wrong, and that there really has been substantial inflation) has sent out a misleading economic signal to owners of inputs, owners of factories, and owners of labor services (that is, workers): “EVERYBODY WANTS YOU!”

But it’s not real. The signal of increased price, which looks like an overall increase in demand, is just a lot more money chasing the same amount of goods, which bids up prices across the board.

This interpretation of recent monetary policy aligns neatly with theoretical explanations that have been useful for identifying past bubbles.

Artificially low-interest rates (from easy monetary policy) were a big win for wind and solar (because of their high up-front capital costs) than for the fossil fuel plants that pay for fuel on the back end (have higher incremental costs). With on-grid wind and solar, the government has created an industry that must be perpetually supported with subsidies to avoid a bust.

Still, government subsidies and good PR attract a lot of entry to reduce margins, and companies can get into trouble such as Siemens.

Conclusion

It has been said:, ‘markets pick winners, leaving government for losers.’ The fact that the PTC was extended 14 times (the last being with the Inflation Reduction Act of 2022) and the ITC 5 times speaks for itself. Milton and Rose Friedman argued persuasively against the infant industry argument, which was the original justification for these tax credits, on the grounds that the infant industries never grow up.

How this all plays out is not exactly clear as government is certainly capable of doling out more subsidies and bailing out wind and solar firms when they get into trouble. But one thing that is clear is that if Congress were to repeal, or even just roll back provisions in the IRA, the artificial wind and solar boom would go bust.