The Ukraine produces some oil, natural gas, and coal that it uses for domestic consumption, but it must also import these fuels in order to meet demand. The Ukraine’s major importance, however, is as a natural gas and petroleum transit country due to its geographic position and proximity to Russia. In 2013, about 3.0 trillion cubic feet of natural gas flowed through the Ukraine to countries in Eastern and Western Europe, providing 16 percent of Europe’s natural gas consumption. Three major pipeline systems move natural gas from Russia through the Ukraine to Europe and another pipeline moves petroleum.

Ukraine’s Energy Supply and Demand

Most of the Ukraine’s primary energy consumption is fueled by natural gas (40 percent), coal (28 percent), and nuclear (18 percent). In 2012, the Ukraine consumed 1.8 trillion cubic feet of natural gas, producing 37 percent domestically and importing the rest from Russia. A relatively small portion of the country’s total energy consumption is supplied by petroleum and renewable energy sources. In 2012, the Ukraine consumed 319,000 barrels per day of liquid fuels, producing 25 percent domestically and importing the remainder primarily from Russia with some deliveries coming from Kazakhstan and Azerbaijan.

The Ukraine obtains almost half of its electricity from its 15 nuclear reactors and most of the remainder comes from fossil fuels (46 percent) and hydroelectric power (6 percent). It generates some electricity from wind power (less than 1 percent). The country consumed 78.5 million short tons of coal in 2012, with 90 percent produced domestically.

Payment issues between Russia and the Ukraine have caused Russia to stop deliveries of natural gas and crude oil to the Ukraine in the past with the most recent stoppage over oil deliveries occurring in January 2014 and over natural gas deliveries in 2009.

The Ukraine has an estimated 128 trillion cubic feet of technically recoverable shale gas that could provide the country with a means to diversify its natural gas supplies away from Russia if developed. In January 2013, Shell agreed to explore an area that the government estimates holds about 4 trillion cubic feet of shale natural gas. The Ukraine is planning to develop its shale gas resources by 2020.

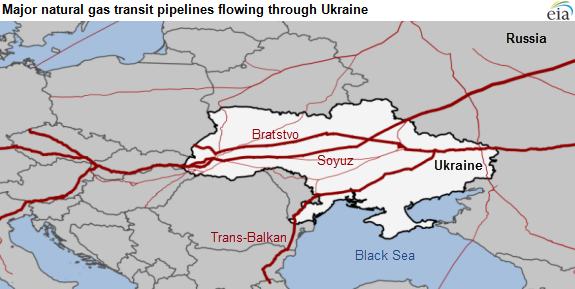

Pipelines Transecting the Ukraine

The Bratstvo (“Brotherhood”) and Soyuz (“Union”) pipelines move natural gas from Russia to Western Europe. The Bratstvo pipeline, Russia’s largest natural gas pipeline to Europe, crosses from Ukraine to Slovakia and then splits into two, supplying northern and southern European countries. The Soyuz pipeline links Russian pipelines to natural gas networks in Central Asia and provides natural gas to central and northern Europe. A third major pipeline delivers natural gas from Russia through the Ukraine to the Balkan countries and Turkey.

Source: Energy Information Administration, http://www.eia.gov/todayinenergy/detail.cfm?id=15411

In 2013, Russia supplied 30 percent of Europe’s natural gas consumption totaling 18.7 trillion cubic feet. That includes the natural gas consumption of all of the members of the European Union and Turkey, Norway, Switzerland, and the Balkan states. Based on data reported by Gazprom and Eastern Bloc Energy, EIA estimates that 16 percent of the total natural gas consumed in Europe passed through the Ukraine’s pipeline network. Natural gas shipments vary by season, ranging from almost 12 billion cubic feet of natural gas per day in the winter compared to 6 billion cubic feet per day in the summer.

In the past, as much as 80 percent of Russian natural gas exports to Europe transited the Ukraine. That was changed in 2011 when the Nord Stream pipeline that directly links Russia with Germany under the Baltic Sea came on line, reducing that number to 50 to 60 percent.

The southern leg of the Druzhba oil pipeline moves Russian crude oil through the Ukraine, supplying most of the oil consumed by Slovakia, Hungary, Czech Republic, and Bosnia. In 2013, about 300,000 barrels per day of oil transited the pipeline, about 75 percent of its capacity. Crude oil and petroleum products from Russia are also shipped by rail through the Ukraine for export out of the country’s ports.

Can U.S. Abundant Energy Help?

Policy makers are calling on the United States to help with the developing energy crisis in the Ukraine and potentially Europe. Some of the recent remarks include:

- Sen. John Hoeven wants the United States to put together a broad strategy to help the Ukraine become more energy secure and reduce its dependence on Russian natural gas.

- Sen. Chris Murphy was speculative about the imposed sanctions, “I mean there’s no doubt that if you cut off Russian gas to Europe, it will hurt. There’s no doubt that if you freeze Russian assets in places like Germany and Great Britain, it will hurt them.”

- Senator Richard Lugar, formerly head of the Senate Foreign Relations Committee, indicated that exporting LNG and building the Keystone XL oil pipeline are strong signals the United States is still invested in fossil fuels. While the politics of both are tumultuous, and any gas exports will “have to strike a balance” with businesses that rely on cheap natural gas in their production processes, “American interests diplomatically and strategically are clearly to get more permits. The fact is we do have the ability and that could make a huge difference because we can send this gas strategically in various directions, and a lot of it.”

In 2012, Russia exported $160 billion worth of crude, fuels and gas-based industrial feedstocks to Europe and the United States. These exports are a major part of the Russian economy, but as can be seen above, European countries are very dependent on their imports of these fuels from Russia. According to Germany’s Chancellor, Angela Merkel, Germany is willing to take the pain that Russian retaliation to sanctions would bring. But that may not be the case for other European countries, who together imported 32 percent of their raw crude oil, fuels and gas-based chemical feedstocks from Russia in 2012. But, this crisis is making the European Union more eager to secure access to U.S. oil and natural gas supplies, which means lifting the ban on oil exports and approving more liquefied natural gas (LNG) export terminals.

The U.S. Department of Energy (DOE) has approved 6 applications for LNG export terminals and the Federal Energy Regulatory Commission has approved a permit for one of those facilities that should beginning operating by the end of 2015. The other 5 may not begin operating until 2017 or 2018. Another 22 applications are awaiting DOE approval. Thus, none of these facilities will be able to help the current crisis with Russia and the Ukraine. Further, most of the early LNG imports are expected to go to Asian buyers under long-term contracts where LNG prices have been about 50 percent higher than in Europe.

It is also not clear that the companies wishing to build these terminals at this time will find it beneficial once the approvals are complete. It is very expensive to build LNG export terminals and those upfront costs will have to be recouped in the price of the LNG. Also, while U.S. natural gas prices are low at this time due to hydraulic fracturing, it is not clear if U.S. natural gas prices will remain at their current $3 or $4 per million Btu level into the future when the companies of these export terminals will still need to recoup their upfront costs. EIA is forecasting that U.S. natural gas prices at the Henry Hub will increase at a rate of 3.7 percent per year between 2012 and 2040.

Conclusion

European countries, including the Ukraine, are dependent on Russia for natural gas and petroleum, and the Ukraine is a major transit country for pipelines and other transshipment of these fuels from Russia. The current crisis in the Ukraine is indicative of the importance of diversity of energy supply and the sources of that supply. For example, the fact that the Ukraine gets almost half of its electricity from nuclear power and mines most of its own coal is beneficial given its dependence on Russian oil and natural gas.

While the United States is a major producer of natural gas, oil, and coal, it is difficult for it to be responsive to current European natural gas needs when the only approved LNG export terminal will not be operating before the end of 2015. But, what the United States can do is formulate an energy strategy for the future for meeting both U.S. needs and those of our allies, as well as exporting the policies and technologies that created the hydraulic fracturing revolution and attendant oil and natural gas boom in the United States. Ensuring a diverse energy portfolio that includes nuclear and coal should also be at the forefront of that strategy.