A recent headline on Bloomberg announces, “Cheap Oil Is Bad for the Economy (At Least, So Far).” The assessment is based on a crude (no pun intended) Keynesian analysis from Goldman Sachs, which views the economy in terms of total spending. In reality, genuine economic strength comes from the ability to transform resources into goods and services that consumers desire. From this perspective, the fall in oil prices—driven by factors such as the U.S. shale boom and the halt in Federal Reserve monetary inflation—is an unambiguously good thing for the American economy.

Goldman: It’s All About (Spending) the Money

The following excerpt captures the flavor of the Bloomberg article:

Cheap oil means cheap gasoline, and the assumption throughout the oil price rout has been that for the U.S. economy, built on consumer spending, cheap gas is all good. In theory, yes. In practice, it’s been tough to find the benefits in the economic data this year.

Goldman Sachs estimates that a decline in energy-related investment such as new drilling equipment, caused by low oil prices, subtracted about half a percentage point from economic growth during the first half. That’s a pretty hefty bite out of a growth number that probably won’t be much higher than 2.5 percent over the first six months of 2015. A note out from Goldman this week suggests that so far the negatives of inexpensive crude oil appear to have outweighed the spur to consumer spending. Goldman forecasts that the drop in oil prices will account for about 30 to 40 percent of the slowdown in economic growth from its annual pace at the end of last year. [Bold added.]

This type of analysis is common on Wall Street, but it’s totally wrongheaded. If someone cured cancer, it would be silly to fret about all the medical spending that would be avoided.

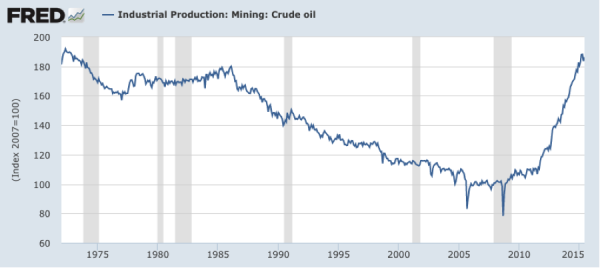

A major new force in the world supply and demand balance is the surge in U.S. crude output, emanating from the revolution in shale production. The following chart, showing an index of U.S. crude oil output (with the 2007 value set to 100), is simply incredible:

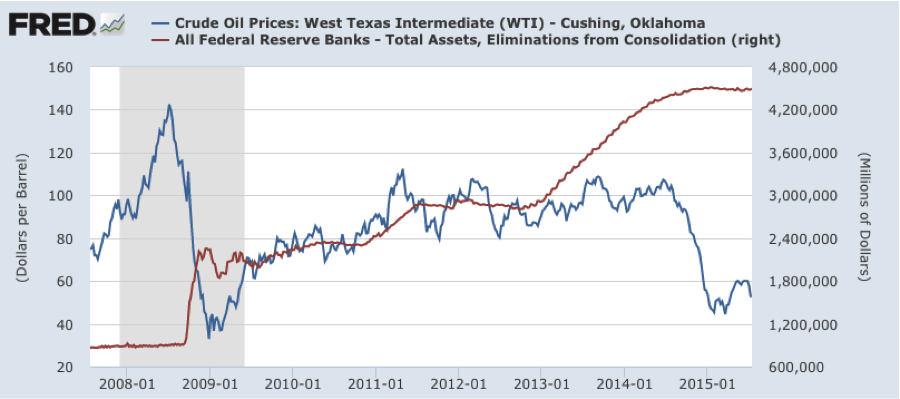

To understand why oil prices may have fallen when they did, there are obviously many factors. But one significant influence seems to be the halt of the Federal Reserve’s monetary expansion (popularly dubbed “QE3”), as the following chart shows:

As the chart shows, oil prices (blue) began their rapid decline right about the time that the Fed completed its so-called “taper,” and held its total assets (red line) constant. This (relative) tightening of U.S. monetary policy went hand-in-hand with a strengthening of the U.S. dollar (as I explained in this IER post in December 2014), and presumably made worldwide investors less anxious to hold commodities (which are a classic hedge against inflation).

Conclusion

If investment in oil and gas drops because of government interference, then that does indeed signify harm to the economy. But the reason isn’t that investment spending per se is always a good thing; it’s certainly possible for entrepreneurs to pour too much into certain projects. In particular, government mandates and taxes divert resources away from where they do the most good, as judged by consumers.

To the extent that falling oil prices reflect (among many factors) domestic improvements in drilling and “fracking” techniques, as well as a halt to Federal Reserve monetary inflation, these are unambiguously good things for the U.S. economy. Consumers obviously gain from having access to fuel at a lower price, and their gain more than compensates the direct loss to oil producers who are taking advantage of the new techniques. Another point is that the U.S. is still a net importer of crude and petroleum products (by about 5 million barrels per day), showing that a drop in the world price of oil would tend to benefit the U.S. economy as a whole. Indeed, that’s why Goldman analysts back in December said falling oil prices would act like a huge “tax cut” for the middle class especially. (In contrast, oil-exporting nations that have not benefited from their own version of a “shale boom” could be hurt, on net, from the fall in global prices.)

It seems that the oil market gets no respect. When prices are unusually high, the pundits complain about families struggling at the pump. And then when prices crash, the pundits complain about declines in energy investment. The real story here is that U.S. oil producers have increased production more than anybody dreamed a decade ago, exploding the narrative that we are an energy-starved country and need to embrace government-coerced conservation and other interventions as our only hope.